Charts of the Week: Software Ate the World

Railroad GPT; Stablecoins volumes are shifting from transfers to payments; The Next Decade of News; See ya later, productivity gains

America | Tech | Opinion | Culture | Charts

We’re excited to welcome Lisha Li to the a16z Infra team. See her announcement here. -AD

Software ate the world

Obviously, we’re biased, but it’s hard to overestimate just how important technology is to the global economy.

You might even say that software, literally, ate the world:

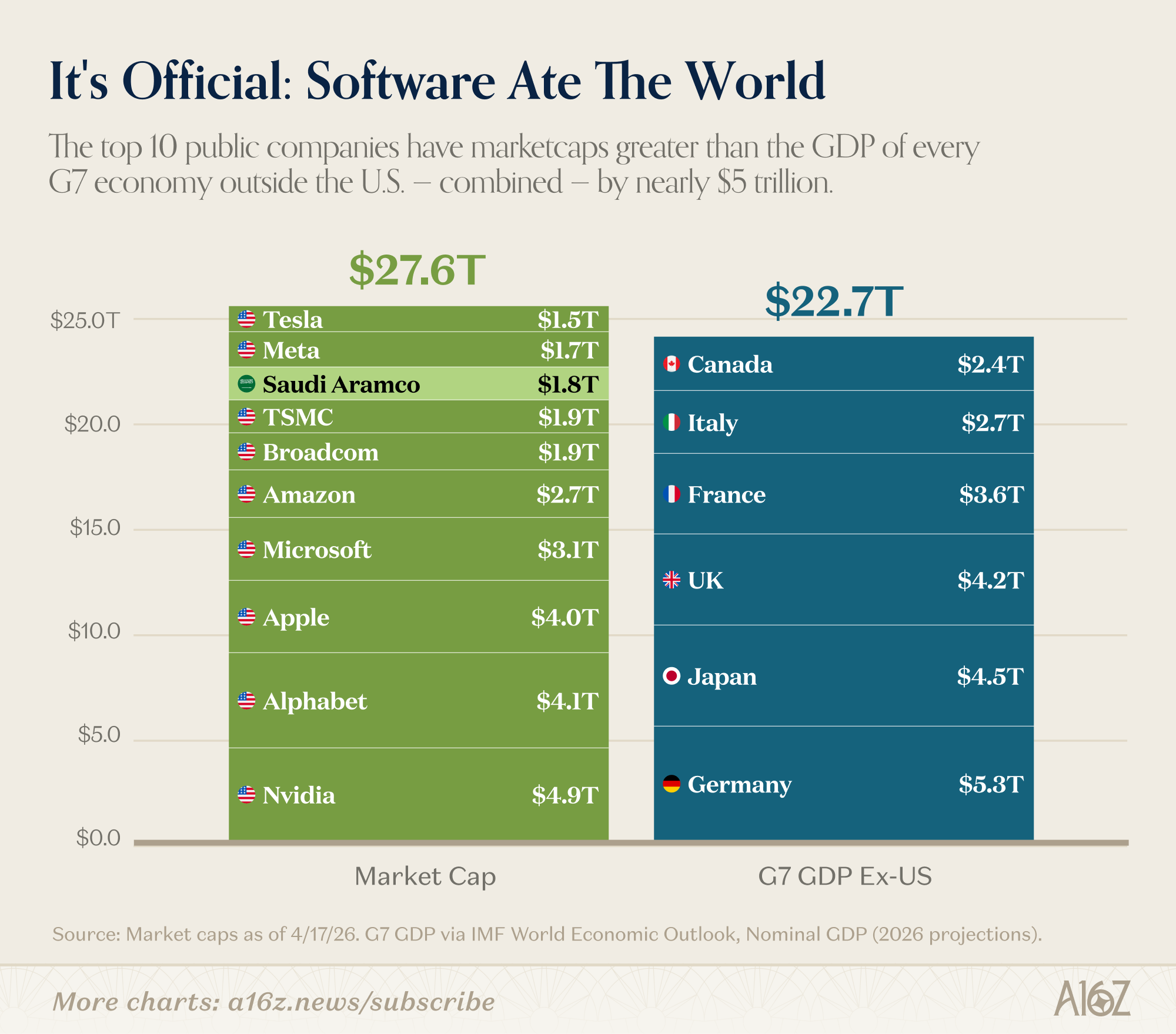

The top 10 public companies by market cap are larger than the combined GDPs of the G7 (ex-US)--and that would be true, even if one excluded Saudi Aramco, which no one would consider a “tech” company. (Although it was founded in San Francisco!)1

To be fair, the Top 10 list is more “tech and semis [and however one would categorize Tesla and Apple]” than pure-play software, but the point stands: tech isn’t just a big deal, it’s the biggest deal.

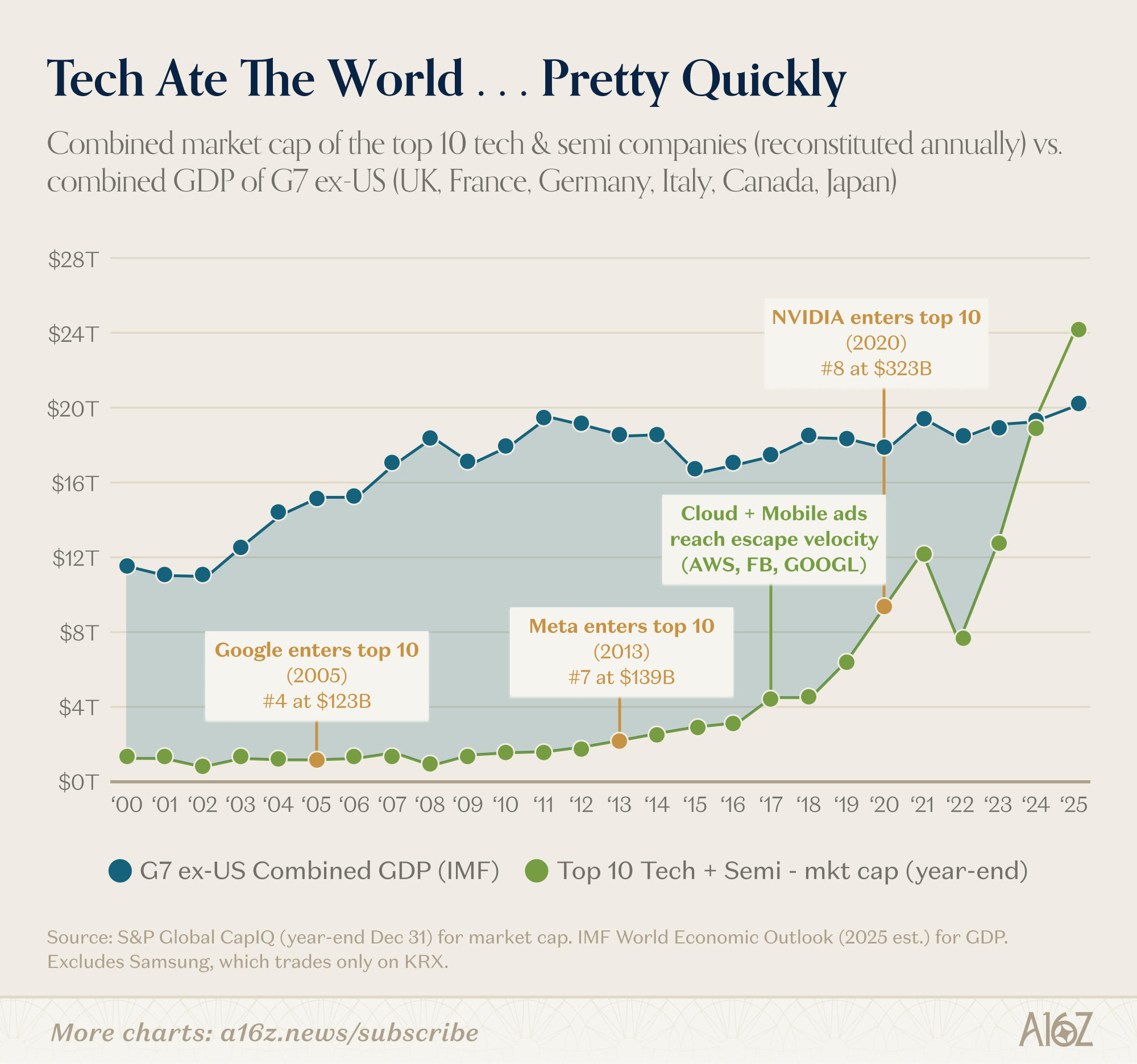

And tech’s global takeover has all happened fairly recently:

The top 10 techcos were a small fraction of the G7 (ex-US), until cloud really began to hit its stride in ~16-’17. From that point, it took less than a decade for their combined market cap to eclipse the rest-of-world’s GDP (ex-China).

Tech’s ascendancy isn’t just a changing of the guard, either.

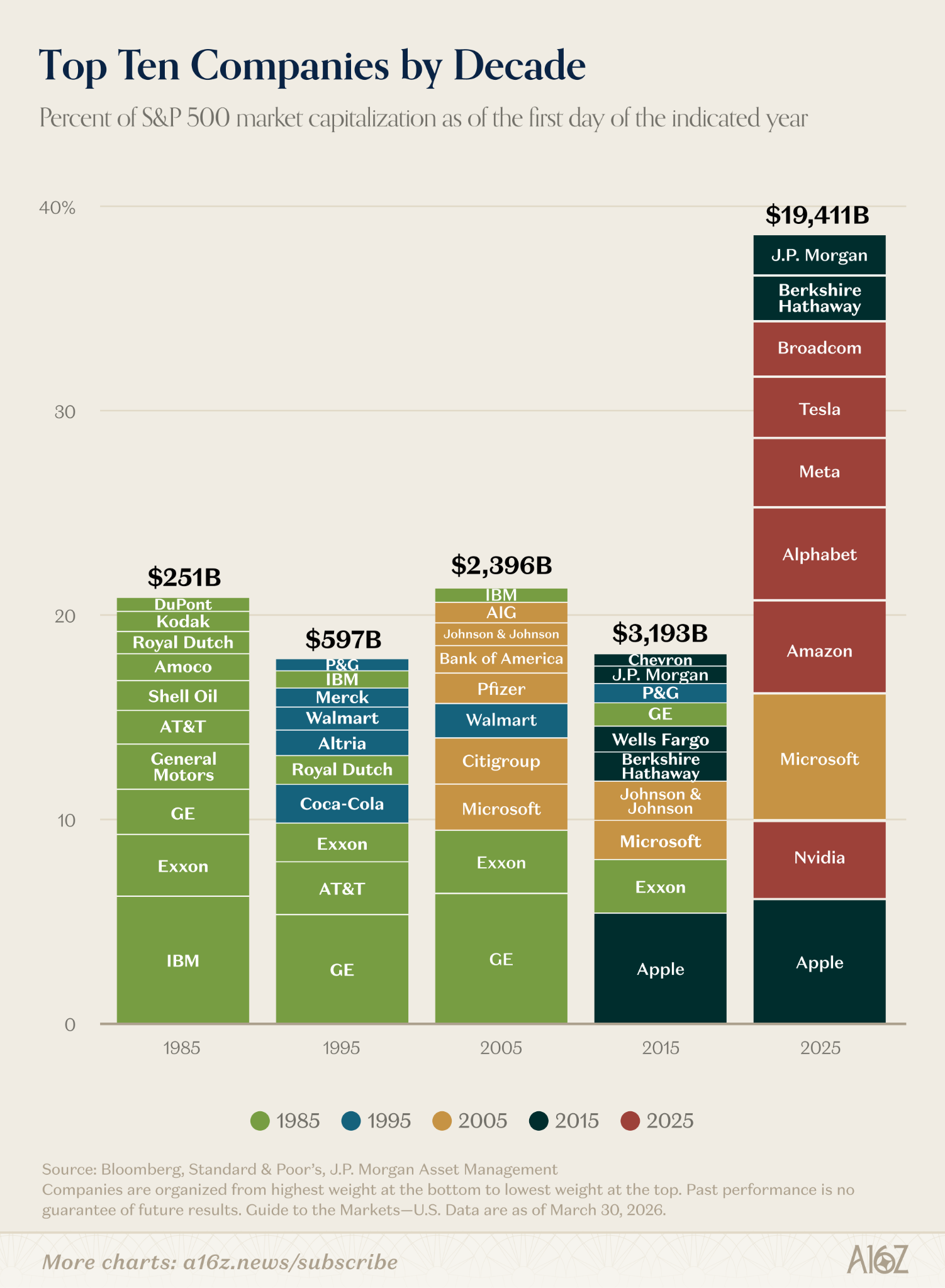

The biggest companies are much bigger than they were, even just 10 years ago:

The combined market cap for the 10 largest companies in the S&P is ~6x larger than it was in 2015, and comprises ~2x larger share of the total index.

To be sure, there was in fact a changing of the guard. The composition of the Top 10 changed-over dramatically, relative to prior decades. By 2025, there were only three holdovers from the previous decade, and only one (Microsoft, a tech company), from the decade before that.

If you were an investor back in 2015, and you were trying to model comparable outcomes for techcos based on the biggest companies in the index, you would have undercounted the upside by a country mile (or 6). Fundamentally, tech “busted the model,” by redefining the outer limit of how large companies could become.

And the outer limit still appears to be moving outwards!

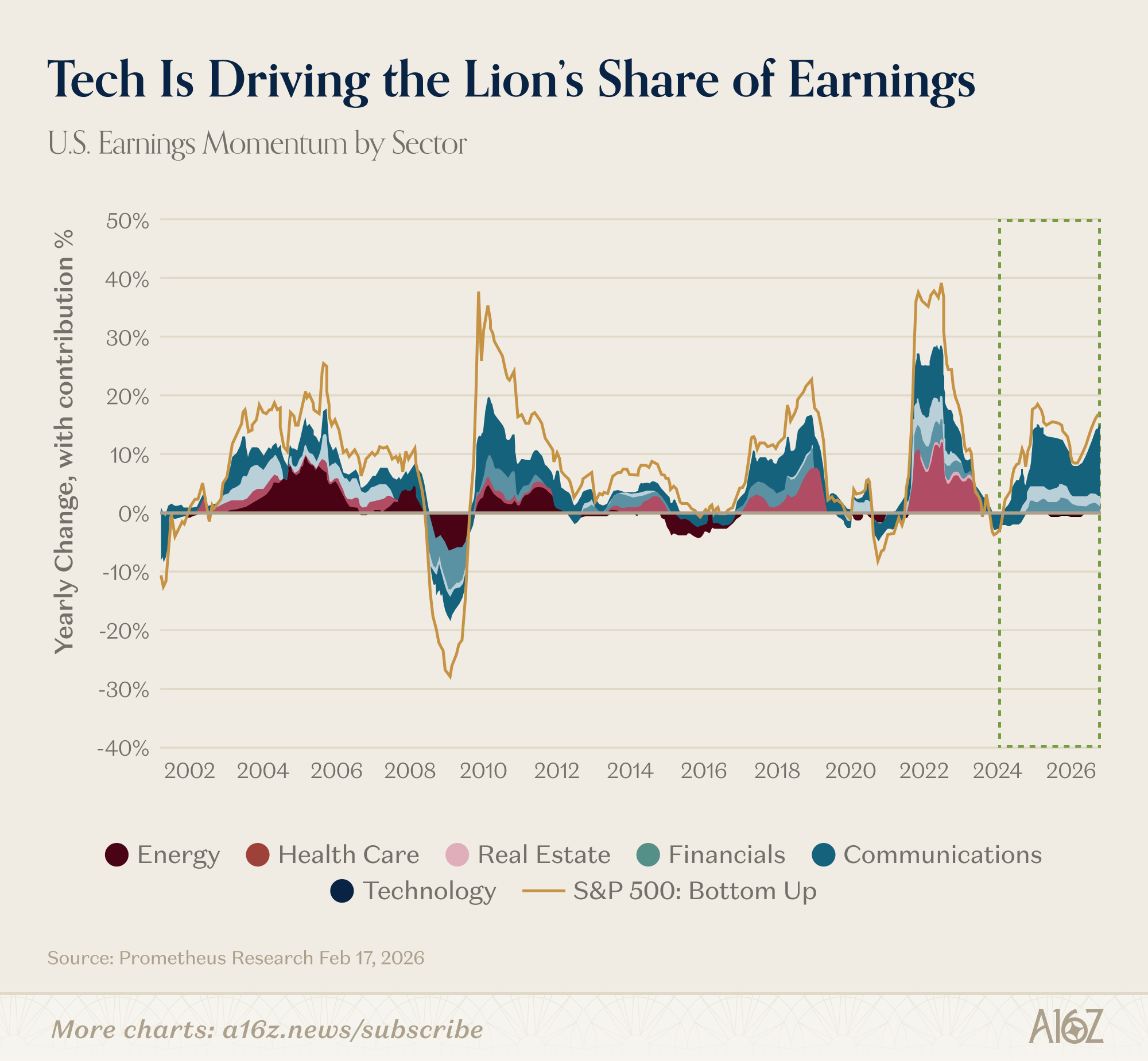

Indeed, tech has become even more central to the global growth story, as of late. Last week, we showed that Tech earnings are expected to grow ~2x faster than the rest of the market. But, if you look back even further, you would notice that tech is contributing an historically large share of the market’s overall earnings growth:

Since 2023, Tech has been responsible for ~60%+ of earnings growth (give-or-take), market-wide.

Other than a brief moment for energy in the early aughts, no other sector has played such a central role in the earnings story (and for quite so long) this century.

At this point, it’s fair to say that tech isn’t just a cycle, it is the cycle.

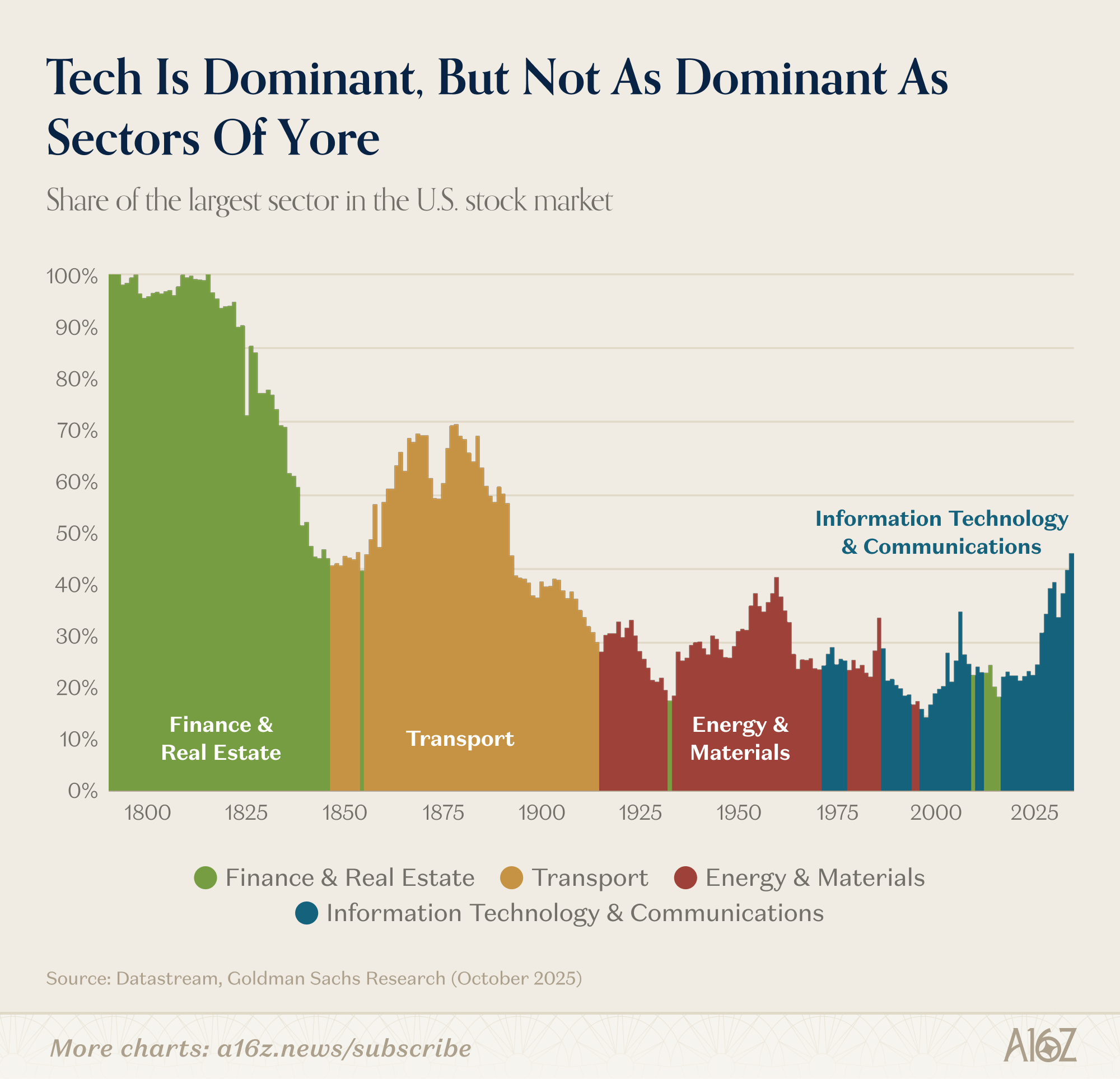

Railroad GPT

We just told you that tech is an unprecedentedly large deal, but that’s not actually true.

In the industrial era, no sector has ever been quite as big a deal as railroads:

At their peak, railroads comprised ~63% of the US market-cap, which BofA calls the “most dominant innovation sector ever.”

Now, doomers like to point to that railroad chart as a cautionary tale: you see, railroads used to be 63% of the market, but the bubble burst, and now they’re barely a rounding error.

Well, no, not really. Railroads are still a big deal, but what really happened is that railroads ushered in an entirely new economy that was previously unimaginable (and bigger than railroads ever could have been).

Railroads ceded their dominance to industrials, which eventually ceded their dominance to tech (with a brief interlude for finance and real estate, in the lead-up to the Global Financial Crisis).

And again, while tech is big today, it’s still not nearly as big (relatively) as Transport (or Real Estate and Finance) ever were at their peaks in the 19th Century.

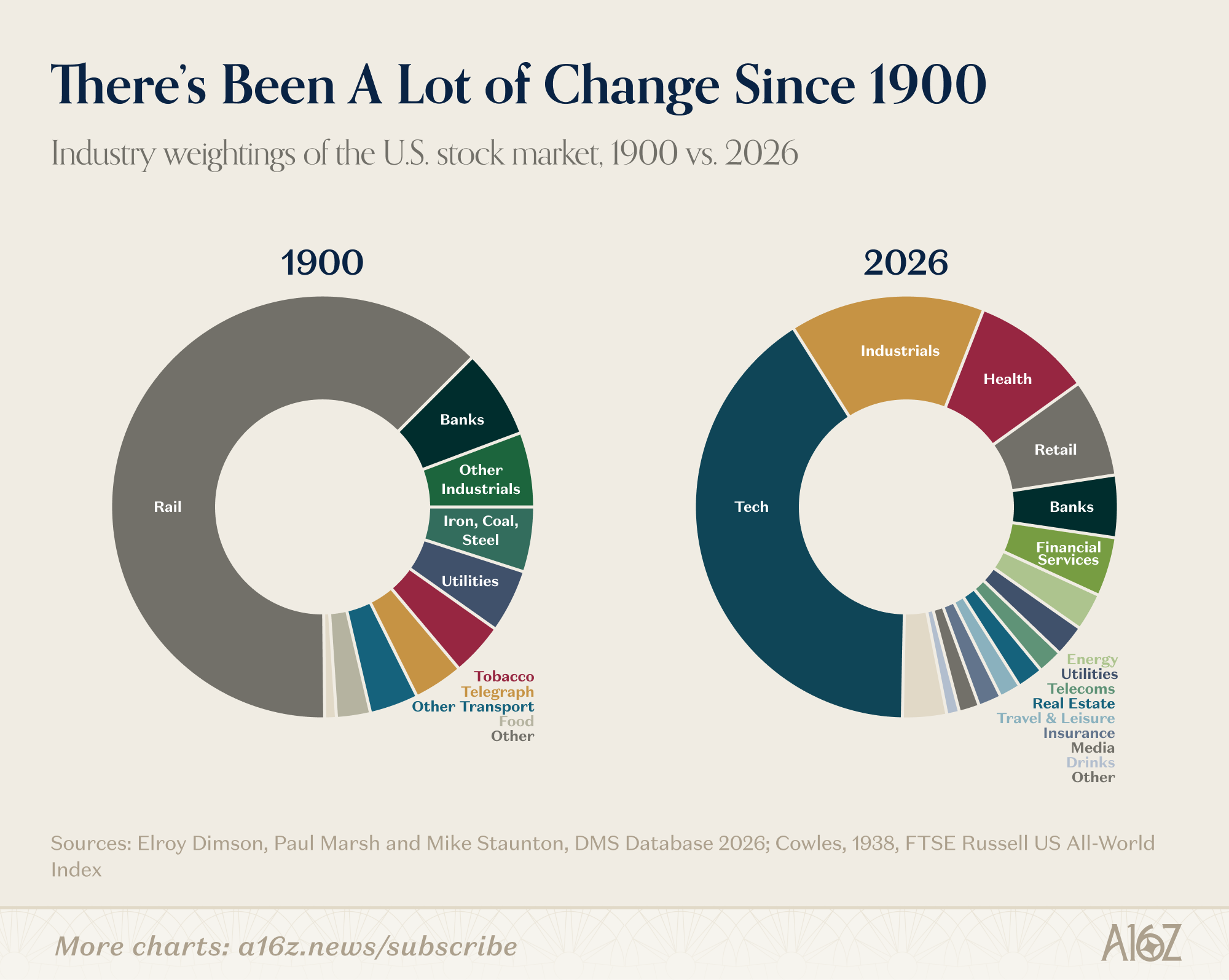

The economy got a lot larger, and a lot more complex. In fact, ~70% of today’s market is in industries that were tiny or nonexistent in 1900.

In 1900, the economy was basically textiles, iron, coal, steel, and tobacco, the rails to transport them, and the banks to finance them. Now those sectors are a tiny fraction of the overall pie.

All of which is to say, the more interesting question isn’t whether such and such platform shift is a bubble, but to consider what new economies might be unlocked by the technological leap forward.

For example, railroads were an incredible General Purpose Technology. One dramatic (but unexpected) change they precipitated was the rise of the modern corporation, as a solution for organizational complexity. Before railroads, a business was usually small enough to fit in one person’s head. But railroads had too many crews, too many stations, and too many simultaneous decisions.

In 1855, the superintendent of the New York and Erie Railroad drew what is now considered the first modern org chart: a layered tree of reporting lines designed to solve the railroads’ increasingly intractable scheduling problems. In many respects, middle management, multi-divisional structure, the professional managerial class, the MBA – all of it – descends from the organizational problems railroads forced into existence.

The point being that railroads didn’t just change what America produced. They changed what the firm was. The railroad-driven emergence of middle management is what Alfred Chandler called the “the visible hand.”

What’s interesting about AI, especially in comparison to railroads, is that AI may once again rewire the dominant organizational template that railroads ushered in over a century ago.

Last month, Jack Dorsey and Block’s leadership published an essay arguing exactly this: the point of AI inside a company isn’t to give everyone a copilot, but to replace what middle management does. Instead of absorb and route information, maintain alignment, pre-compute decisions, etc.—the kind of coordination that management typically is responsible for—in an AI business, humans move to the edges, to focus their judgment on customer contact and human interactions.

In his framing, an 170-year-old model for firm and managerial alignment will be delegated to technology, creating an entirely new type of organization. That seems like a big deal.

Whether Dorsey’s right (and what that new type of firm ultimately emerges) is certainly an open question, but the implications are far more enduring than wondering whether tech will or won’t sell-off its highs, in any given quarter.

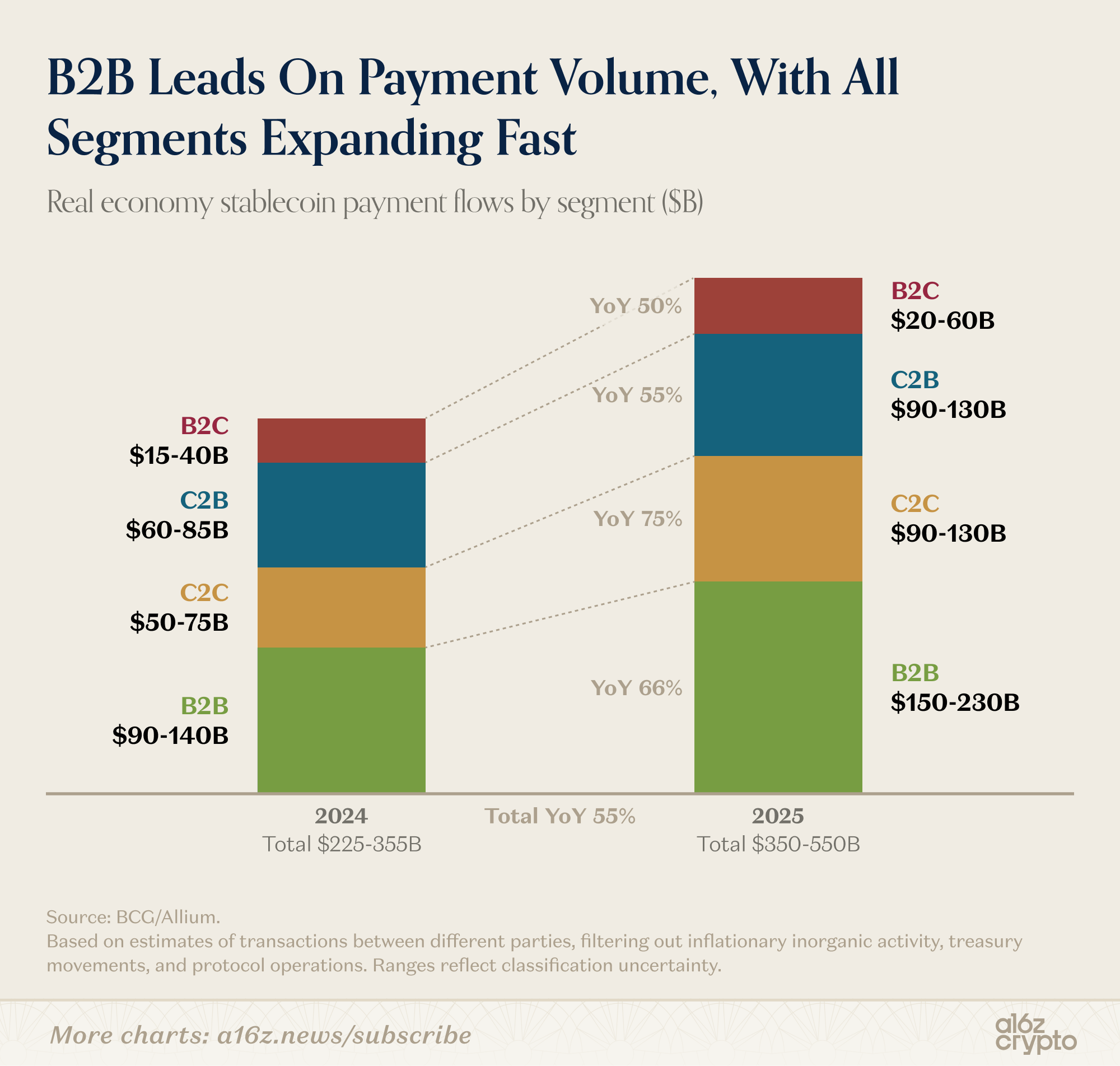

Stablecoins volumes are shifting from transfers to payments

When you strip out things like trading, treasury flows, and exchange mechanics — the bulk of stablecoin transactions — you’re left with an estimated $350–550B in payments between different parties last year.

The business-to-business segment dominates stablecoin payments by volume (unsurprisingly, given the scale), but B2C and C2B are growing, as well.

All of which is to say that stablecoins are increasingly playing a role in ordinary commerce. This is part of a broader shift a16z crypto has writing about here.

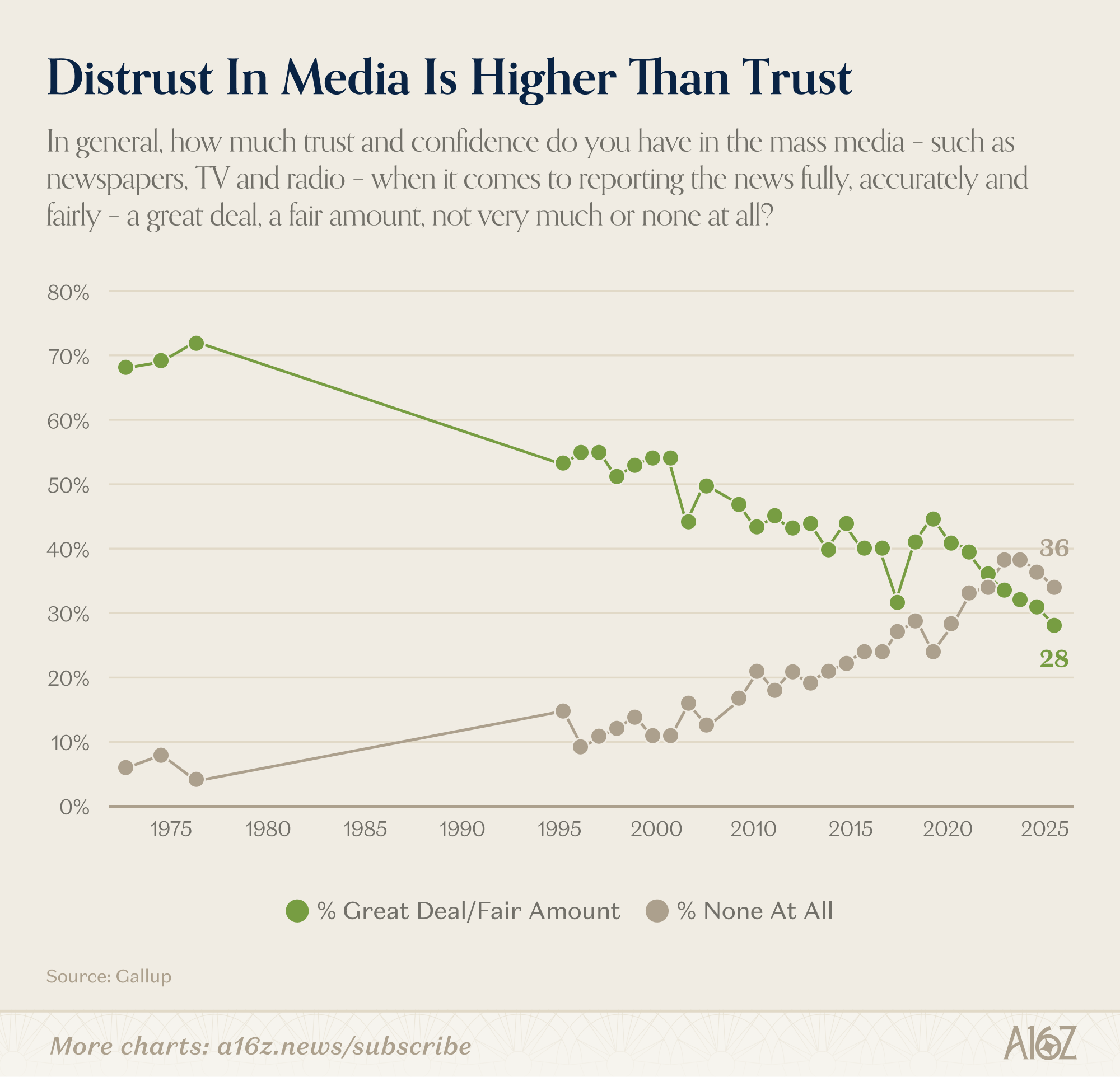

The Next Decade of News

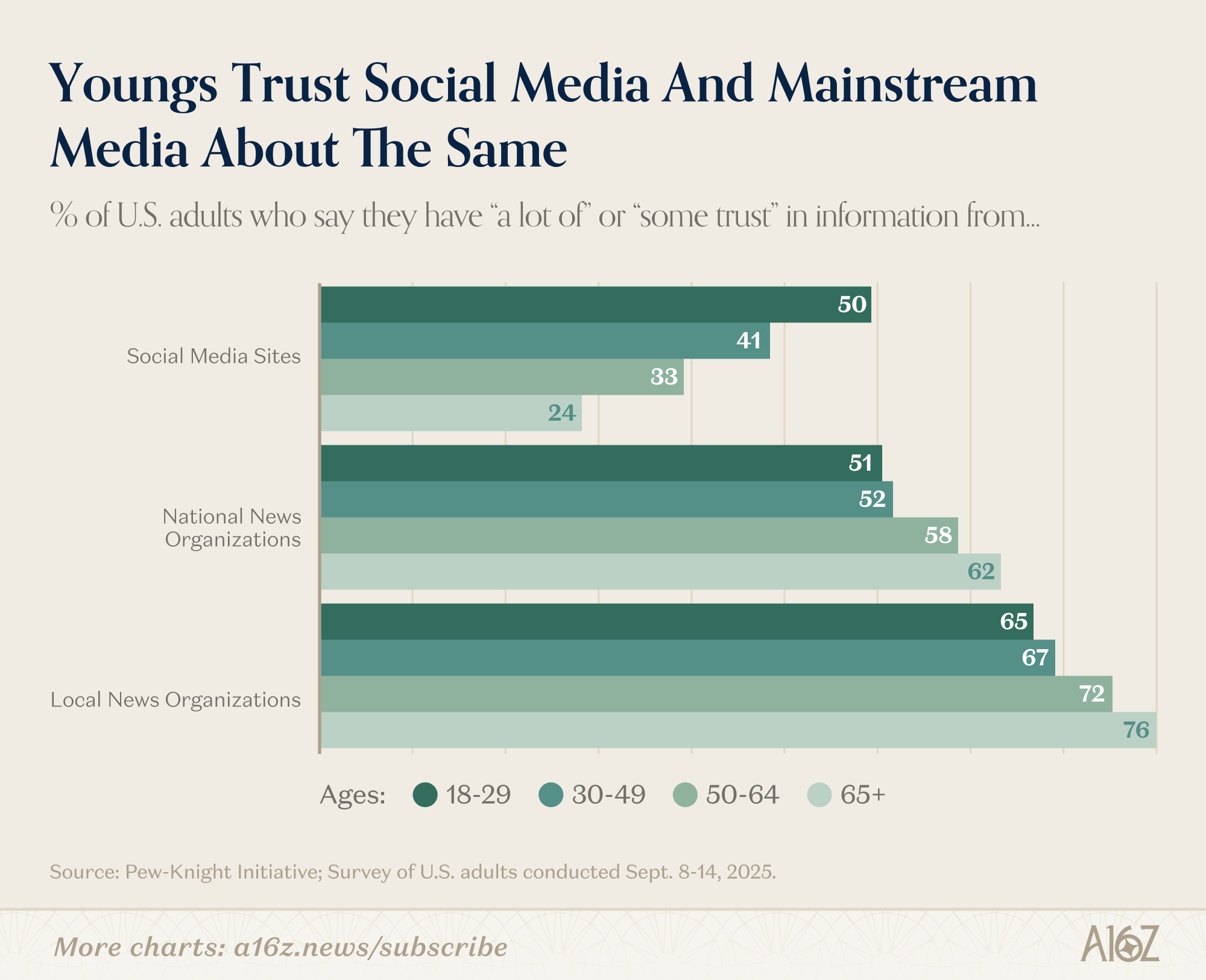

Americans’ trust in mass media recently hit another new low, in one of the great slow-motion collapses in modern polling.

In 2025, only 28% of Americans said they had a “great deal” or “fair amount” of trust in the mass media (e.g. newspapers, TV, radio). In 1975, it was 72%.

The aggregate trust number doesn’t really tell the story, however.

The real story is in the generational splits, which are, in fact, massive:

The younger you are, the less trust you have in traditional media, and the more trust you have in social media (and the opposite is true, as well—the older you are, the more trust you have in traditional media, and the less trust you have in social media).

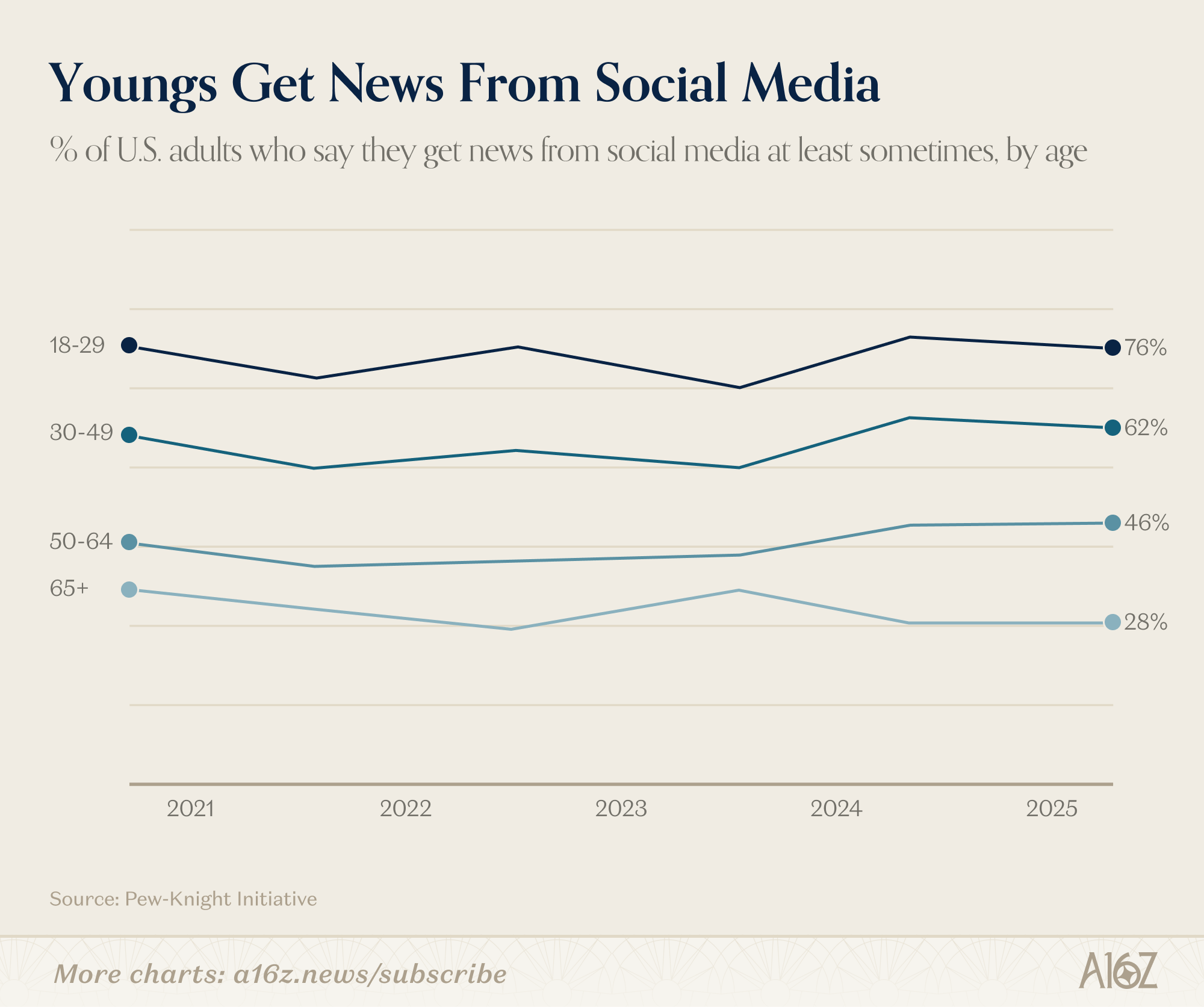

Unsurprisingly, not only is there a trust gap between young-and-old, social media-and-legacy media, but there is a consumption gap, as well:

76% of adults under 30 get news from social media at least sometimes. Among the 65-and-older crowd, it’s just 28% (which is slightly lower than it was ~5 years ago).

So, trust in mass media has certainly fallen off its peak, but a good chunk of the story is explained by the evolving media habits of the younger generations. Relative to their elders, the youngs have much less trust in mass media, and are far more avid consumers of social media alternatives.

Just to return to the original observation, the 72% era of peak media trust is typically remembered as a golden age of journalism. Whether it’s remembered as such, it’s nonetheless also true that the early 70s was a period when only a small handful of networks and newspapers dominated the information-mix, with little in the way of competition.

It’s fair to wonder then, how much of that “peak” trust was about great journalism, as opposed to lack of other alternatives. They’re not mutually exclusive of course—it’s possible that the late 60’s and early 70’s had both great journalism and a captured audience, but either way, it’s hard not to notice that the generation with the least trust for mass media, is also the one who’s come of age with the most alternatives.

That’s the argument Martin Gurri makes in The Revolt of the Public: the collapse of information monopolies across every domain – media, government, expertise – revealed authority that had never been fully earned. Once the public could see behind the curtain, trust fell accordingly.

Gurri also makes the argument that the public is better at tearing things down than it is at building things anew. He may well be right, but at the very least, the capital requirements for building new media alternatives have never been lower. Whether they can rebuild trust in news will be the story of the next decade.

See ya later, productivity gains

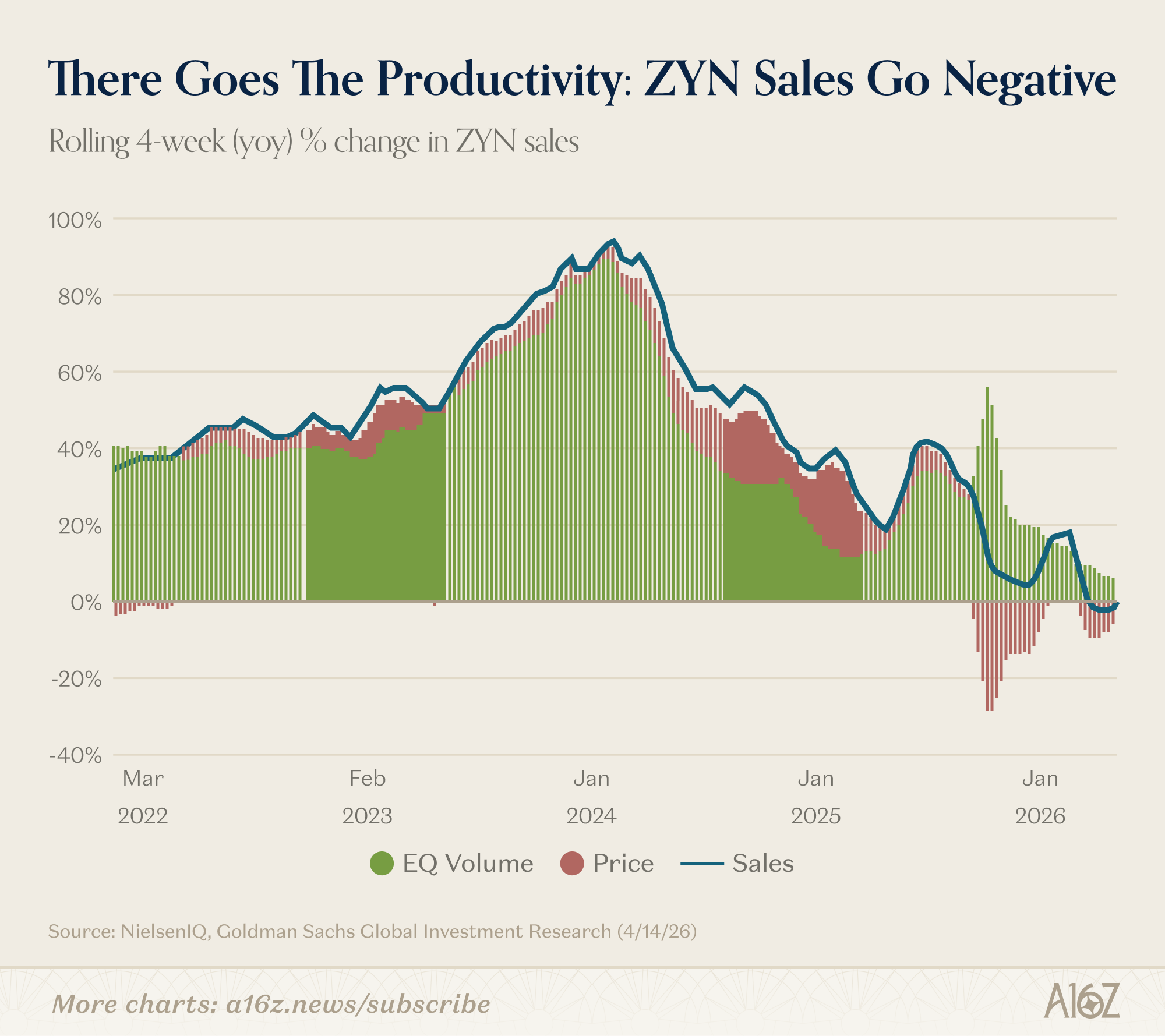

Zyn sales have entered uncharted territory: negative yoy growth.

On a 4-week rolling basis, sales of Zyn were ever-so-slightly negative yoy, for the first time ever.

The truth is, on a volume basis, Zyn sales are still increasing, but given lots of recent promotional activity, the total dollar value of sales was slightly lower.

Productivity gains, fully intact.

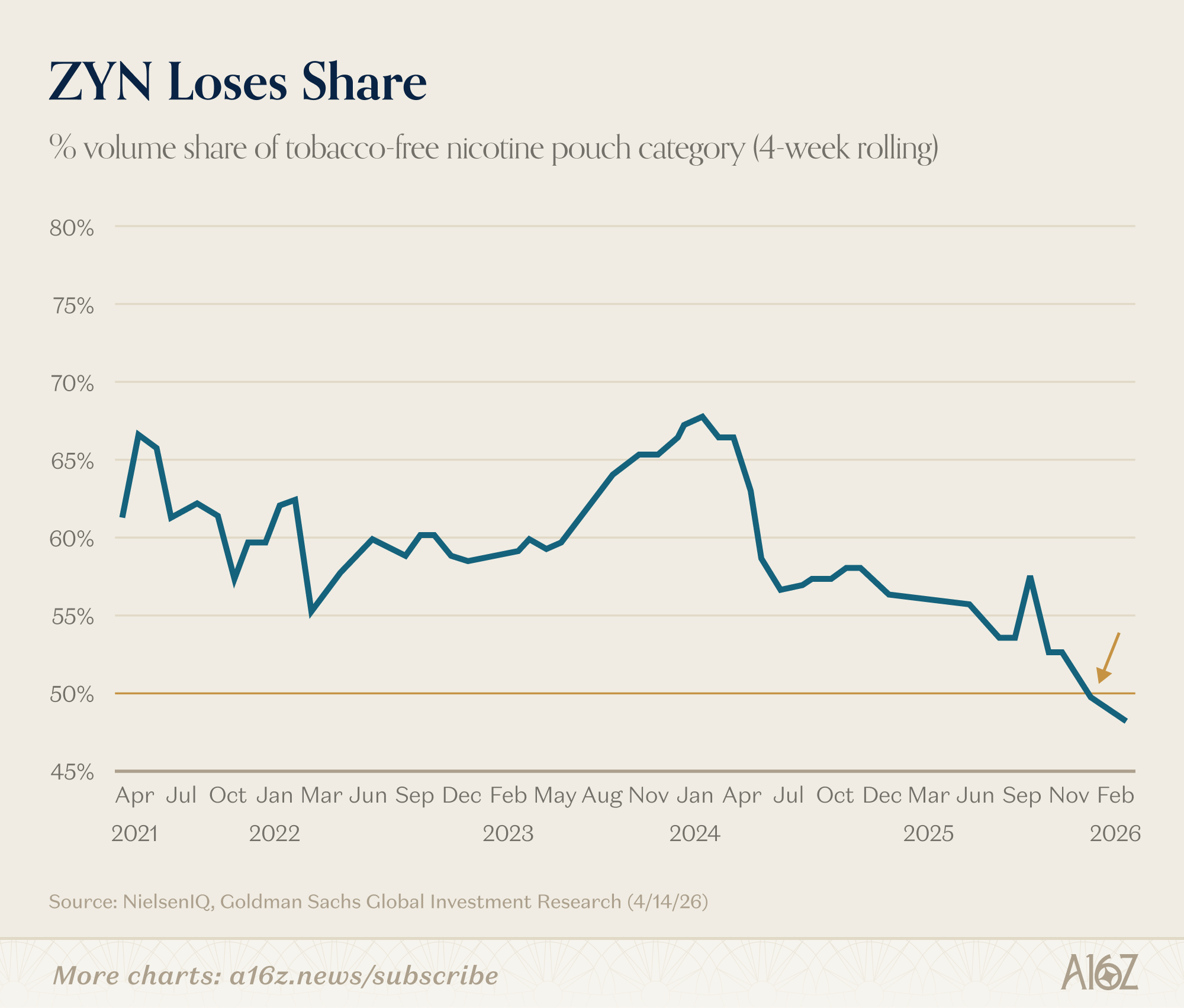

Another interesting aside: Zyn no longer represents the majority of nicotine-pouch sales:

Zyn’s share of the overall market dipped below 50% towards the end of last year.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

Yes, we know, stocks v. flows. It’s a fun visual nonetheless.

What this chart doesn’t show is the speed of the shift. The 1985-2015 gap took 30 years. The 2015-2025 gap happened in 10. Concentration accelerates as winner-takes-most dynamics meet software’s near-zero marginal cost. The next 5 years chart is going to be harder to look at.

In the "media trust" section, how/where are Substack blogs (like this one) categorized? They're certainly not legacy media, but are they actually social media? To me, "social media" means sites like Reddit, X, Facebook, etc.

I would consider Substack blogs to be a separate category. Specialty/niche media, perhaps? I think it's relevant because the news sources I trust are virtually all hand-picked Substack commentaries and newsletters as well as a few independent ones not living on the Substack platform.

I don't consider legacy media or social media to be trustworthy sources, but I will put a lot of weight into what my curated "news and opinion" email feed shares with me.