Charts of the Week: The Fastest V-Shaped Recovery Ever

First semis, then software; Peak Social Media; Your SaaSflation Is My Opportunity

America | Tech | Opinion | Culture | Charts

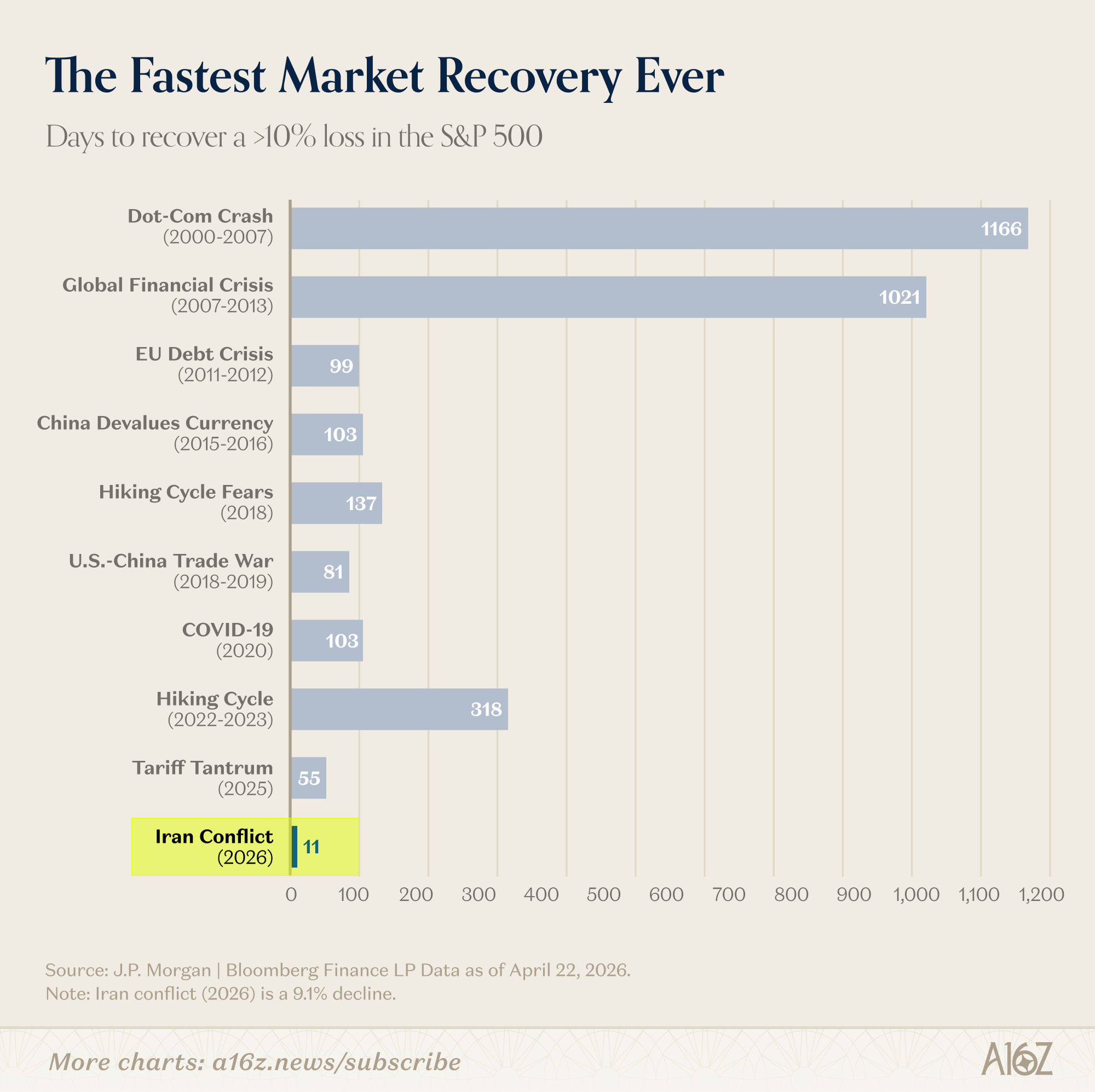

The Fastest V-Shaped Recovery Ever

S&P 500 sold-off by ~10% during the Iran conflict, and just 11 trading sessions later, it made a full recovery.

It constituted the fastest V-shaped recovery ever on record.

Last Friday, the S&P 500 closed at an ATH 7,165.08, up 30% yoy and almost 9% over the past month alone.

For situation monitors, the whiplash is a thing to behold. For everyone else, they may not have even noticed their 401(k)s took a header in the first place.

It could just be a coincidence, but either way, these fresh new market highs seem to have revived an old debate: are stocks too expensive? This comes only weeks after wondering ‘Is Tech Cheap?’ What a world.

Well, two of the most successful investors of the past fifty years recently weighed-in, and for their part, they’re inclined to say “yes, stocks are too expensive [for them, at least]”

In a CNBC interview during the March correction, Warren Buffett was asked whether stocks looked cheap. “No,” he replied. “Three times since I’ve taken over Berkshire, [the market has] gone down more than 50%... this is nothing. If they’re 5-6% cheaper, we aren’t in it to make 5% or 6%.”

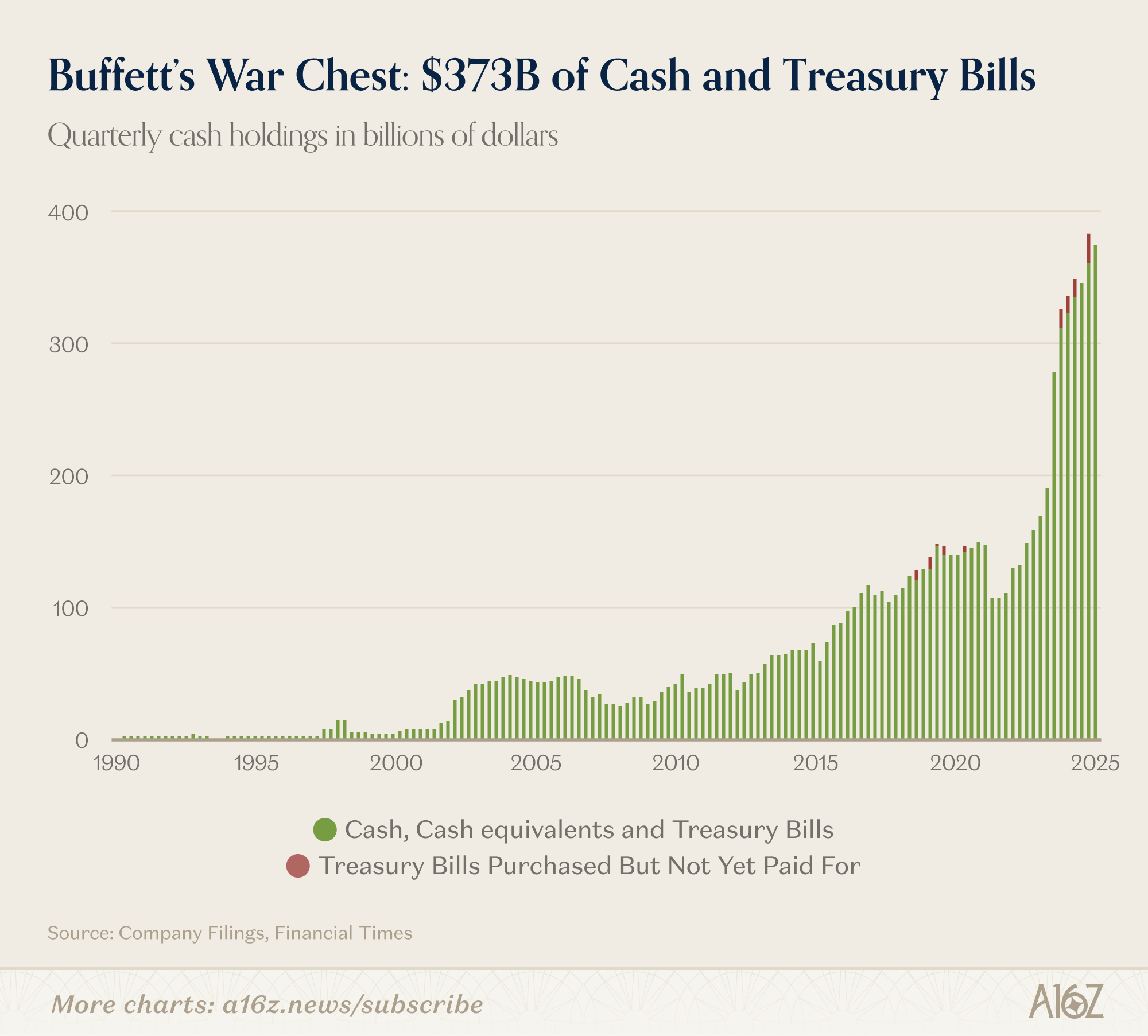

Buffett is certainly very busy not-putting his money where his mouth is.

Berkshire is sitting on roughly $373 billion in cash – the largest pile in its history – still waiting for that rainy day to go bargain-hunting.

The second hall-of-famer to cast some doubt on stock prices is Paul Tudor Jones. In an interview with Patrick O’Shaughnessy, PTJ pointed out just how high stock prices have become, in relation to the economy writ-large:

“We’re at 252% of stock market cap to GDP. In 1929, we were 65%. In 1987 we got to 85-90%. In 2000, 170% . . . Let’s say we mean revert to the past 25 or 30-year P/E. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.”

Sounds bad.

Now, what would cause that mean-reversion to transpire? Neither PTJ or Buffett can say for sure, but they’ve been around long enough to take the possibility seriously. It should be noted that the S&P 500 is up more than 10% since Buffett’s interview, for those keeping score at home.

Far be it for us to question the wisdom of those two giants—and mean reversion can be a helluva drug—but there may be some reasons why the market is structurally different now (i.e. we’re going to question it, anyways).

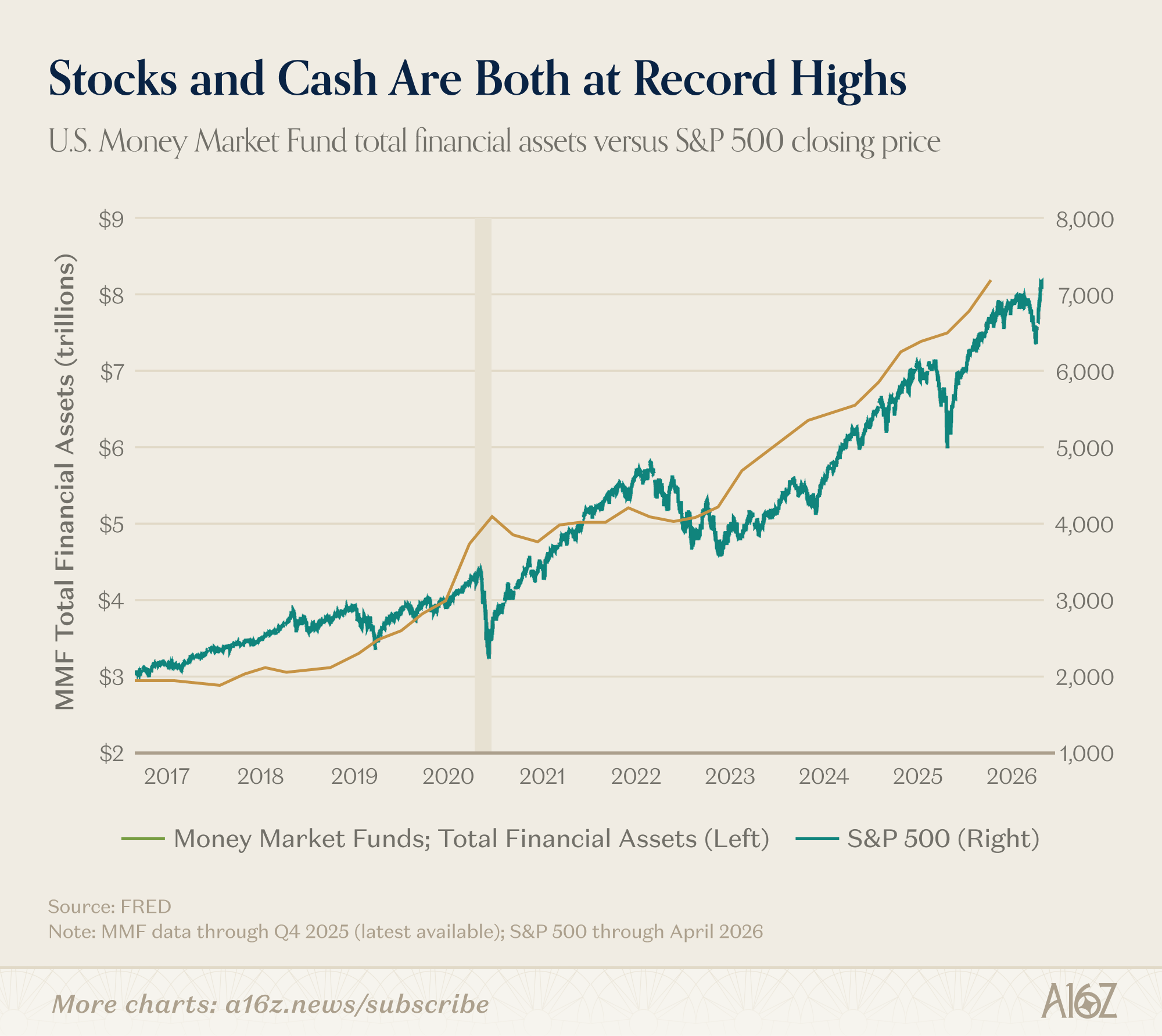

One reason that prices may be structurally higher is that there is just a lot more cash around now than there was before.

Just to take an overly simplistic view of things, despite all the money currently at-work in equities, the balance of money market funds continues to rise:

MMF balances are at record levels of ~$8 trillion, nearly double pre-pandemic levels.

More cash for MMF, and more cash for equities, and more cash for everyone, make stocks go brrr? Could be.

Fed Chair nominee Kevin Warsh made a similar call-out in his confirmation hearings last week. The Fed’s balance sheet doubled during COVID in 2 years—from $4.2 trillion to a $9 trillion peak. Even after three years of quantitative tightening, it sits at $6.7 trillion today, and roughly 30% of all U.S. dollars in M2 existence today were created in the last five years. That’s a lot of fresh cash.

If you view the S&P 500 as a price-ratio to dollars, the shrinking value of the denominator may be doing more work than people realize.

“The big balance sheet has become an ordinary, recurring force that, I think, has been quite unhelpful,” Warsh told the Senate Banking Committee. He called it “fiscal policy in disguise,” and said the Fed is “not blameless” in the widened wealth gap and K-shaped economy that has emerged.

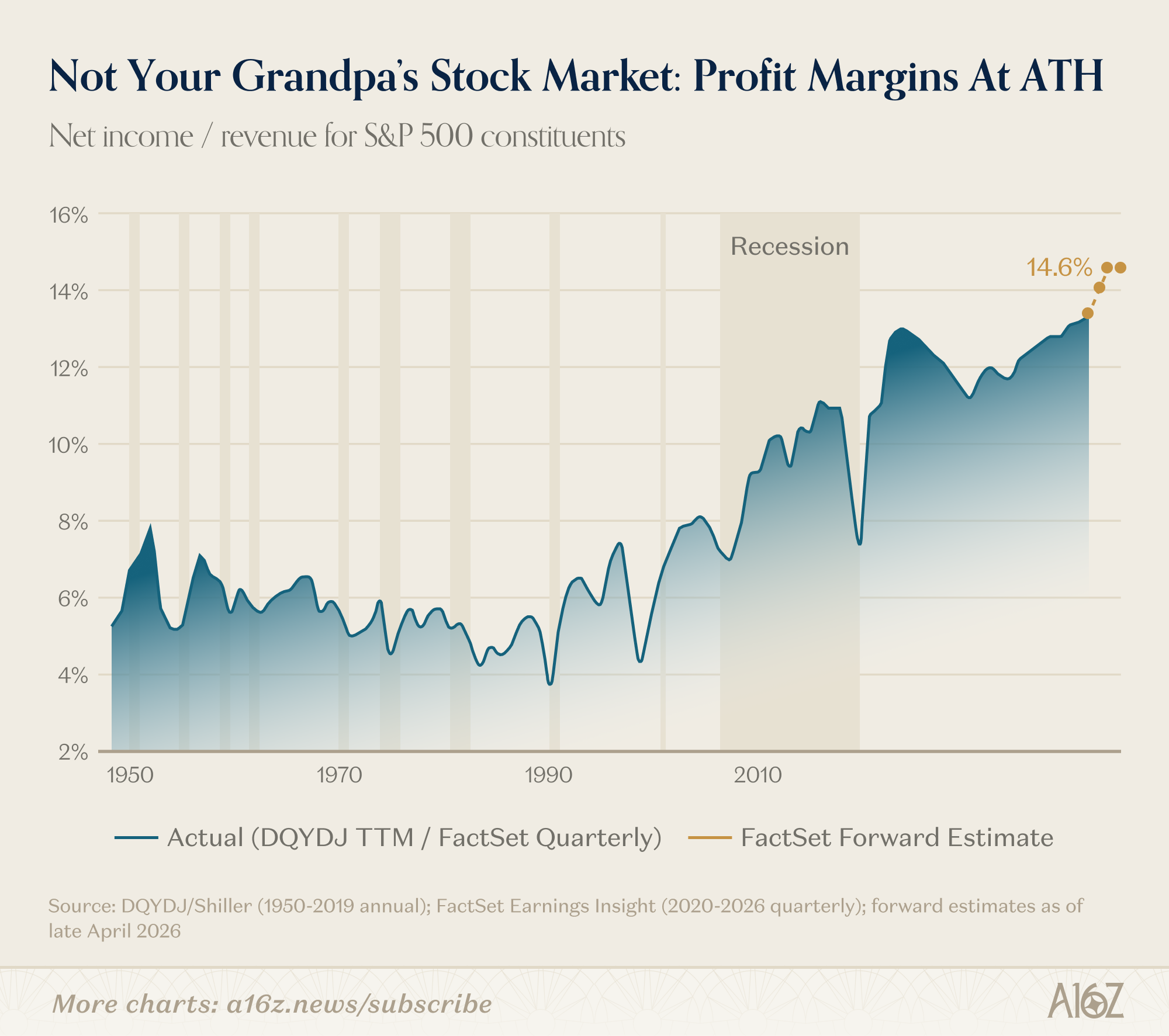

A second possibility, of course, is what we’ve alluded to before: the reason that stock prices are growing is because earnings are growing and margins are historically wide (and getting wider).

Generally speaking, more profits at fatter margins is a well-regarded basis for assigning higher multiples.

PTJ is certainly right that multiples are historically high and that the value of the stock market (relative to GDP) is too . . . but if you’re going to turn the clock back 30 years for a benchmark of what those values ought to be, then it bears mentioning that profit margins are roughly double what they were in the 1990s, and forecast earnings growth is more than double the long-term historical average.

Now, perhaps those forecasts are illusory, but still, “the prices are too high because they’re higher than before,” is on its own, a strange objection.

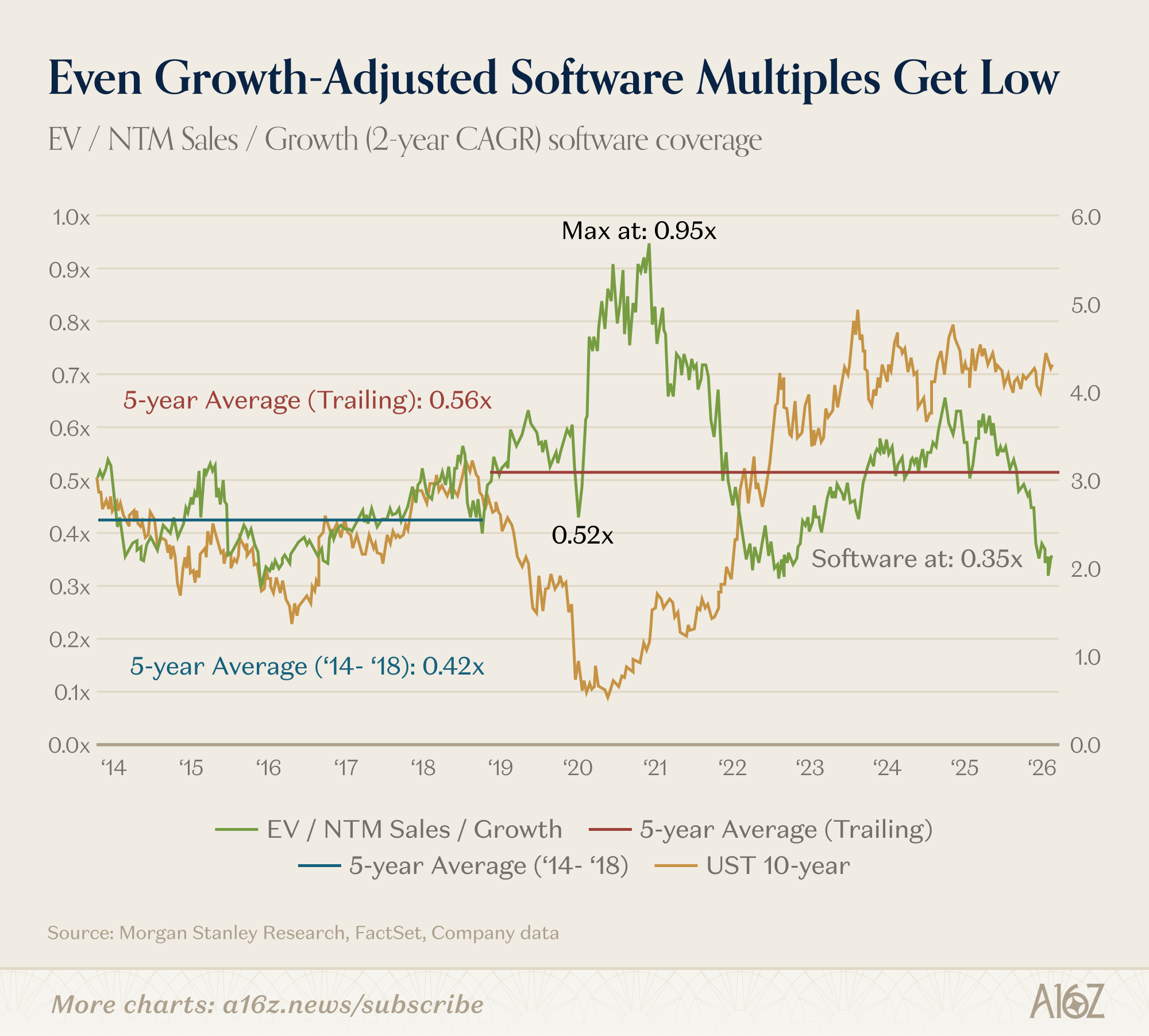

Depending on where you look, you might even say that in some cases prices are relatively low:

On a growth-adjusted basis, software multiples have already mean-reverted to the previous decade’s average.

“This time it’s different,” are, of course, the most famous last words, and when GOATs speak, we listen . . . but certain things are, in fact, different. For now, at least.

First Semis, Then Software

While on the subject of the stock market, one thing we’ve observed before is that while tech is driving a lot of the growth, it’s really semis (and AI infrastructure) specifically that’s driving the lion’s share of returns. Software, for its part, is still scuffling, relatively speaking (again, as we’ve observed many times before).

The out-performance of the AI buildout v. the more subdued performance of rest-of-tech raises an interesting question: how can AI infrastructure trade at a substantial premium, while the putative beneficiaries of AI trade at little-to-no premium, at all? If all this capex is going to be justified, there will need to be tangible benefits that flow through to the token-buying customers . . . but as of now, few-to-none of those benefits appear to be priced-in.

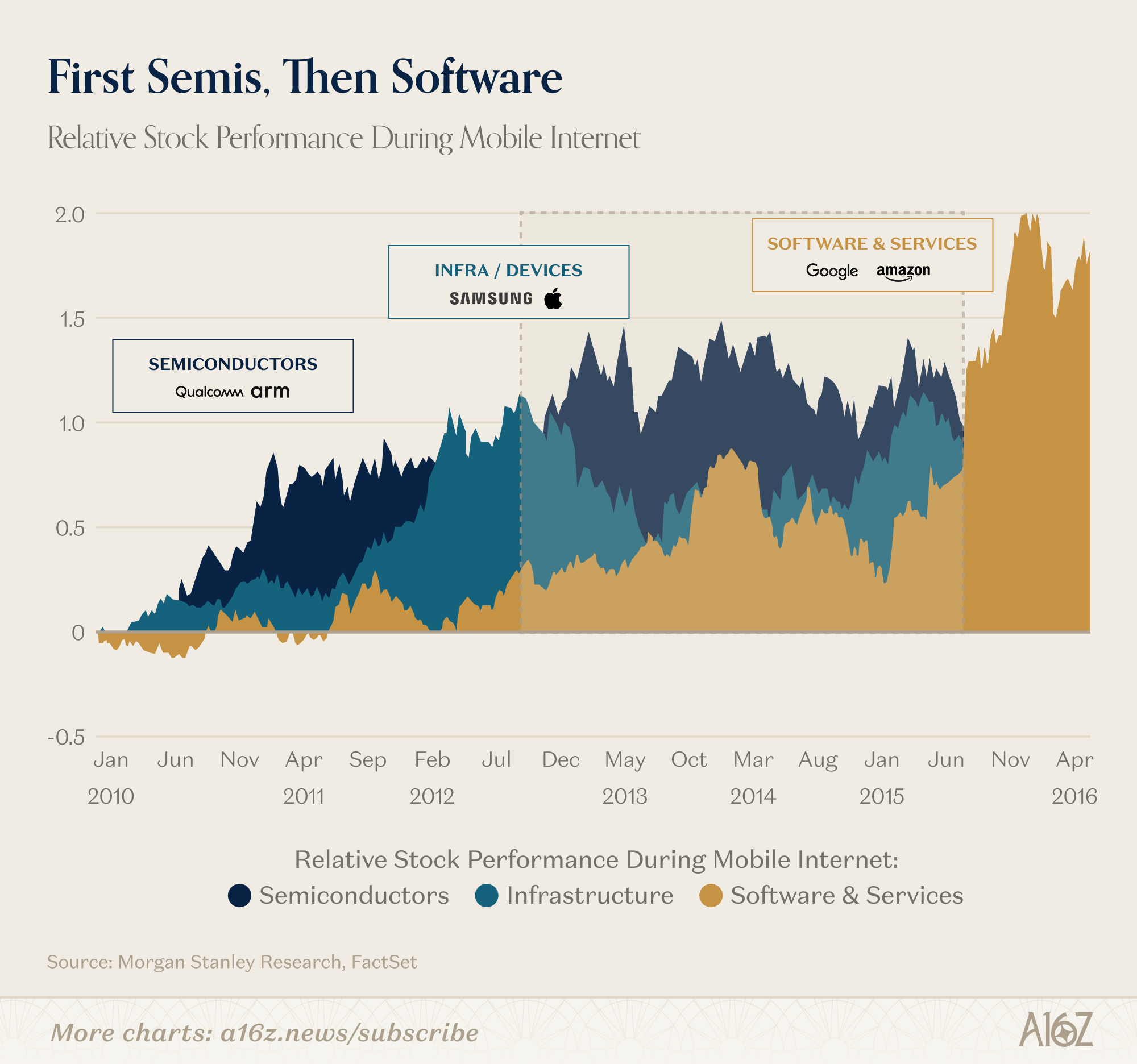

Without going down a rabbit hole of the various possibilities that might explain that disconnect, for present purposes, the point we want to make is that it has happened before: semis went first, and then software did eventually take the cake.

The post-GFC market recovery was also a “semis and infrastructure, first, software and services, second” kind of thing:

During the mobile-tech cycle, it took about 5 years for software to emerge as the clear market leader. Before then, it was semis and infra (i.e. the enabling capex) that led the way.

More precisely:

Semis like Qualcomm and ARM captured the picks-and-shovels returns from 2010 to 2012 because every smartphone needed chips before any apps could exist;

the platform layer (Samsung and Apple) came next by selling all those smartphones; and then

software and services came last, and won biggest—Google and Amazon (and the “app layer” more generally) pulled ahead, as value migrated up the stack to where the applications (now running on all that hardware) lived and breathed.

Is the AI cycle following the same semis-then-software trajectory? It’s not for us to say, but there are certainly some similarities.

First, of course, is the semis-led charge, although this time, instead of Qualcomm leading the way, it’s Nvidia.

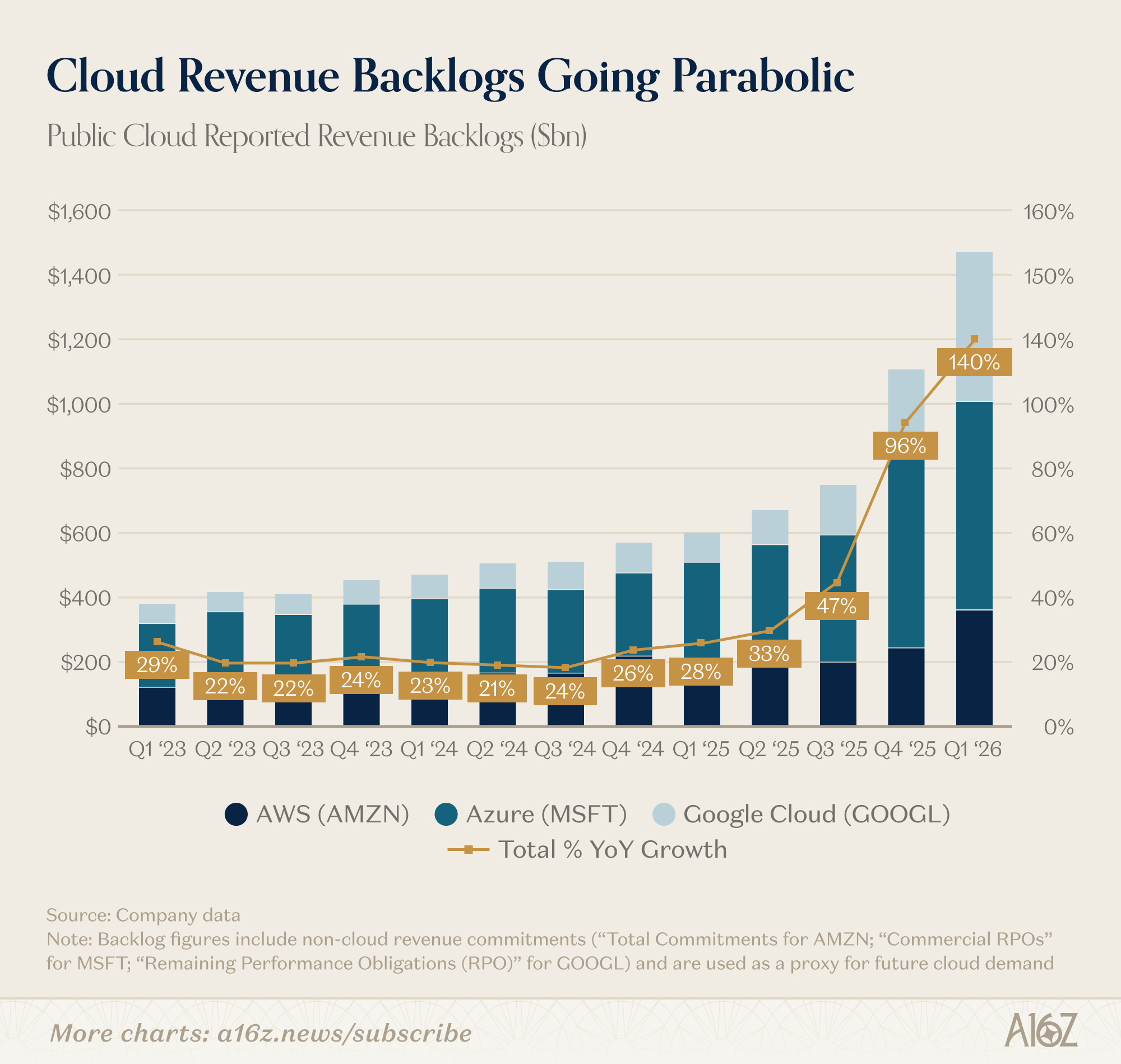

Second, is perhaps the acceleration in cloud, one layer up in the stack, where all those chips are being put to work:

Reported revenue backlogs for the hyperscalers nearly doubled yoy in ‘Q4. That’s not supposed to happen to already fully-scaled businesses.

Third is . . . well, the third is where it gets interesting.

The previous semi-led cycle’s biggest winners came from the application layer—Uber, Airbnb, Instagram, WhatsApp, etc.—and enterprise SaaS, as well. They were preceded by all the hardware because without all the hardware, none of the software would have been possible at that scale. It did take ~5 years, though, from the beginning of the semis-charge to when software really took off.

In the AI cycle, we know that the application layer is, in fact, scaling—indeed, scaling faster than ever before, albeit mostly on the private side. Speed-to-revenue for AI companies is unprecedented.

Whether and when the application layer takes off in the public markets—and brings software back to the fore—only time will tell. But this isn’t the first time that atoms have led the bits.

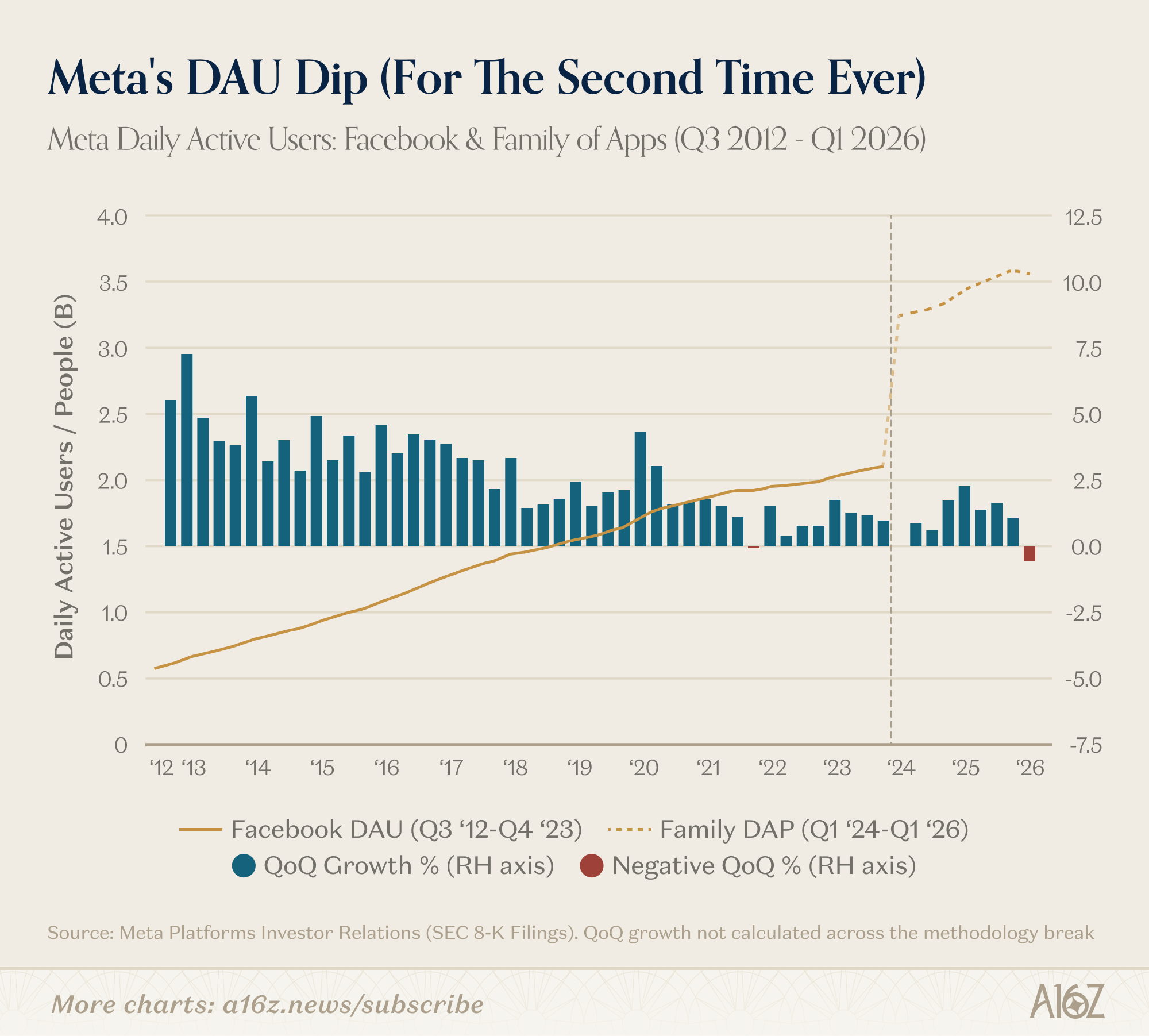

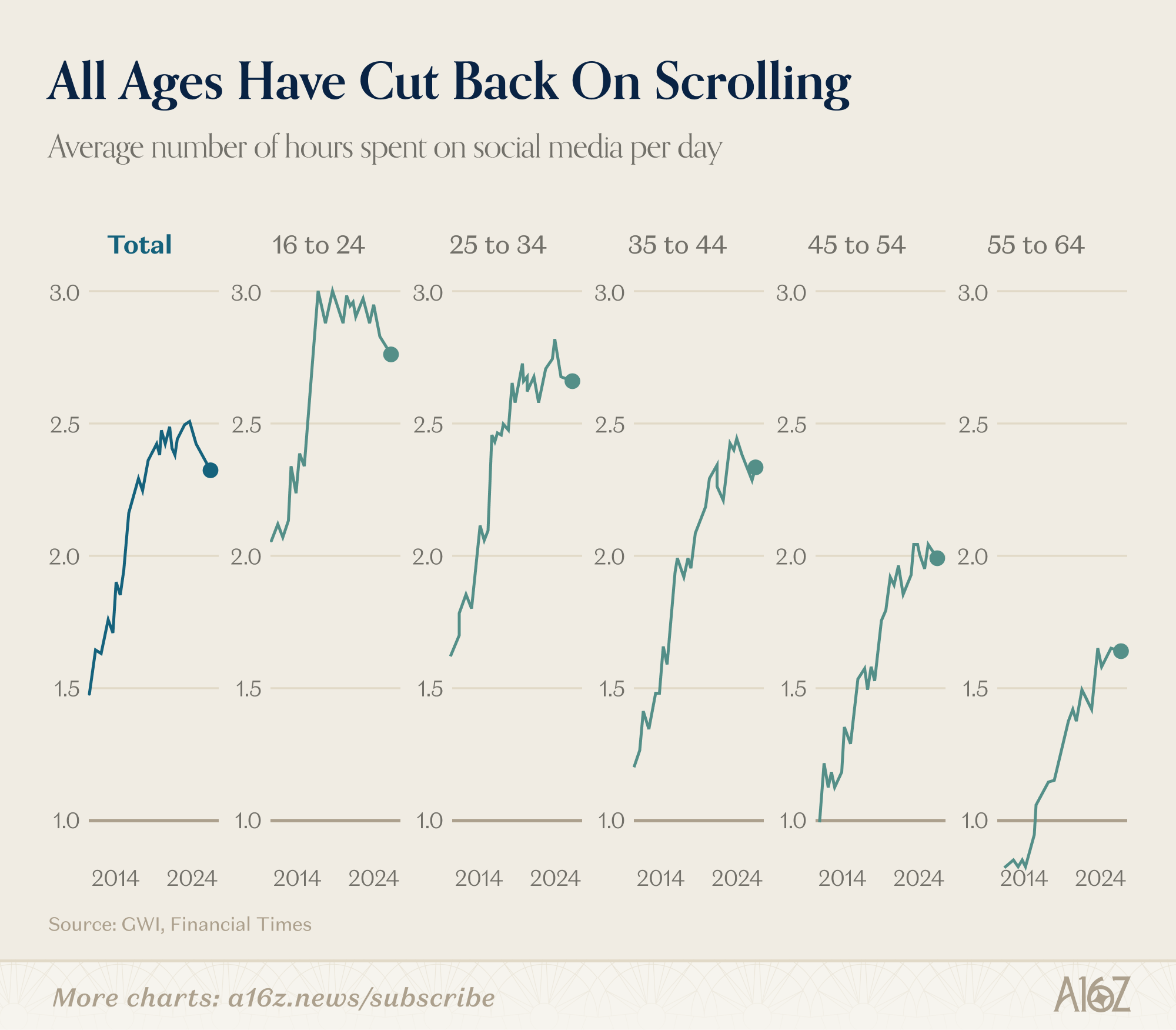

Peak Social Media

Here’s another first.

Meta’s daily active users declined for the first time, well, not “ever,” but the first time since 2021, which makes this the second time ever.

3.5B+ daily users is still a lot, but it’s slightly less than before.

It turns out, however, that “less time on Facebook” may be part of a broader theme.

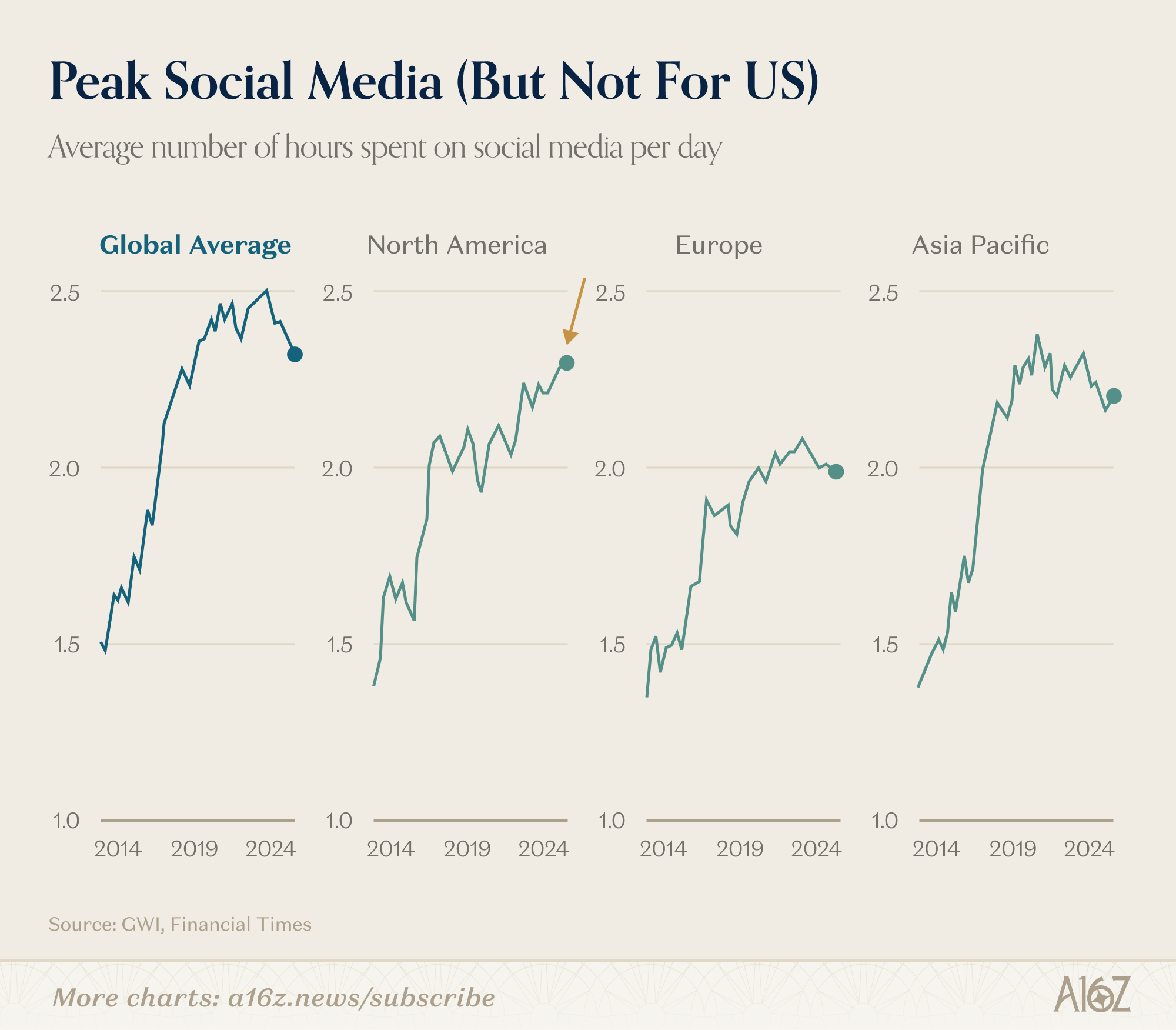

Time spent on social media globally peaked in mid-2022 and has been falling since.

According to GWI’s tracking of 250,000 adults across 50+ countries, daily social media use across the developed world fell by about 10% from a peak of ~2.5 hours in 2022 to ~2.3 hours.

The decline is sharpest among the demographic most associated with platform addiction: 16-to-24-year-olds. If you’re in camp “social media and the phones are bad for the youngs,” then this is good news.

There is one notable exception, however:

North American social media consumption is still rising. By 2024, it had climbed to roughly 15% more than European levels and is still rising.

Why do North Americans appear to be uniquely addicted to social media? Your guess is as good as ours, but it will be interesting to see how AI plays into this dynamic. AI-generated content is exploding all over the internet, and social media is no exception. Whether standalone AI-content apps for image/video generation, or the tools that platforms are rolling out for creators, AI is increasingly in the creator’s seat (or perhaps the co-pilot’s seat).

YouTube CEO Neal Mohan wrote in his 2026 letter that more than 1 million channels used YouTube’s AI creation tools daily in December, and 9 of the top 100 fastest-growing YouTube channels globally are entirely AI-generated.

Maybe consumers will get tired of it . . . or maybe social media’s hold on our attention spans is just getting started.

Your SaaSflation Is My Opportunity

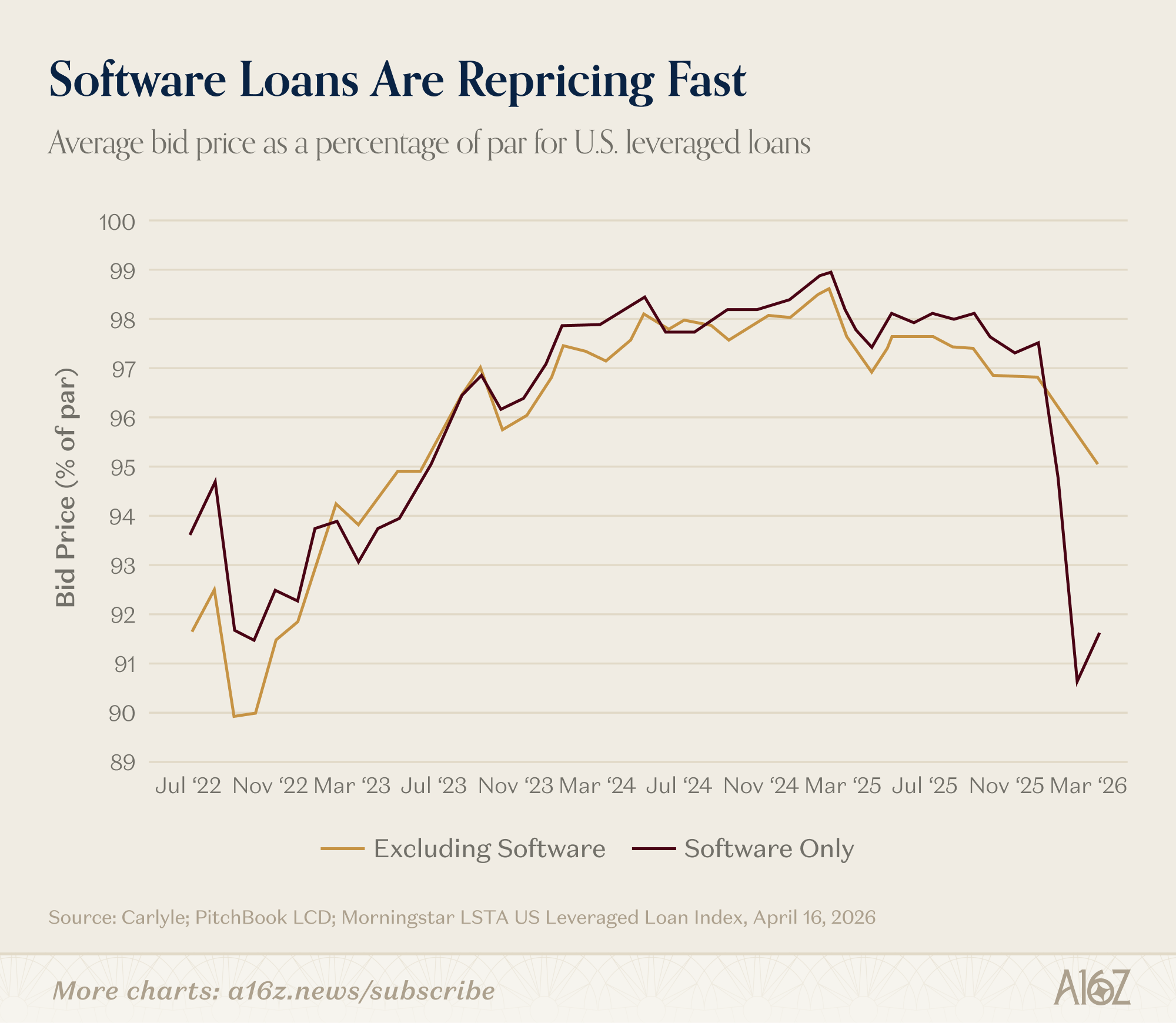

Here is yet another observation related to the current software malaise: the spillover into the credit markets.

For a decade, software was considered a fantastic thing to lend against. SaaS companies had predictable cash flows and sticky, recurring revenue, which are exactly the kinds of things that lenders like to see. The private equity industry built an entire playbook around it: buy mature software businesses, lever them up, and let the revenue service the loans. Lenders, for their part, were happy to harvest the yield.

But with the big compression in software multiples, that playbook has broken down. It’s had some big implications for private credit, and the publicly traded Business Development Companies that specialize in this sort of thing.

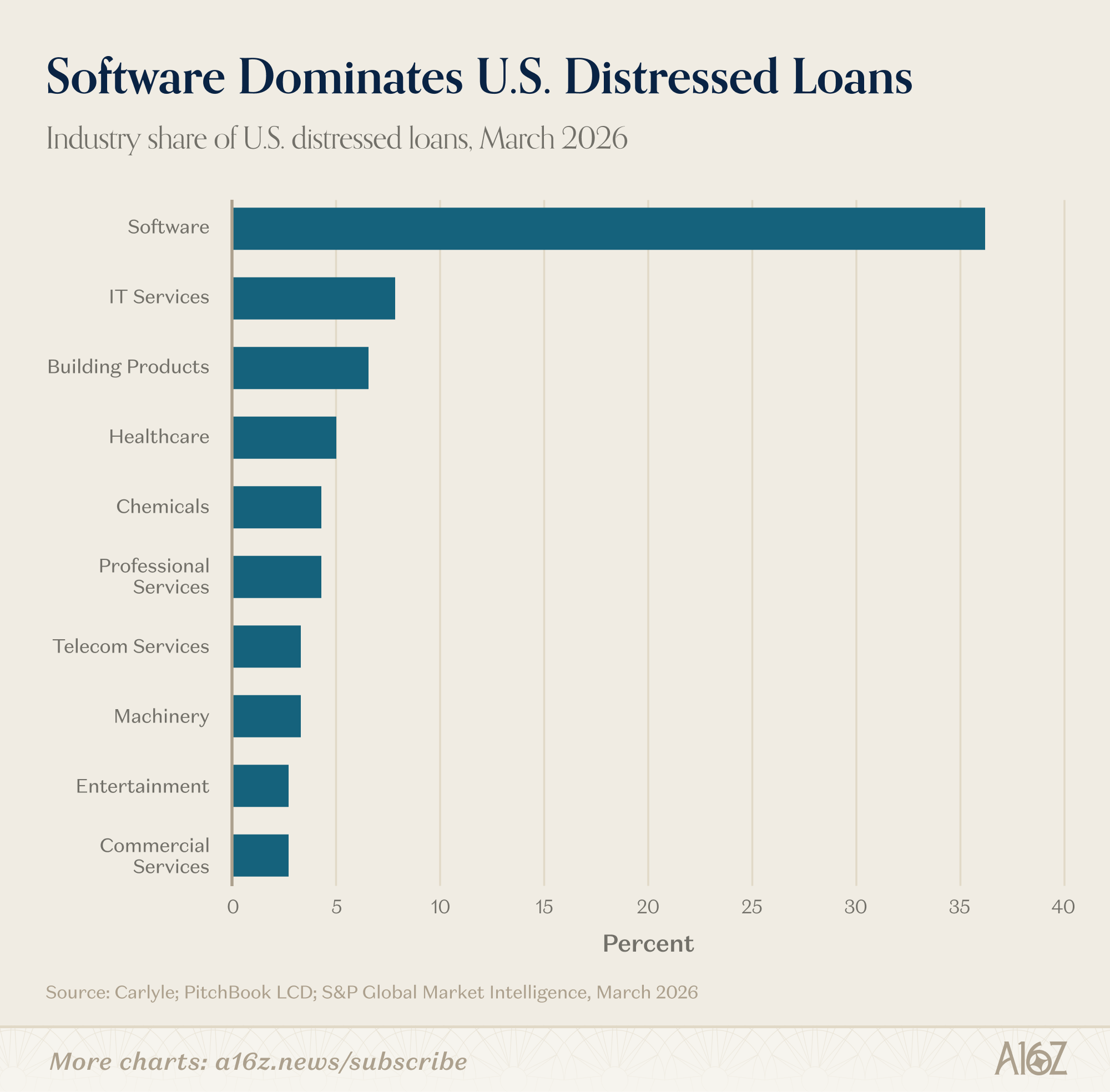

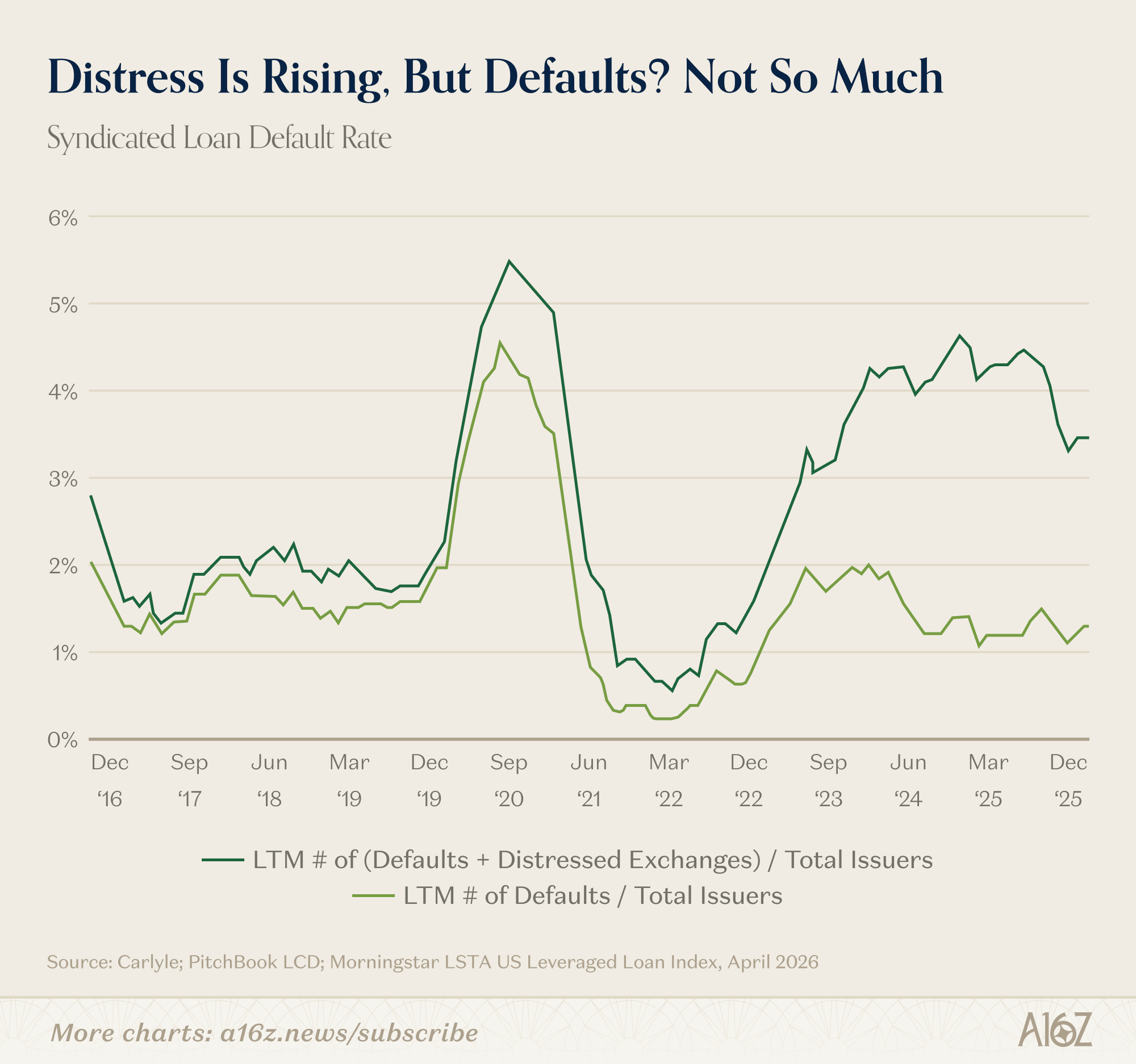

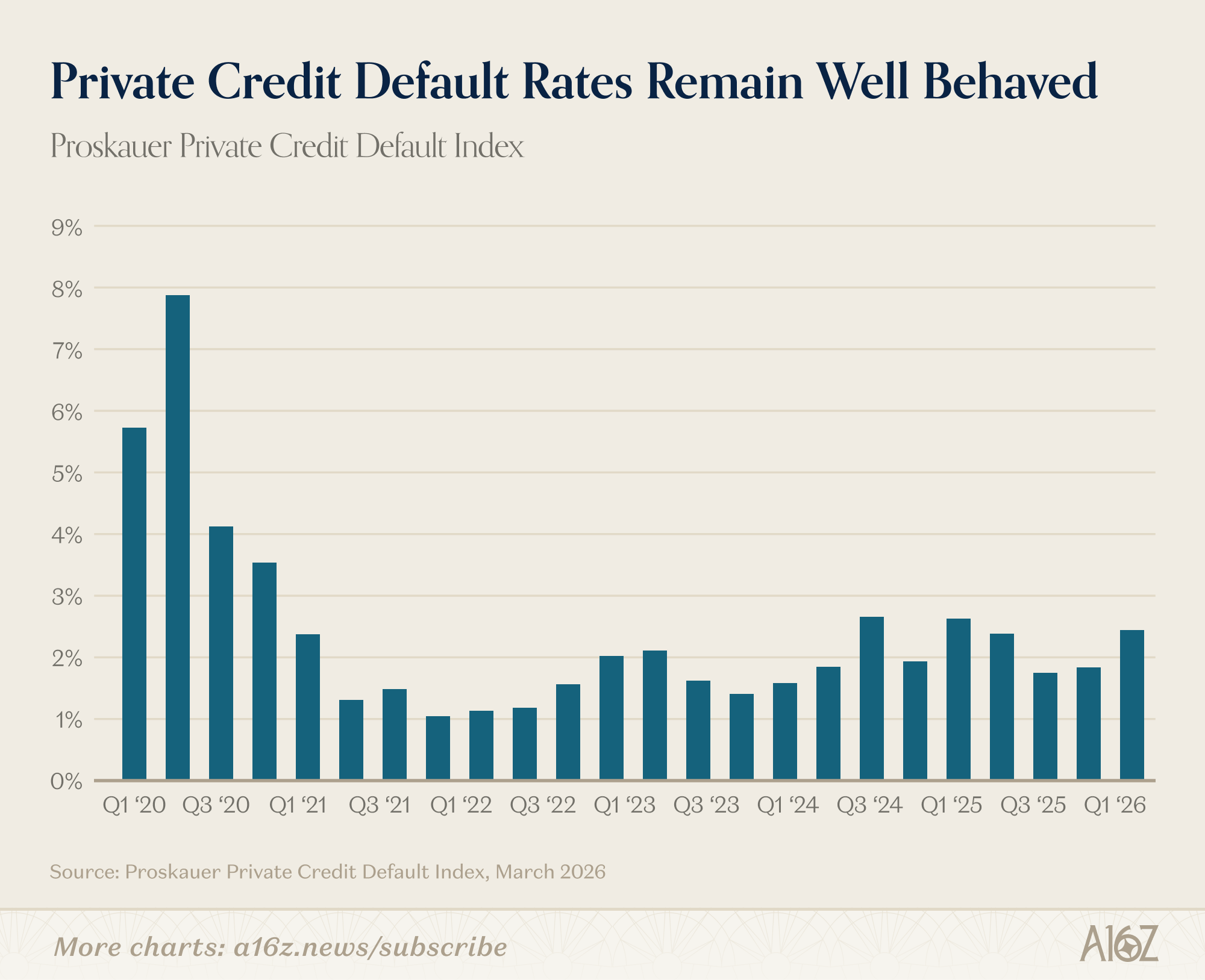

Pricing on software-backed debt has plummeted, relative to comparable credits from other sectors:

Average bids on software loans have dropped to ~90 cents on the dollar, and software now comprises ~35% of distressed loans (usually defined as loans trading with a ~20%+ discount).

Software gets less valuable, so too do software-backed loans. Makes sense, right?

Well, sort of. It certainly makes sense that the equity would reprice, but equity is not debt. And from an actual credit perspective, the loans are still performing about as well as they were before:

Default rates in either of the syndicated loan market or private credit both look no worse for the wear.

Now, present default rates aren’t necessarily predictive of future default rates, but the point still stands: software debt is selling off, even though software lenders are still getting paid, and that’s a bit odd. Just because the value of all future cashflows of a company may be worth less than they were before, doesn’t mean those cashflows are so impaired as to make the debt something less than money-good.

So, what’s going on?

Well, there are, of course, anecdata to make lenders nervous, like this one: Thoma Bravo recently forfeited its SaaS company Medallia back to its creditors. Thoma Bravo bought Medallia in 2021 for $6.4 billion, financing the deal with about $3 billion in debt. As interest rates rose, however, Medallia’s annual debt service roughly tripled from $100 million to $300 million. Fast-forward to the present, and Blackstone and other lenders refused to extend a lifeline, so Thoma Bravo decided to write down its $5.1 billion in equity and hand over the keys.

Medallia’s core business is a feedback-and-survey product, which is exactly the sort of thing in the crosshairs of AI-disruption. A big discount on the equity probably makes sense. But will disruption come so quickly and so intensely such that the company will lack the cashflows to repay the debt, as well? Perhaps, but perhaps not, and what’s true of Medallia isn’t necessarily true of the entire universe of software-backed loans.

But, that hasn’t prevented the sector-wide pall. Asset prices have dropped, fundamentals be-damned. And for the credit-pickers willing to be discerning, that means it’s “go time.”

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

What I find underexplored: how this dynamic is reshaping founder fundraising psychology. When public markets snap back this violently, the private market narrative resets almost in real time too, LP confidence, valuation anchors, risk appetite all shift before the quarter even closes.

Been writing about exactly this tension, how macro whiplash filters down into early-stage decision-making. Happy to share if anyone's thinking through the same.

As a small bakery business with web and four stores, the SAAS software we use is becoming increasingly problematic to achieving AI automation.

SAAS advantage is building a UI for the data it stores or processes. Those UIs have been enshitified over the years as the SAAS providers have been adding features to try and get more monetization and differentiation. That strategy is at odds with what I as a small business want to achieve with AI.

I want to create an AI interface to my data in that is stored in the SAAS that is turn to my use case and allows me to have UIs and agents work across the SAAS platforms. I'm already at odds with my inventory management SAAS provider. The answer is two fold:

1. Build my inventory management from the ground up. Then I can have my own data nsematics and direct database access.

2. move to an open source source platform that enables some UI and existing data semantics but allows me full customization with new UIs and agenic solutions.

The SAAS provider wants me to engage their engineering but they never seem to be able to get a meeting together. Likely because they don't see an answer that maintains their business case.

At least from my perch, the SAAS providers only "moat" is the data stored in the SAAS specific database. Do they allow direct access to that data. If they do, they destroy their moat. If they don't, I move.

The SAAS providers certainly have legacy momentum but as far as I can tell, zero forward strategy for maintaining their business case. Especially given how good AI LLMs are at coding.

I predict that by next tax season, TaxAct and Turbotax will have lost at least half of their subscription base if AI LLMs can connect directly to submit taxes for the federal government and states. That's a very simple concept for them to enable. An the LLM has a much better UI than either of the platforms. Also given the experience I had with taxes this year, AI LLMs are better at implementing the rules and discovering additional tax deductions. I believe TaxAct, TurboTax, H&RBlock and tax accountants are creating a disinformation campaign around the potential problems to slow the inevitable.

I'm only an anecdotal case, but from my perch, the SAASpocolips is real. I have the advantage that I have a deep technical background also. Other small business may not. But I still don't see how a small business wouldn't be looking at AI as a way of lower SAAS subscription costs at the same time it increases useability and productivity.