Charts of the Week: Learning to Weld

The puzzle of youth employment; AI native small business; Who do you think you are, Mr. Big Short?

America | Tech | Opinion | Culture | Charts

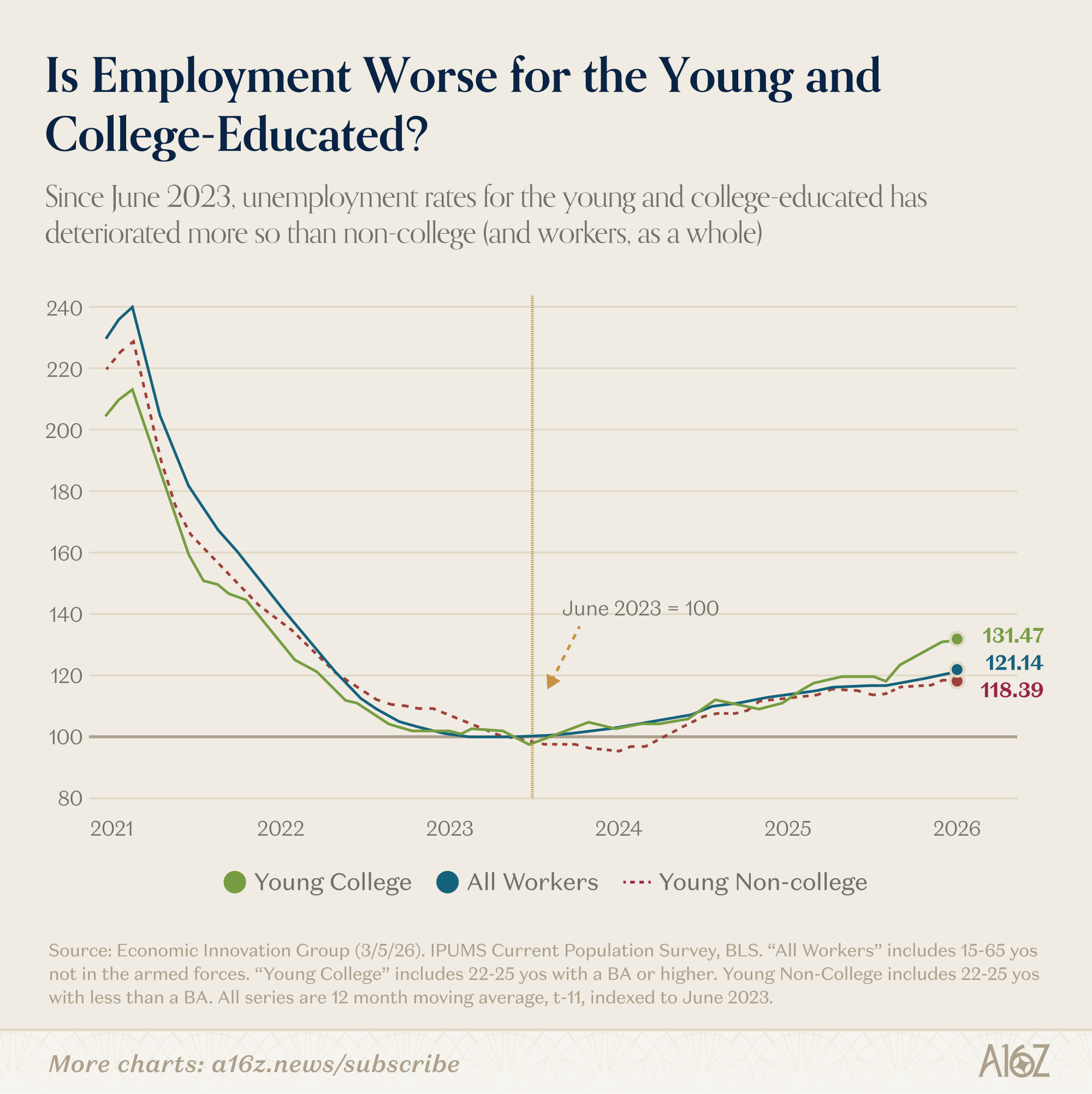

1. It’s a tough job market for young people, knowledge-worker or otherwise

It’s common knowledge at this point that it’s a tough job market out there for young people.

The obvious culprit is AI, which has already vibe-coded all the entry-level white collar jobs into oblivion:

The unemployment rate for young, college-educated workers has deteriorated more so than the field, and certainly more so than young, non-college workers. (Note that this is indexed change, and not absolute levels.)

If it’s the college-educated that are uniquely struggling, then it’s case closed: AI did it. No one needs analysts anymore. White-collar work we hardly knew ye’. This is the end for knowledge work. Blackpills and UBI from here on out.

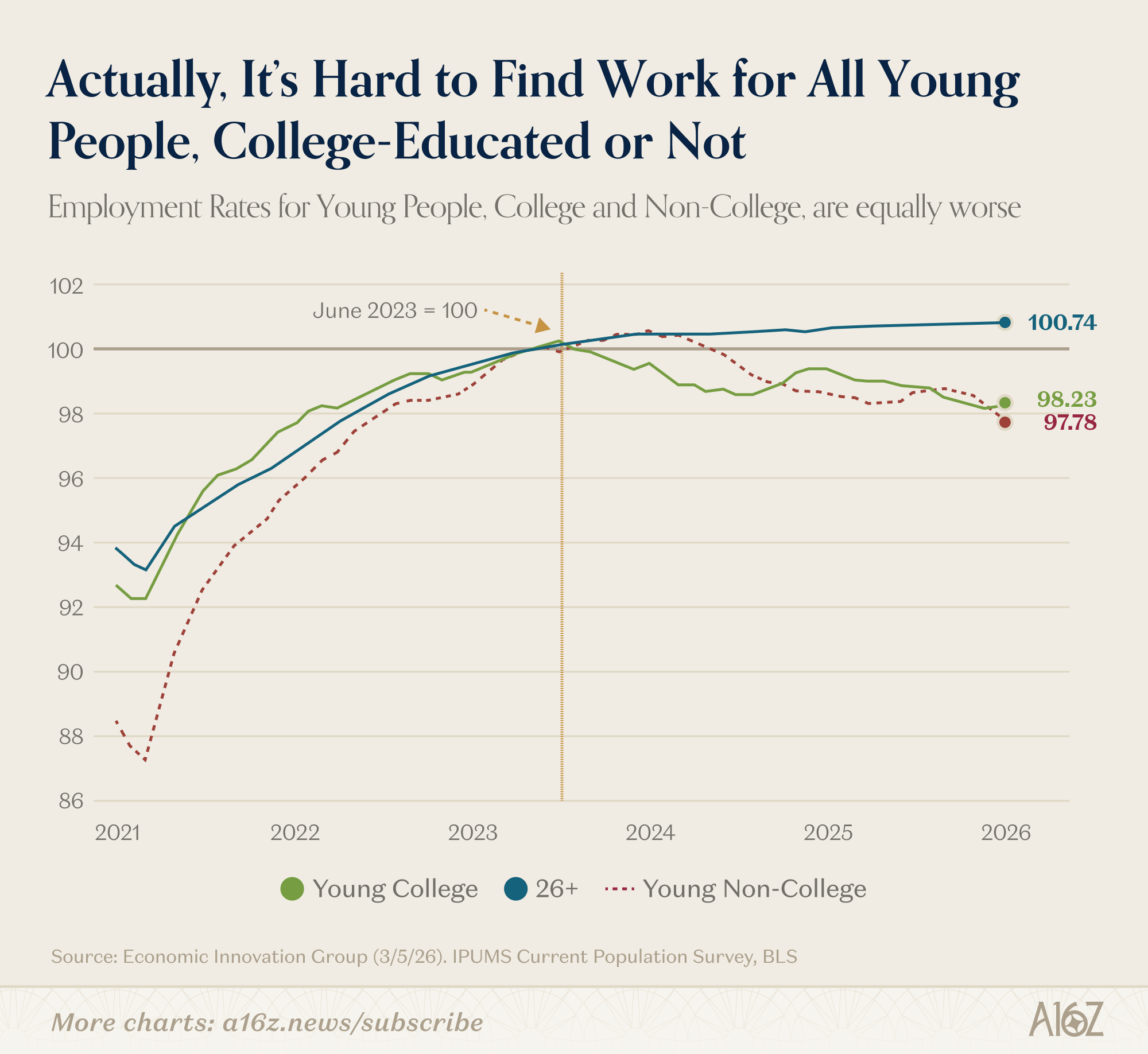

Well, not so fast. The reality is that it’s not just “knowledge work” roles that are hard to find, but you have to cut the data a little differently to see it more clearly.

Take a look at the employment rates for both college and non-college young folks:

Employment rates for young workers, whether college educated or not, have both been in roughly equal decline for the past two years.

When you look at it this way, young knowledge workers specifically don’t appear to be uniquely challenged. It’s just hard out for all young people. There just isn’t that much hiring going on.

Now, the employment rate measures the share of young people in the workforce, but it differs from the unemployment rate in two key respects: (a) it includes people who aren’t actively looking for work (who would otherwise be excluded from the unemployment rate), but (b) still excludes people who are in school (and therefore have a good reason for not seeking employment).

In other words, the employment rate is a more complete measure of employment, especially for young workers. While it might make sense to exclude non-searchers from the headline unemployment rate (because there are many reasons a working age adult might not be looking for work, some good, some bad), it makes less sense for young folks, where college is really the only good excuse.

And, back to the story at hand, if it’s the case that both college and non-college young people are struggling to find gainful employment, then it’s harder to blame AI specifically.

Generally speaking, entry-level non-college work is not the repast of easily-automated workflows—it’s retail, food service, hospitality, and blue-collarish roles, all of which require fully-functional hands and feet, that AI does not yet possess. The point being that it’s not just “knowledge work” that’s hard for young folks to find—it’s all the work.

So, if it’s not AI that’s making the job market hard for young people, then what is it?

Well, it’s hard to say for sure, and it may not be one thing, but first some context:

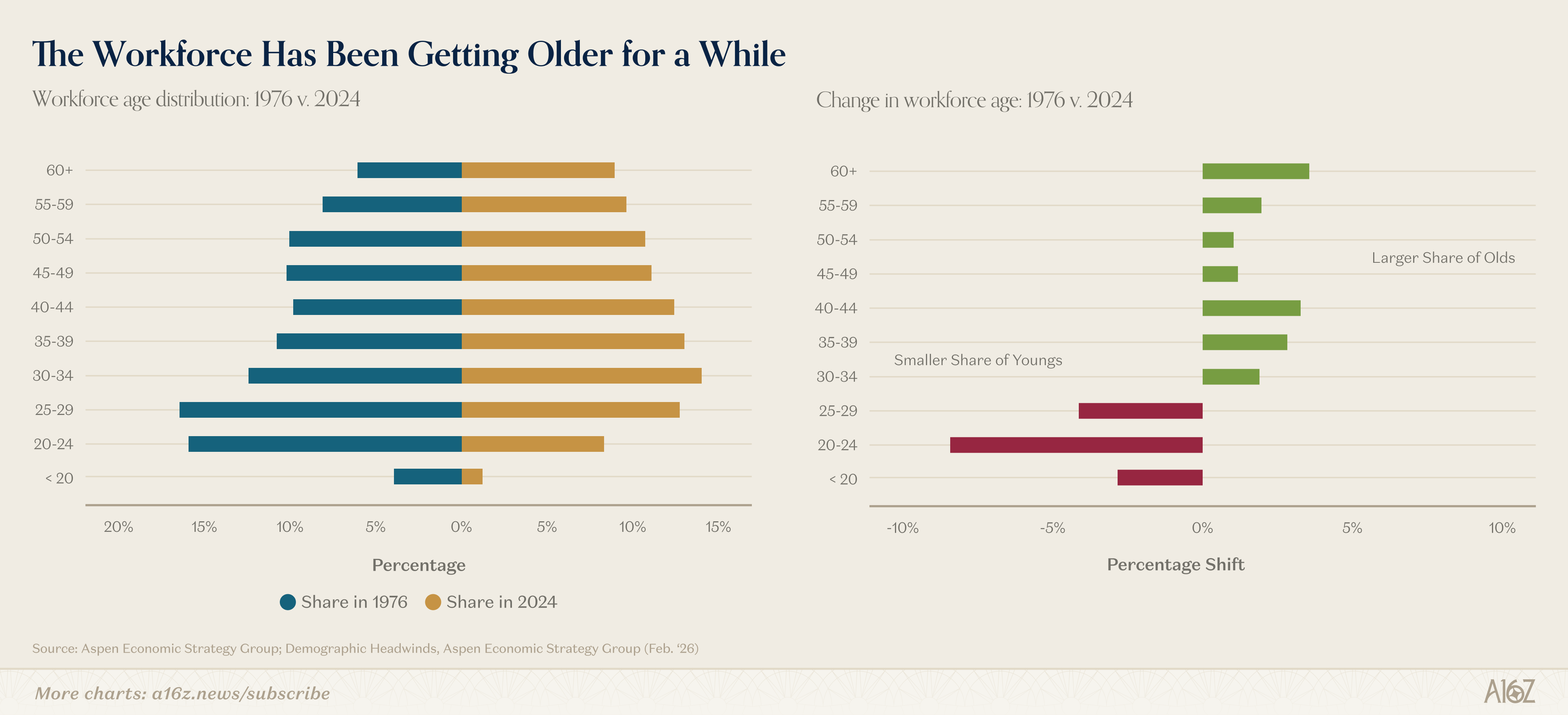

Going back to 1976, the share of 20-somethings in the workforce has declined ~12%.

Young folks, in general, are an increasingly smaller share of the workforce, and that’s been true for a while. A good chunk of the change is driven by the rising college attendance, but other structural shifts play a role too, e.g. the relative decline of blue-collar/manufacturing jobs that might have otherwise been a compelling alternative to college.

Again though, just because the workforce has been skewing older since the 70s, that doesn’t explain why the employment rate for young people has declined very recently—especially because the employment rate excludes people currently in school. It may be that college has become less-appealing recently to young people, and the workforce hasn’t adapted to that shift, just yet—that’s certainly possible, but some other data suggests that perhaps a different dynamic is at play.

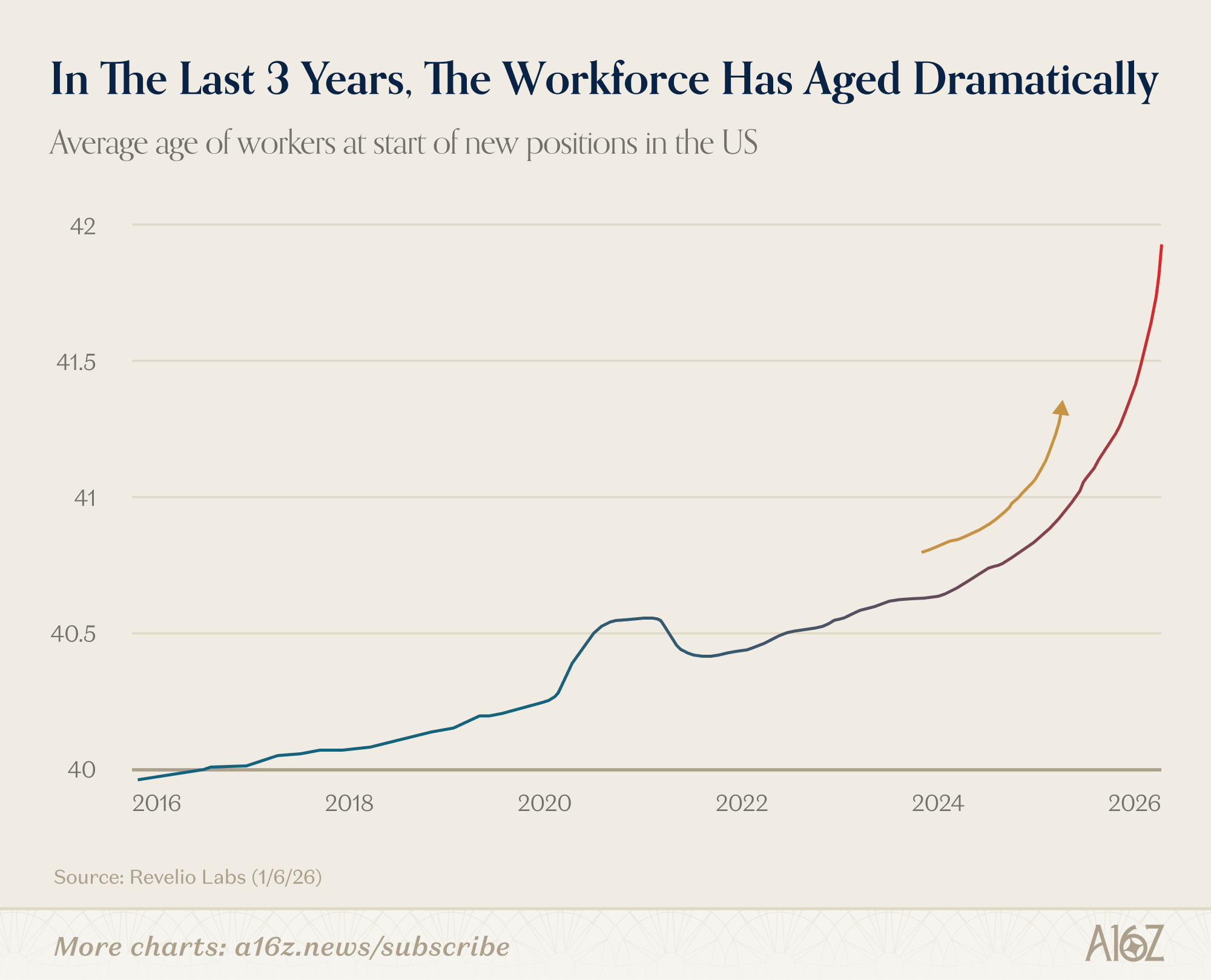

One thing that’s changed quite recently is that the age of the workforce has increased fairly dramatically since 2025

The workforce had been getting steadily older by ~1 year every 5, but that pace accelerated ~5x in 2025, when the average age jumped a full year, in just a year’s time.

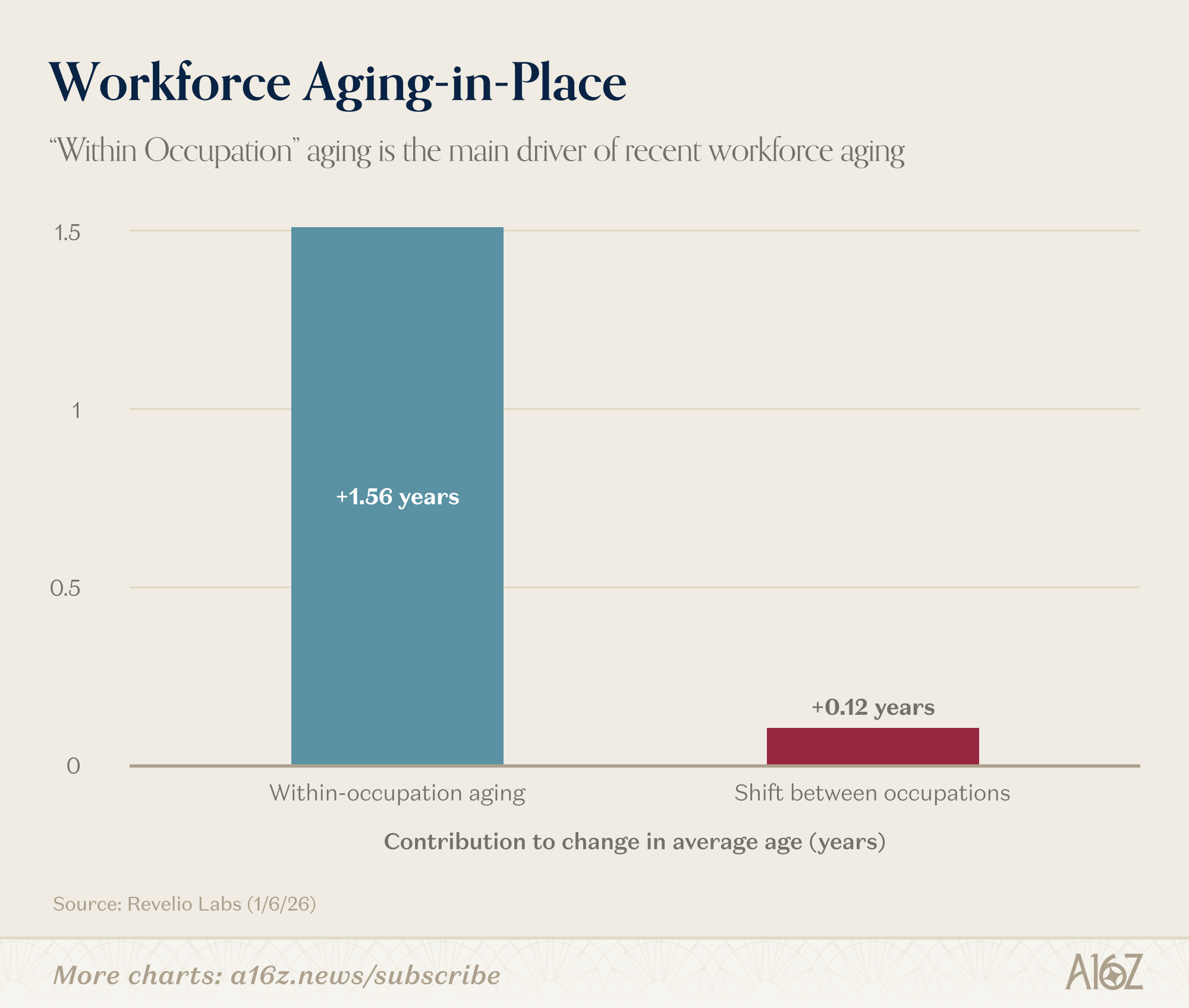

Some of that aging is explained by the lack of entry-level hiring, but it turns out that another part of what’s happening is that people are staying in their jobs (and in the workforce more generally) longer than they used to:

“Within-occupation” aging explains almost the entirety of the recently older workforce, at least according to Revelio’s data.

If job-switchers were getting older too, then workforce aging might reflect some demand-shift to more experienced workers (which is true in some narrow cases, but not more generally). The fact that nearly all of the aging is “within-occupation,” indicates that people are simply less-inclined to retire. Along similar lines, other data shows that “working lives” have extended by ~1.5 years, and that retirees are increasingly coming off the bench to reenter the workforce.

Putting it all together, and while we can’t say for sure, it’s possible that one of the reasons hiring is rough for all kinds of young people is that older folks are simply working longer than before. While it’s generally a mistake to think of the labor market as a zero-sum game, if the off-ramp gets extended, it stands to reason that the on-ramp may get backed-up, as well.

So, don’t blame AI for the lack of entry-level jobs—perhaps blame old folks for working too hard, instead.

2. Learn to weld

Staying on the jobs theme for a moment, but now we’ve got some good news.

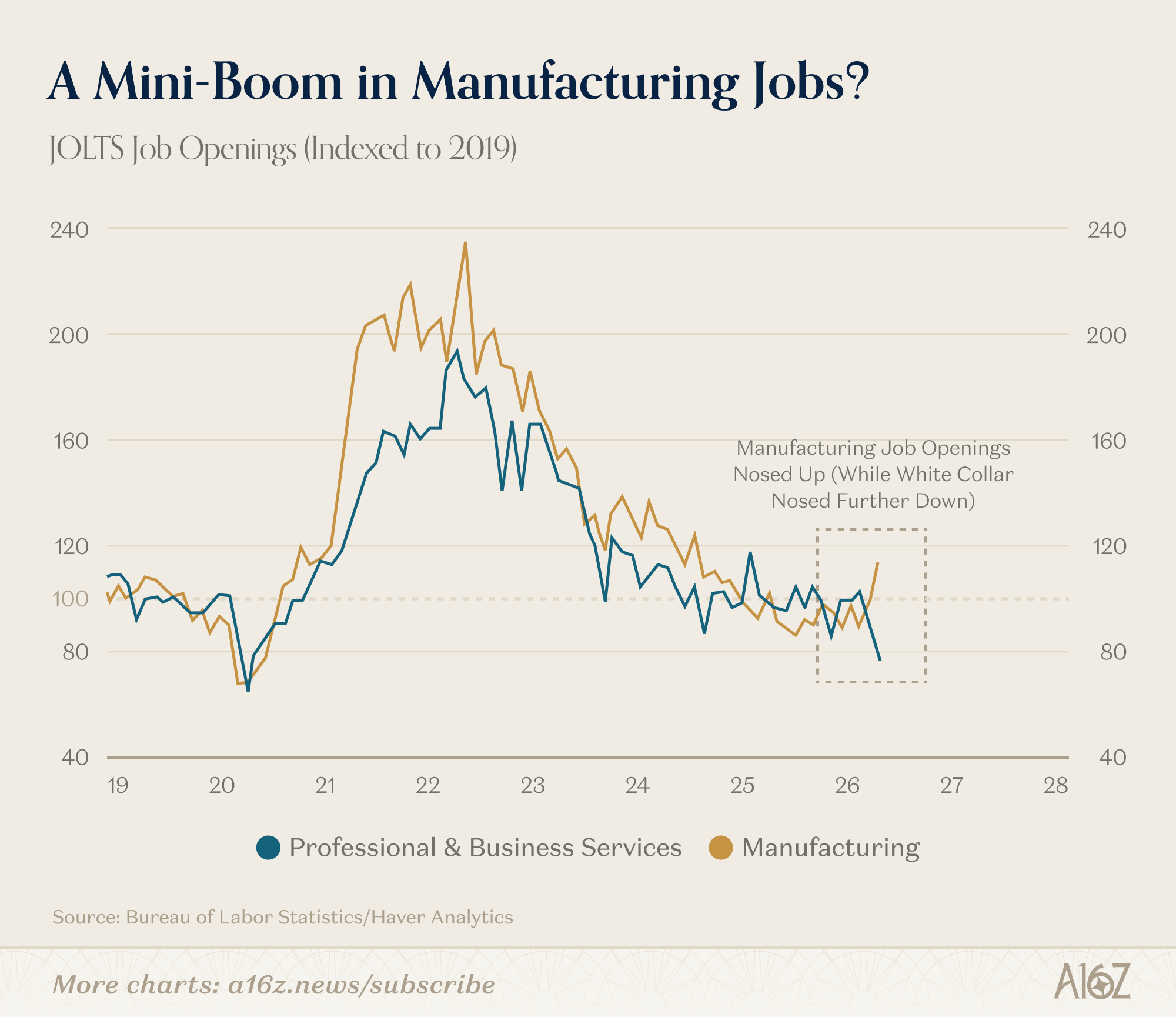

The change is subtle, but manufacturing jobs appear to be on the rise:

Manufacturing job openings increased slightly in the beginning of 2026, in contrast to white-collar roles, which continued their 3-year decline.

A rise in manufacturing roles should be welcome news for entry-level hires, which have gravitated towards blue-collar work in the past. What’s causing the manufacturing job boomlet? Well, it’s probably got something to do with AI-the-job-maker. Or rather, the infrastructure build-out, more generally.

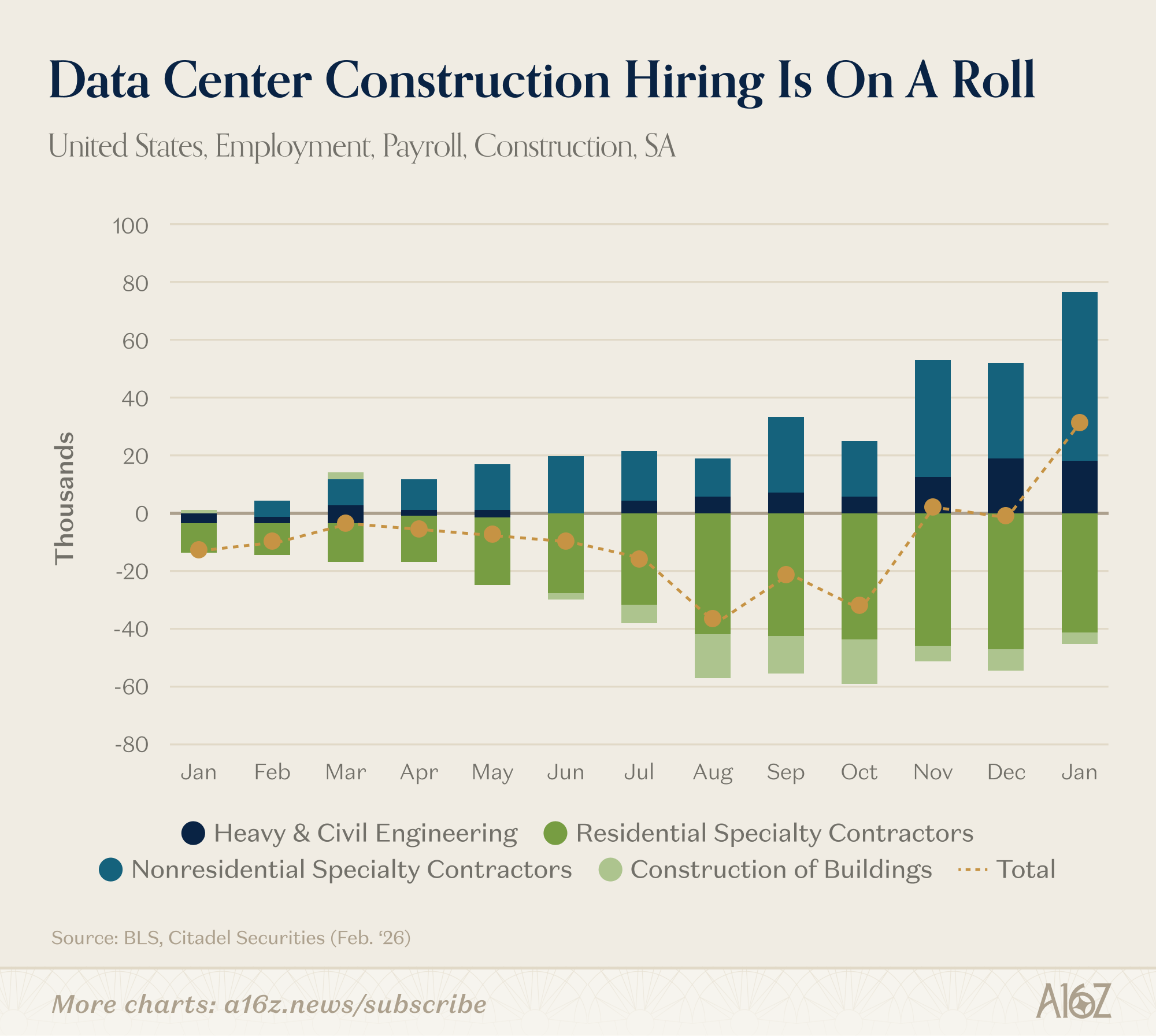

We already know that data centers are driving hiring for construction workers, and specialty construction, in particular:

Non-residential specialty contractors and civil engineers—the kinds of people involved in industrial construction—have been in hot demand, in contrast to residential construction hiring, which has been in decline for over a year.

Construction and manufacturing are not the same, but you can’t build data centers (or upgrade the grid) without all kinds of heavy equipment, parts and machines, i.e. the sorts of things that manufacturers manufacture. It makes a lot of sense that surging AI buildouts might also increase demand for manufacturing.

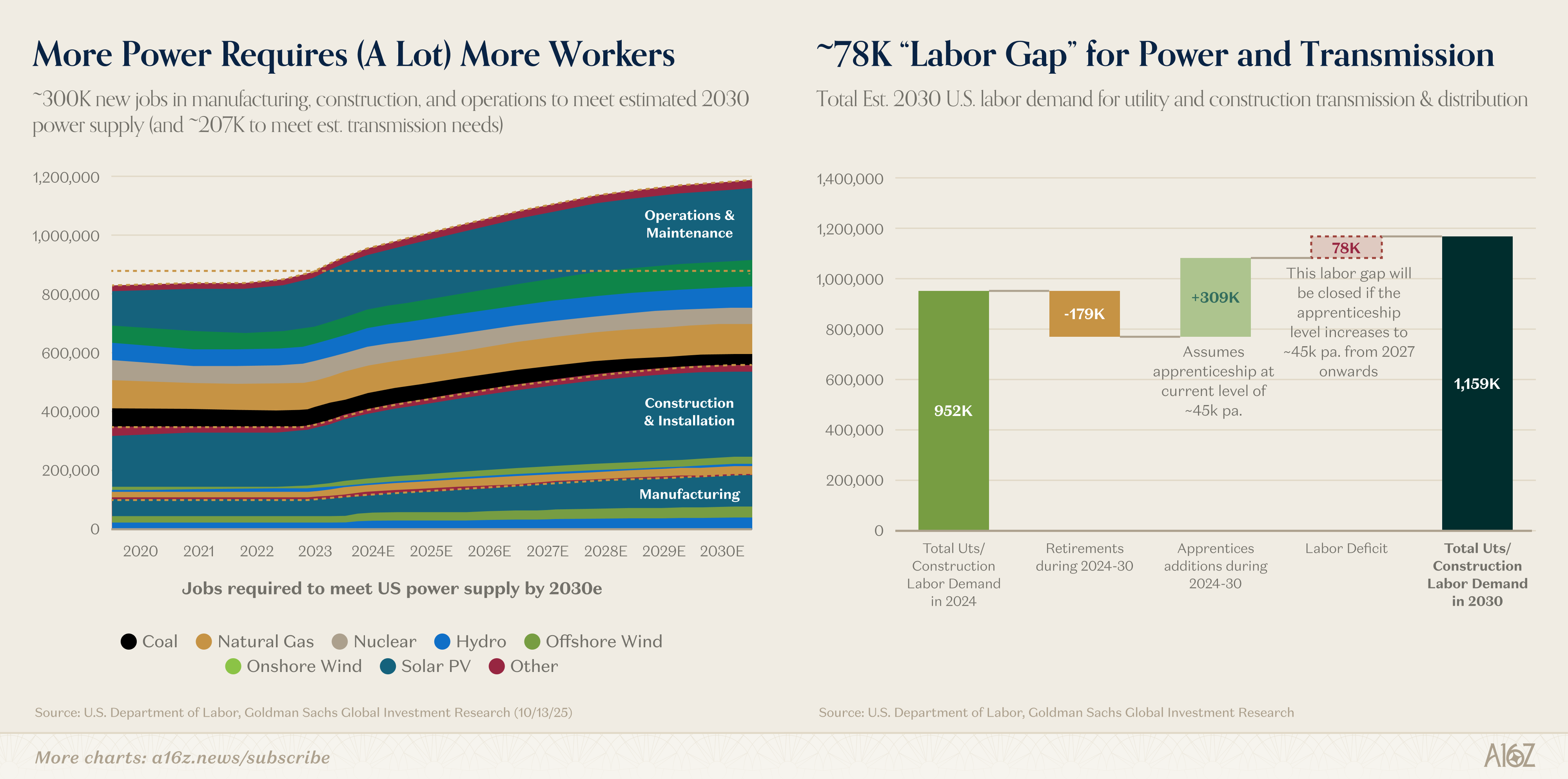

By some estimates, the (re)industrial renaissance is going to need so many new manufacturing, construction, and operational workers that we’re not going to have enough to go around:

Goldman Sachs estimates an additional ~500K jobs are needed to achieve the buildout, leaving a ~78K “labor gap,” (even assuming that 100% of apprentice roles gets allocated to the sector).

The shortage of skilled tradespeople has been a thing for a while now, both as demand for “blue-collar” expertise increases, but also as the existing workforce gets older. Add a few hundred thousand new AI-infra jobs to the pipeline, one can only imagine that the shortage will get worse. Certainly that’s what Goldman Sachs thinks, at least.

To all the struggling young folks out there, we’re not saying the solution is “learn to weld,” but we’re not not saying it, either.

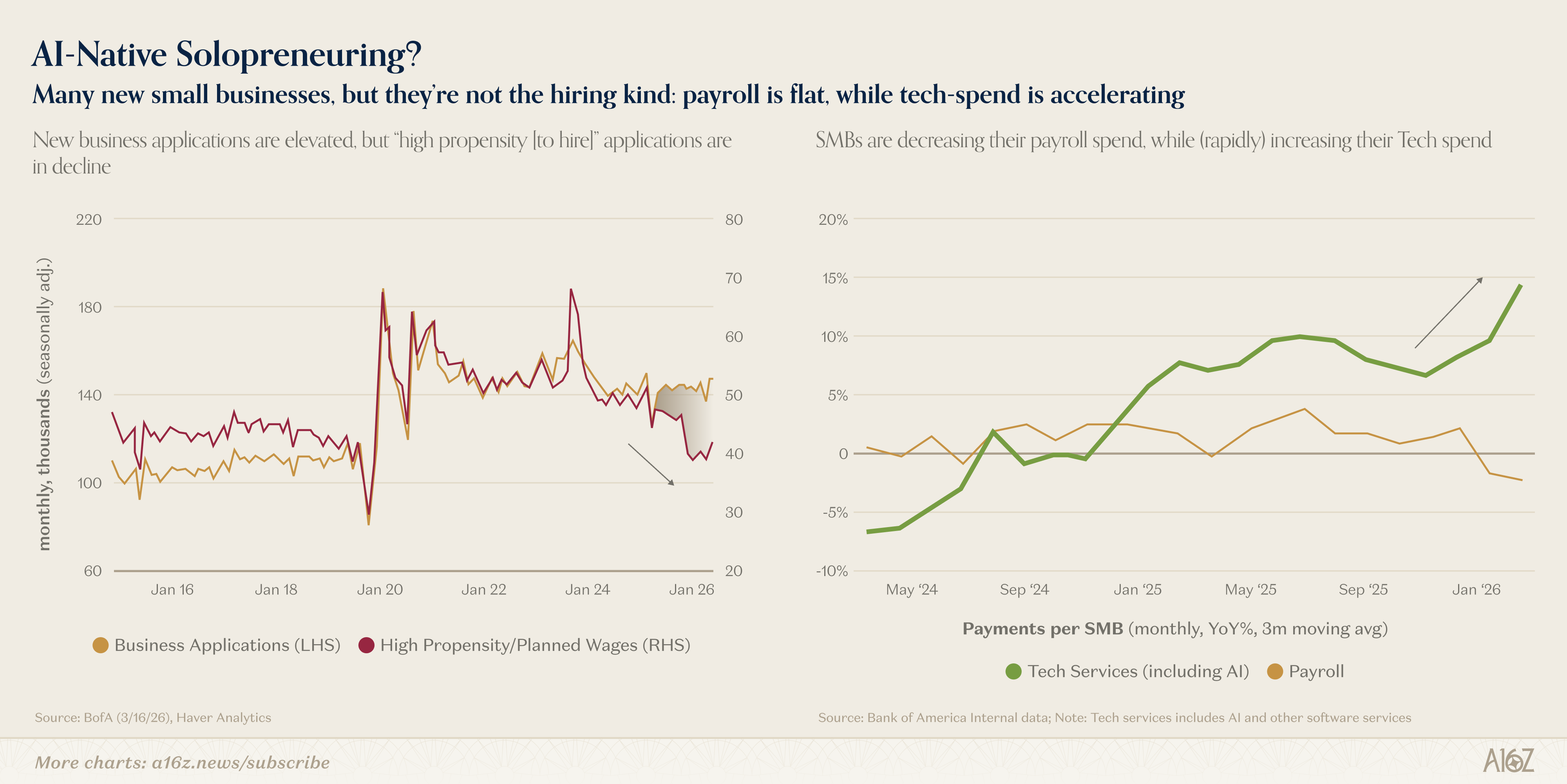

3. Rise of the AI native small business?

We’ve all heard of the one-person billion dollar company coming to a vibecode terminal near you. With agents orchestrating agents orchestrating agents, a lone determined founder now has the operating leverage to build and operate a massive company without a single (other) employee.

It hasn’t happened yet, of course, but the possibility isn’t so far-fetched.

What has happened, however, is that lots of new small businesses are forming, and while they’re not hiring much, they are spending a lot on technology:

New business applications are elevated, but “high propensity [to hire]” business applications are in decline.

At the same time, SMB payroll expenses are flat-to-down, while tech-service spending keeps trending up.

So, the data shows lots of new business formation, but it’s of the “non-hiring” type, and while small businesses aren’t adding much payroll, they are spending a lot more on tech.

Is this the early innings of AI-native solopreneuring? Who knows, but we can’t wait to find out.

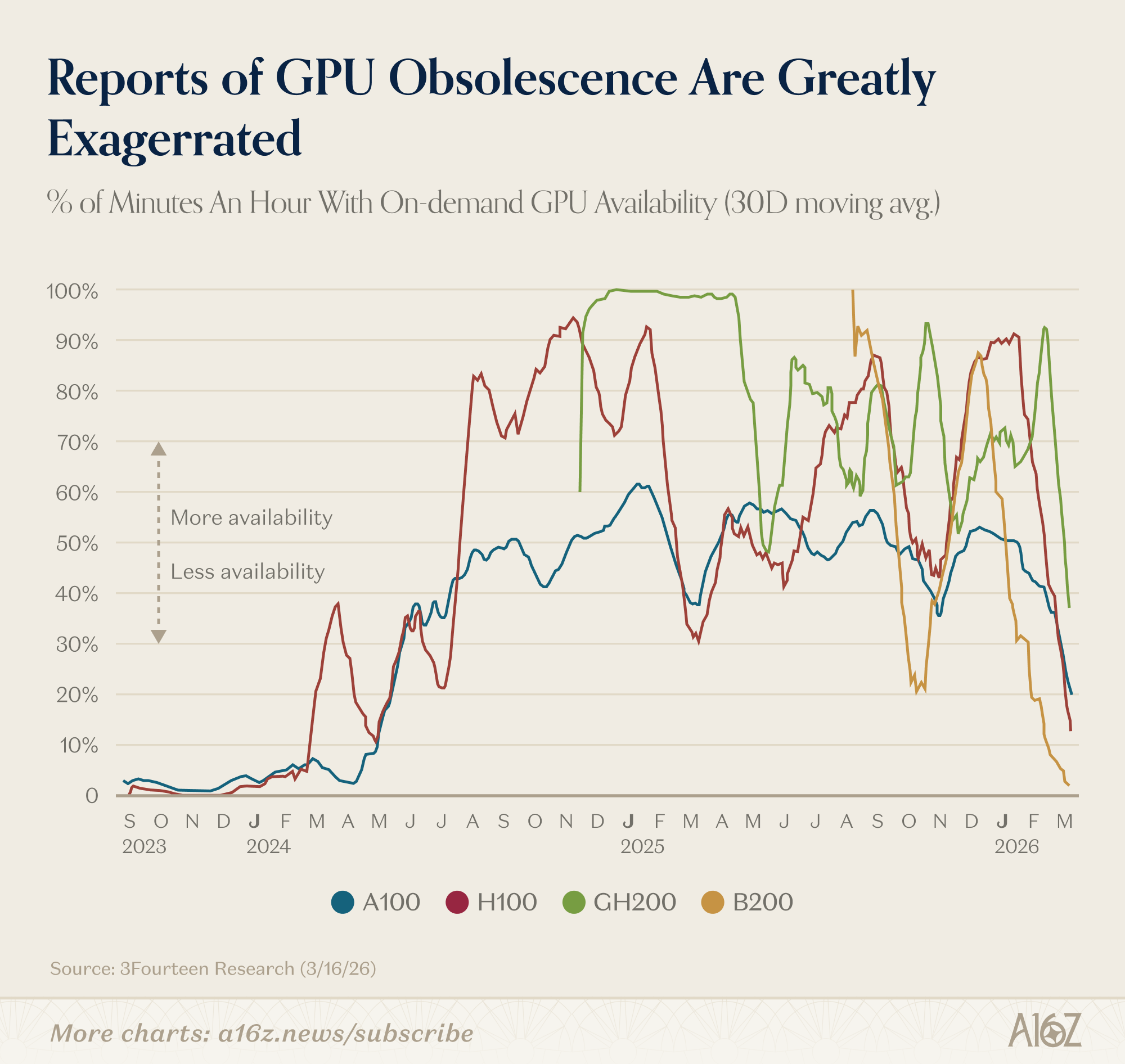

4. Who do you think you are, Mr. Big Short?

Every now and again, the doomers wonder “but what will happen to all the old GPUs?!”

It’s a fair question, for sure. The Big Shorter himself (aka Michael Burry) said the hardware should depreciate in 2-3 years (and not the 5+ years that hyperscalers are currently modeling). If new GPUs come out so quickly, then they must make the old GPUs obsolete, just as quickly.

Checkmate, hyperscalers. The bubble is going to burst, any moment now.

Maybe one day, but not today, Mr. Big Short, not today:

According to data tracked by 3Fourteen Research, since late 2025, “on demand” GPU-availability has gotten scarcer and scarcer—for the latest B200s, it’s basically non-existent. If you need on-demand GPUs, your best bet is the GH200, which is still only available less than 40% of the time.

Perhaps next month will tell a different story, but for now, if older GPUs are going obsolete, someone should probably tell whomever is burning all that compute that they’re wasting their time.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

The reason older people are not leaving the labor market is because they have not saved enough for retirement in the 401ks that replaced the pensions which employers dumped, and a rising cost of living vs fixed income. They are not staying in for the love of the job.

131.47? how about you label your charts axes