Charts of the Week: DExit . . . real or feigned?

Jevon-it; Capex in context; Kalshi Forecasting the Fed Funds Rate; Delayed Onset of Adulthood

America | Tech | Opinion | Culture | Charts

DExit . . . Real or Feigned?

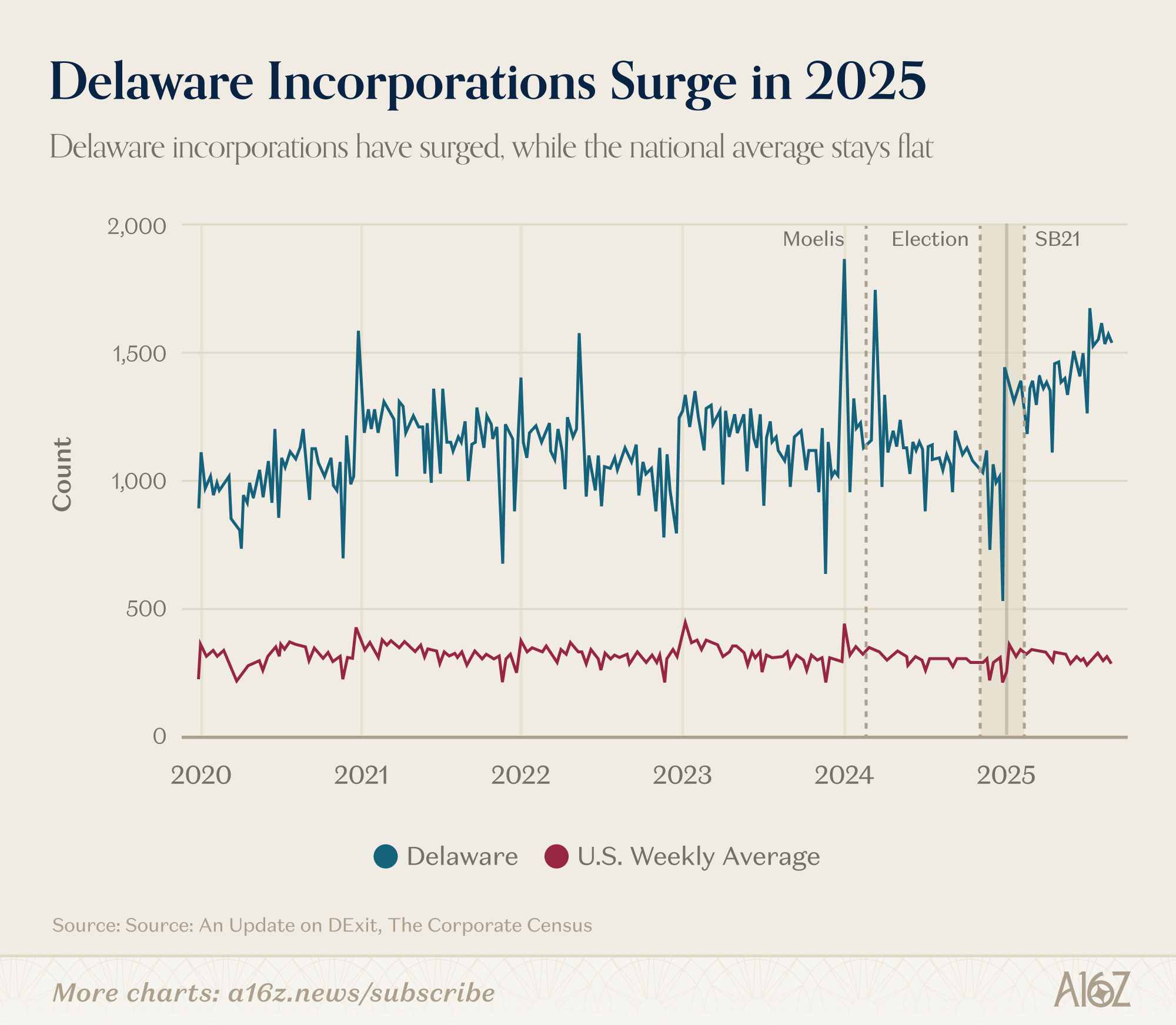

Delaware is still the home state for corporate America, but increasingly less-so:

According to Ramp’s data, Delaware’s share of new incorporations has been declining since 2023, and fell by ~10% in Q3 ‘25.

History doesn’t repeat, but it does rhyme . . . maybe.

Delaware wasn’t always the corporate mecca.

A little over a century ago, Delaware supplanted New Jersey—the original “mother of trusts”—as the go-to jurisdiction for incorporation. The catalyst for ex-NJ flight was then Governor Woodrow Wilson’s effort to reign-in “corporate abuses,” which made NJ a much less friendly place to do business. Delaware, which had modeled its corporate law after NJ’s pre-Wilson regime, was more than happy to welcome corporate refugees, and then together with the Delaware Chancery Court, spent the next 100 years building a reputation as a sophisticated and fair place for firms and investors to resolve their disputes.

What took a century to build, though, has only taken a few years to break. Rightly or wrongly, the Delaware Court of Chancery has recently taken a more permissive approach to shareholder litigation (especially in a few high-profile cases, including Tesla, but not only Tesla), and companies are beginning to literally take their businesses elsewhere. Good night, and good luck, Delaware.

That’s the conventional story, at least, but other data suggests a more complicated picture.

First, even the Delaware founding myth isn’t quite right.

It wasn’t until the 1980s (i.e. 60 years after Gov. Wilson) when Delaware finally overtook NJ as the incorporation capital of America:

New Jersey reigned supreme for far longer than the conventional narrative would have it. The catalyst for the eventual Delaware takeover was probably Delaware’s adoption of certain laws related to director liability that made it especially popular for public companies. That, and increasing network effects, which took on a momentum of their own.

Second, whatever may be happening with high profile public companies (and the companies in Ramp’s data), overall Delaware appears to be doing just fine. Better than fine even:

According to data published by the Harvard Law School Forum on Corporate Governance, Delaware has grown its share of total corporates pretty dramatically since the end of 2024 (and through 2025).

In fact, if you wanted to find a single clear example of “DExit,” it’s probably this, and it’s got nothing to do with Tesla, and instead relates to a specific corporate form:

Wyoming LLCs took off like a rocket ship around 2015.

Why? It probably has to do with certain asset- and privacy-protection specific to Wyoming LLC law that the state itself has marketed as the “cowboy cocktail” entity structure.

Anyways, the point here isn’t to say that DExit isn’t happening (because at least some data suggests that it is—and even a small number of high-profile decampments is significant), but the story is surely more nuanced than the conventional narrative would make it seem.

The reality is that Delaware still enjoys the benefit of being the default option, not to mention all the network effects that come with it, and those can be very hard to shake.

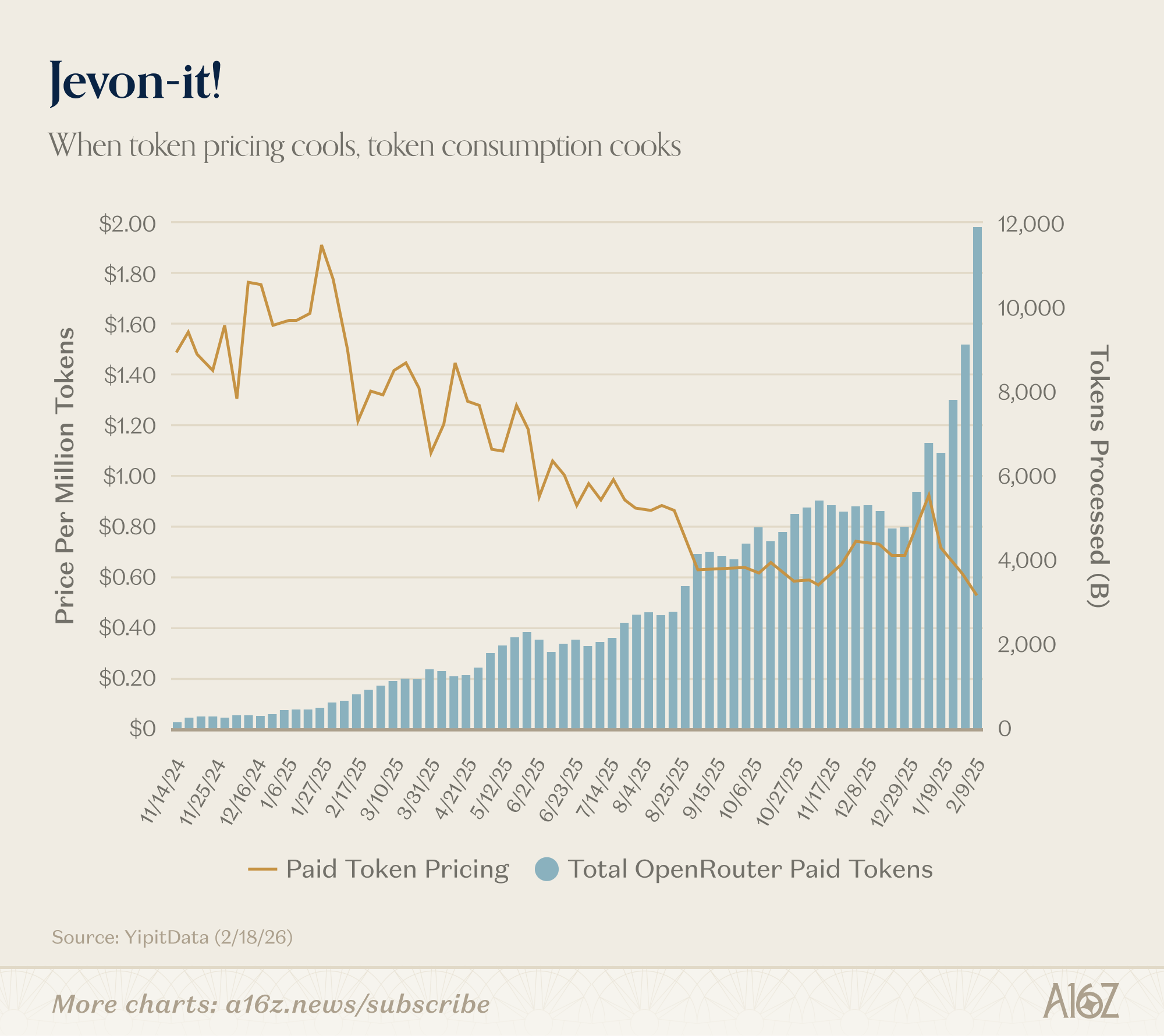

Jevon-it

We’ve published an older version of this chart, but with more data, the look is even more impressive.

When token-cost goes down, token-consumption goes up:

Since the beginning of the year, “paid token pricing” declined from ~90 cents per million to ~50 cents per million, while tokens processed nearly doubled, from ~6,000 to ~12,000.

That’s a Jevonian relationship right there. The cheaper it gets to AI, the more AI we get. You love to see it.

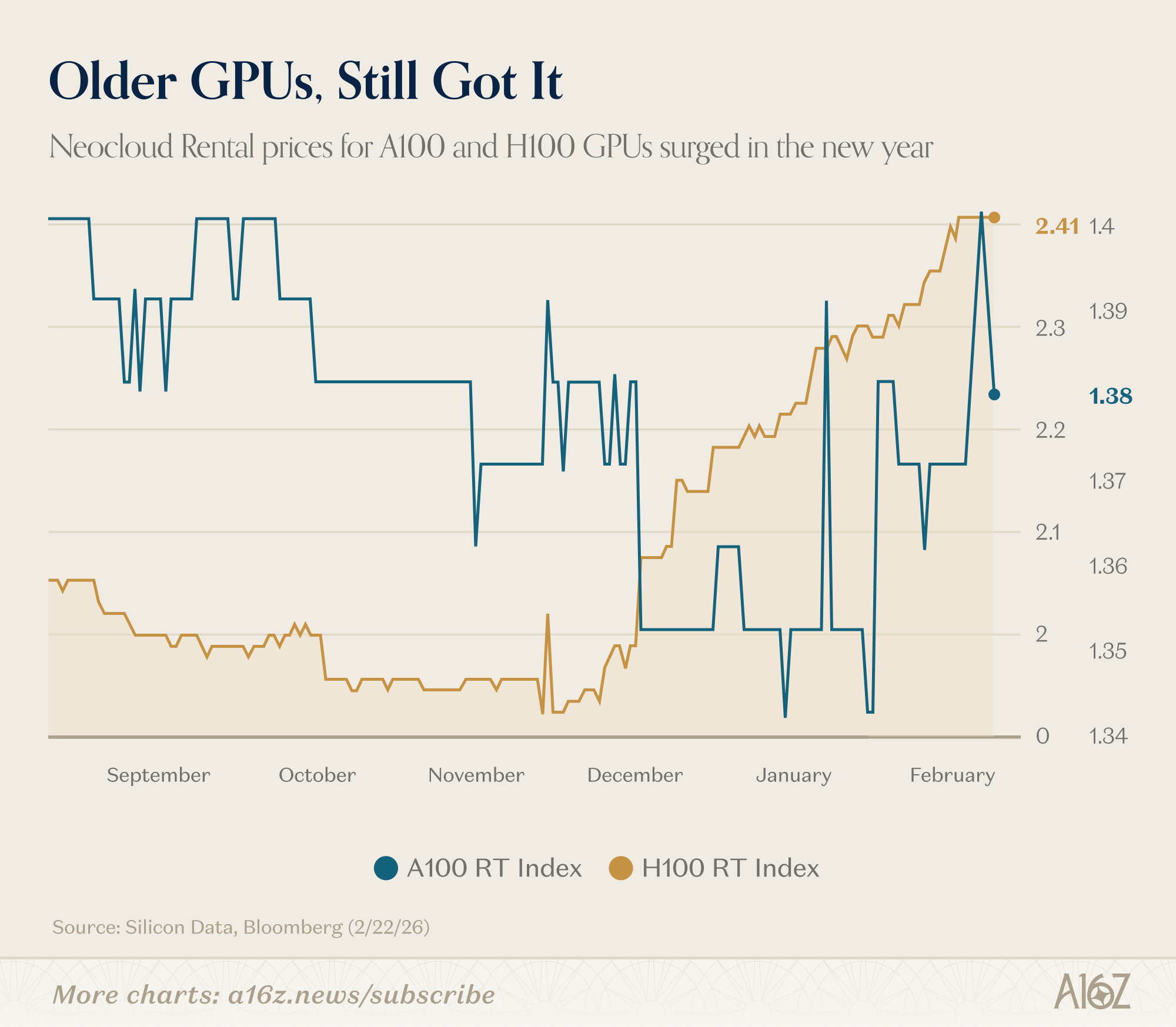

Remember how no one would want to use the old GPUs when the newer, better ones came to market?

That too does not appear to be the case:

Rental pricing for both Nvidia’s H100 and A100 has been increasing this year, according to data from Silicon Data.

Far from flooding the market with more compute than it can use, it continues to seem like the market is barely scratching the surface of what it might do if given the chance.

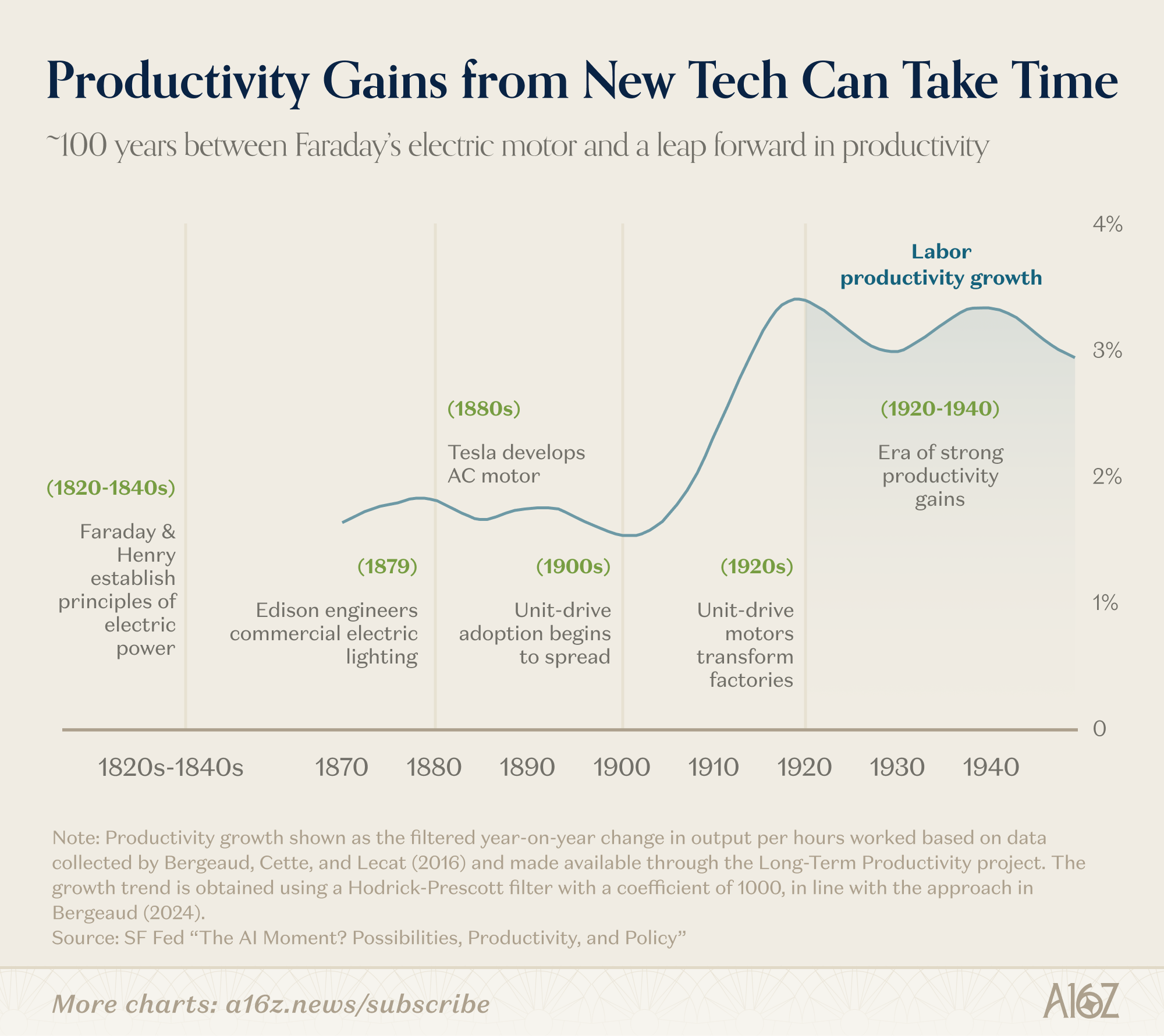

It’s not a perfect comparison, but if history is any guide, it may take some time before we really know what an “AI-driven” economy looks like:

It took ~100 years from when Faraday and Henry first began talking about electric currents to unleash the industrial productivity wave in the first half of the 20th Century.

Cycle times have sped up since the 1820s, for sure, but there’s still an awful lot of moving parts involved in a platform shift, like this one.

What’s that thing that Roy Amara liked to say? “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.”

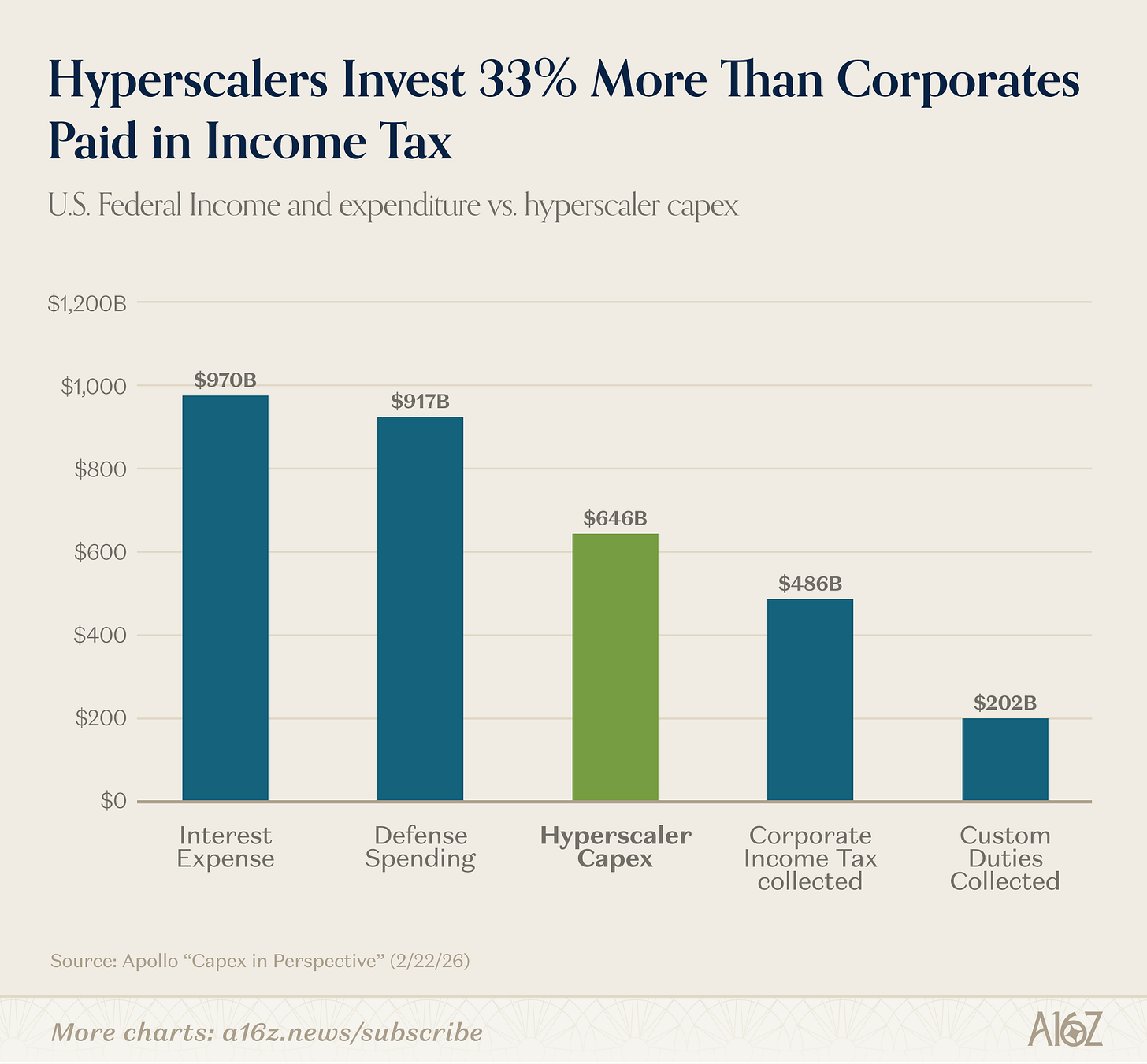

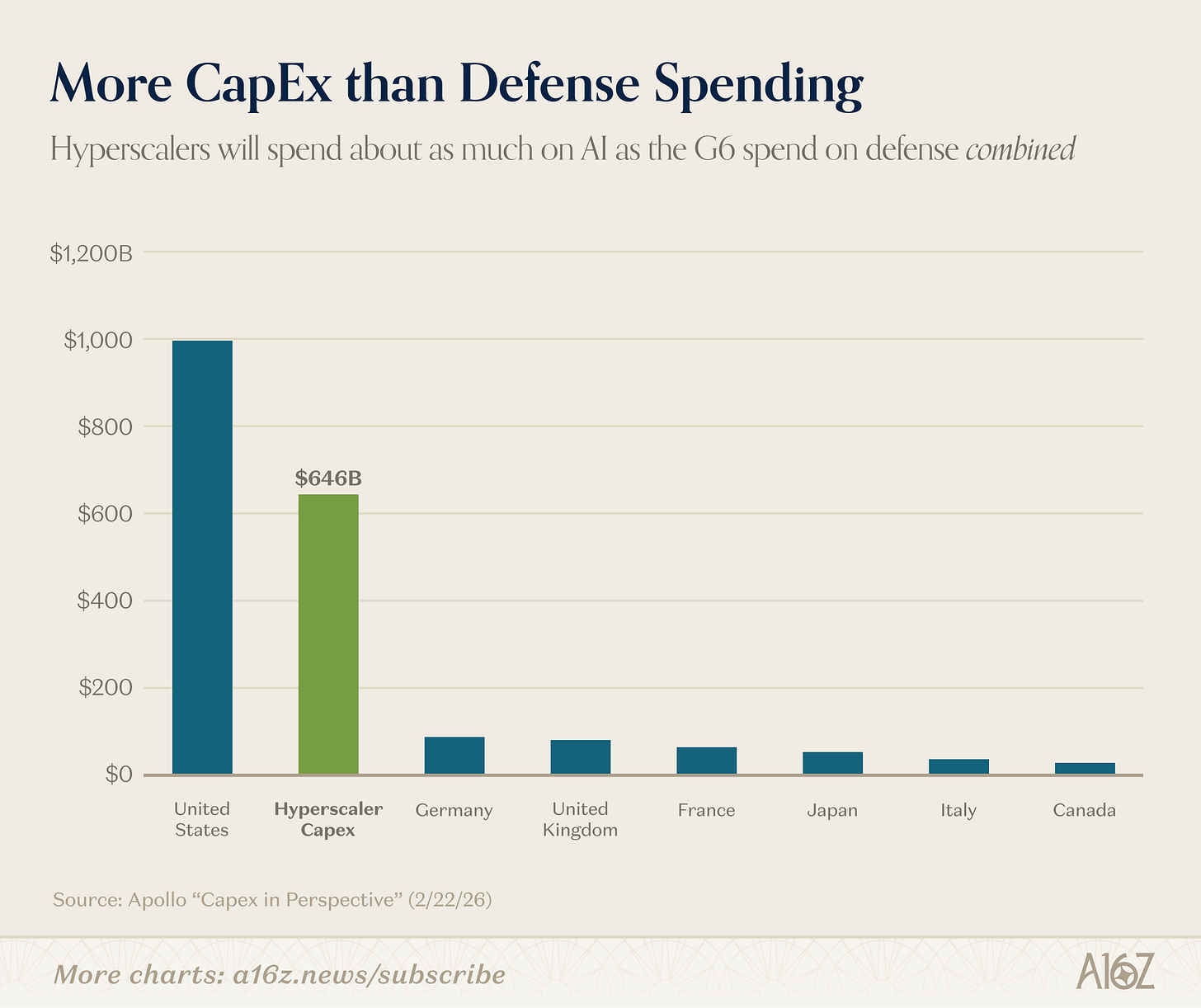

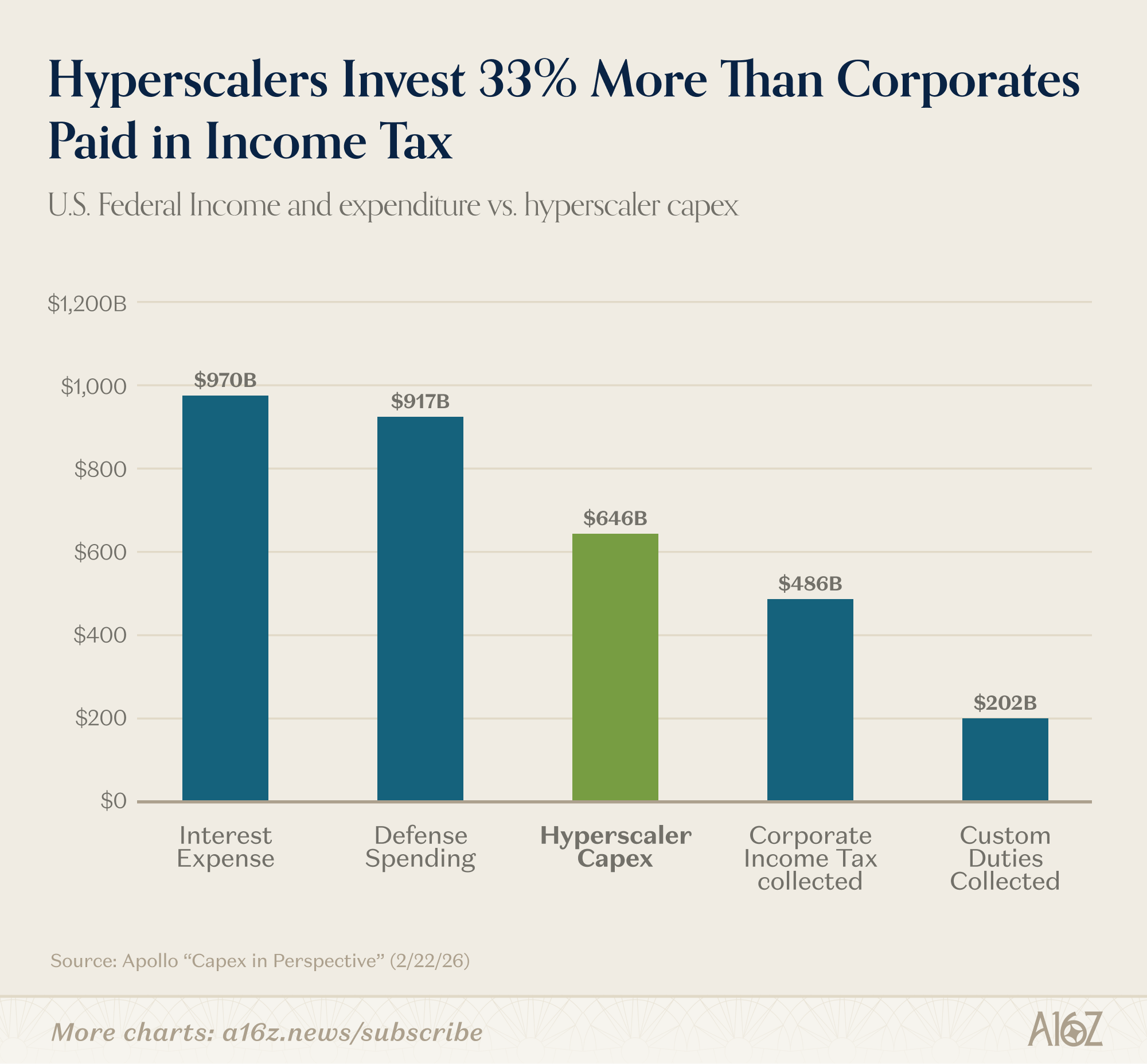

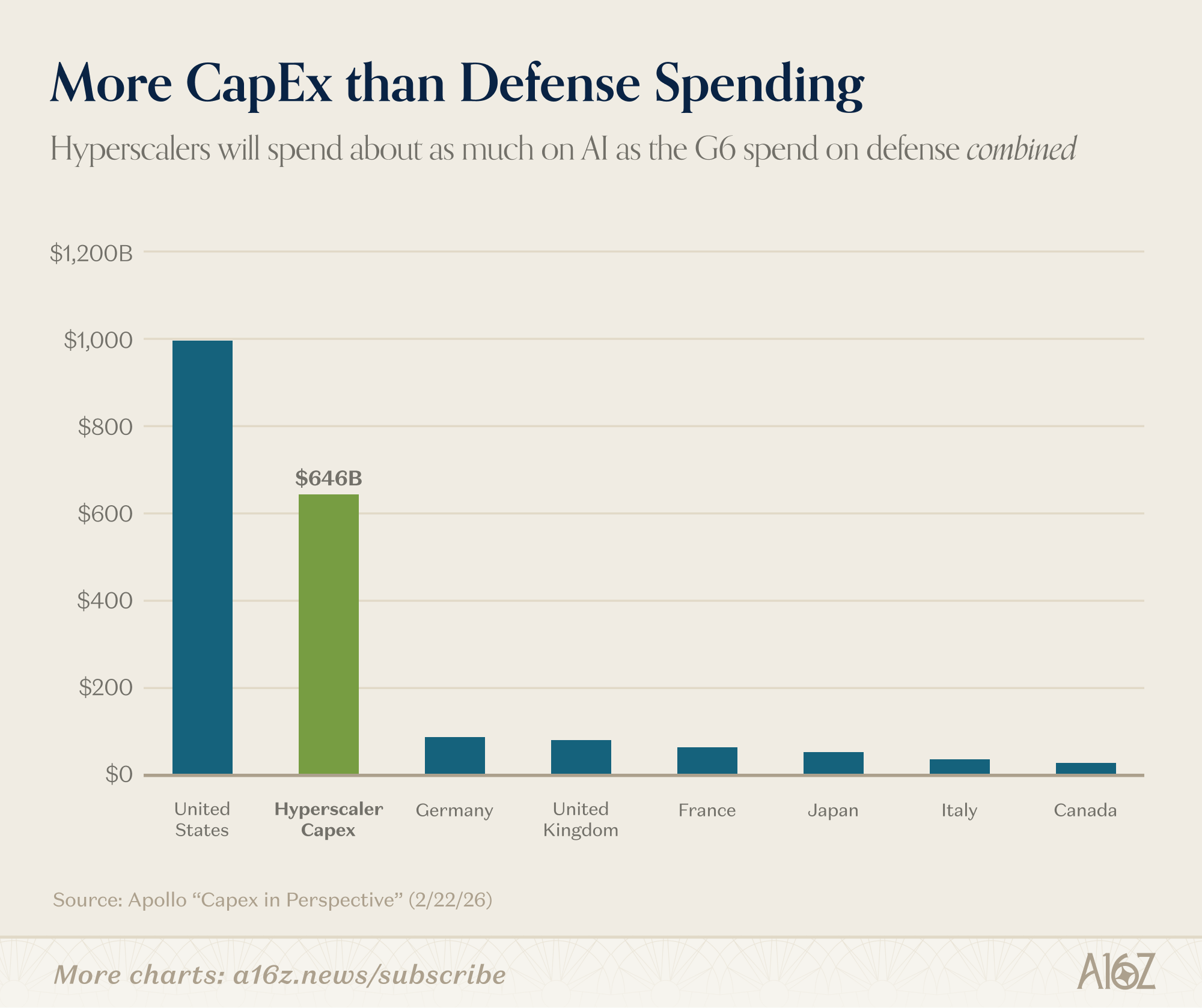

Capex in Context

Behold the data that never seems to get old: AI Capex is big.

How big?

Consider the following:

2026 AI Capex is expected to be nearly as massive as the entirety of net-new bank lending in 2025:

Capex is ~33% larger than the entirety of US corporate income tax collected, and ~3x larger than custom duties:

Capex is ~6x larger than the total military budgets of any of the non-US G7:

So, yeah. It’s a lot of Capex.

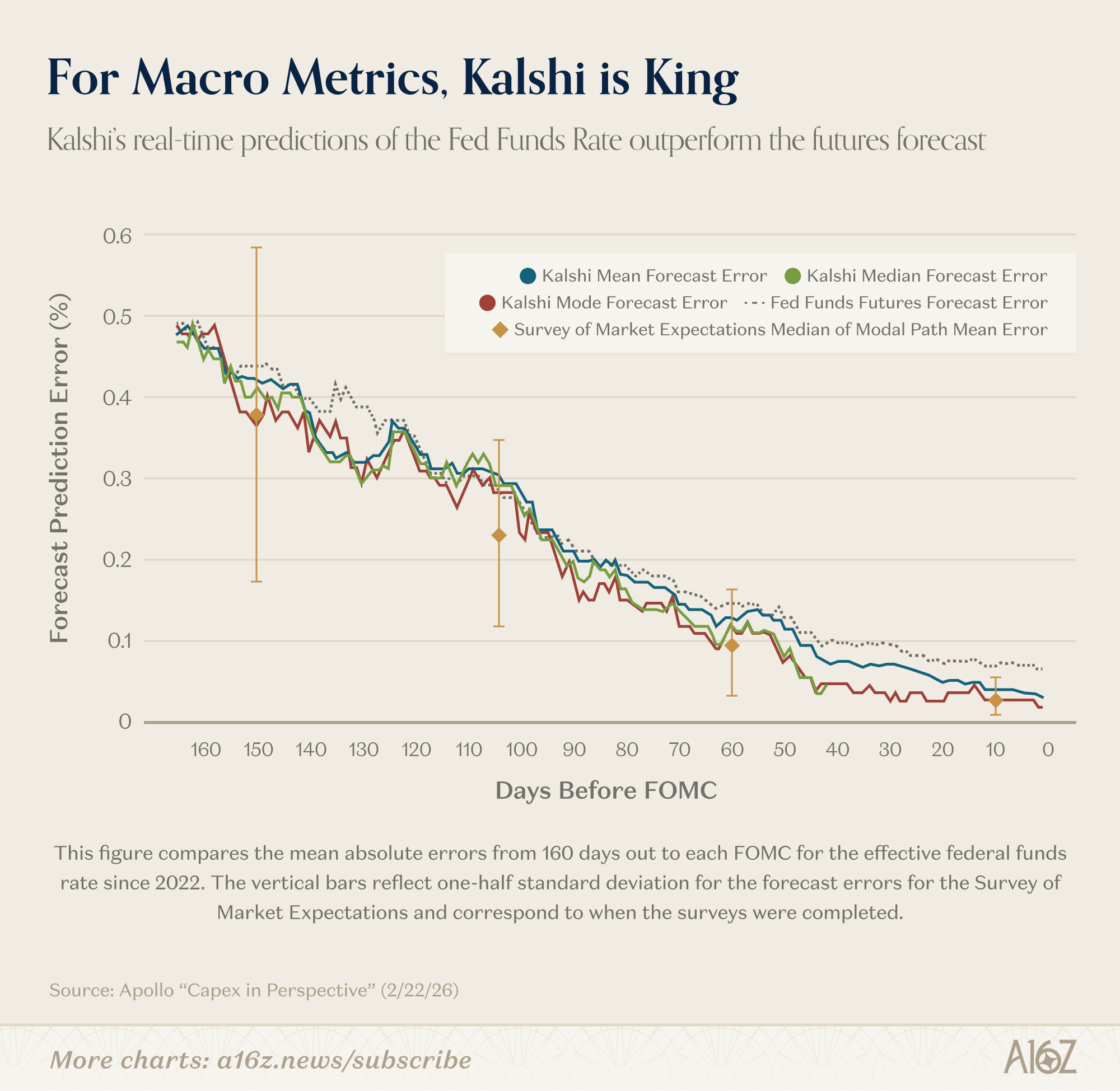

Kalshi Goes Macro

Fed researchers think prediction markets are pretty neat.

By one measure, at least, Kalshi is doing a better job of forecasting the Fed Funds Rate than professional forecasters:

For the federal funds rate forecasts 150 days (3 FOMC meetings) ahead, Kalshi’s mean absolute error is very similar to that of professional forecasters. But unlike the survey—which provides a snapshot every six weeks of a modal path—Kalshi offers a continuously updating full distribution

. . . We find the Kalshi median and mode have a perfect forecast record on the day before the FOMC meeting, which represents a statistically significant improvement over the fed funds futures forecast.

In other words, while all the forecasters start out about the same, Kalshi’s “continuously updating” forecasts get better and better over time, culminating in a “perfect forecast record” on the day before rates are officially declared. Plus, Kalshi did better than the futures forecast.

It’s not just the Fed Funds rate where Kalshi excels. As the Fed researchers point out, because there is no other options market for macro indicators like inflation, growth, and unemployment, Kalshi is the only place for “high-frequency, continuously updated, distributionally rich benchmark[s]” for where the “crowds” think those parts of the economy are going.

Sounds like a pretty big deal.

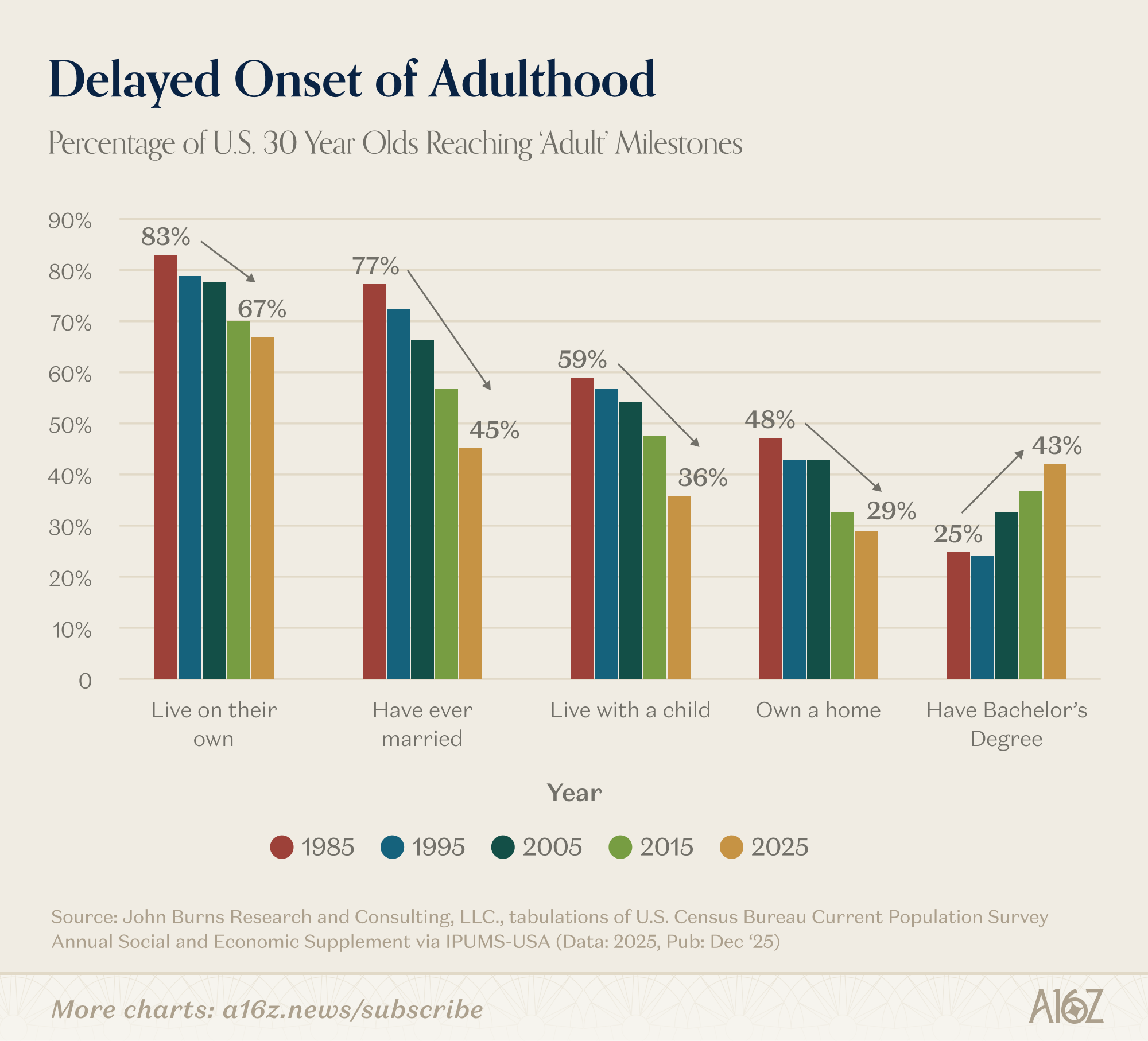

Delayed Onset of Adulthood

This is a striking chart, presented without (much) commentary:

The % of 30yos hitting major life milestones has been in fairly steep decline since at least the 80s.

Fewer 30yos:

Live on their own;

Have ever married;

Live with a child; and/or

Own a home.

The exception to “milestone attainment” is college attendance, where the share of 30yos with a B.A. has nearly doubled since 1995.

Was all that college worth it?

Milestone? More like millstone, amiright?!

Maybe yes, maybe no, but it seems like “buyer’s remorse” is in the air.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe.

Thanks for sharing this! It perfectly captures a shift we’re starting to feel in Europe, too. The 'Delaware by default' trend seems to be fading. This morning, we posted a newsletter regarding the Romanian ecosystem, and we addressed this aspect. https://icebergplus.substack.com/p/2-the-brief

I’m particularly curious about your take on the 'inner sovereignty' aspect. Do you think states like Texas or Nevada are finally figuring out how to keep their own 'slice of the pie' by offering better local protections? It feels like founders are finally choosing sustainable growth at home over the prestige (and the massive headache) of jumping abroad too early. We already see some signals in Europe; here is an article I wrote about this topic. https://icebergplus.substack.com/p/2-the-brief

does the "collegiate class" generate the cadence of civilization, is it generated by it, or are they mutually cocausitive? the true chicken-and-egg question of the westphalian order.

this is the morphism between blue jeans, french semiotic philosophy, and the narrow inheritance lottery.

education of midwits who cannot benefit from it—can anyone? it seems those who can benefit from education educate themselves to unity without $100k (lowball for a provincial school) and, in times of peak gatekeeping like Paris 1250 and SF 2015, some are a credential which selects for trait conscientiousness and agreeableness.

but for civilization, it seems equivalent to the hypochondriac who look up symptoms until going to the hospital, wherein acquiring a nosocomal illness.

those who have beans to knead, may they knead the transient and eternal Meow