Charts of the Week: Making the Stuff that Makes the Stuff

Spirited Away; Giving Zero Clicks; V-Shaped SaaS? Depends on Who’s Asking

America | Tech | Opinion | Culture | Charts

Making the Stuff that Makes the Stuff

There’s a decent amount of evidence that a manufacturing “boom-let” is underway. Survey data shows that manufacturing activity is increasing, for both new orders and production. There’s even some evidence of increased hiring intentions, as well. And American Dynamism has progressed in a few short years from rallying cry to investment thesis to real progress.

For now, though, it’s just a boom-let—you might even call it a modest reversal of a prior malaise. And, while it’s a good start, it’s nothing close to a full “reindustrialization,” or “reshoring,” of American industry. The biggest blocker is that while we’ve gotten more focused on parts and machinery (especially as it pertains to AI), we haven’t spent nearly enough time and investment on the stuff that makes the stuff (i.e. the factories and machines that produce parts and machinery).

We have what’s referred to as a “capital stock” problem:

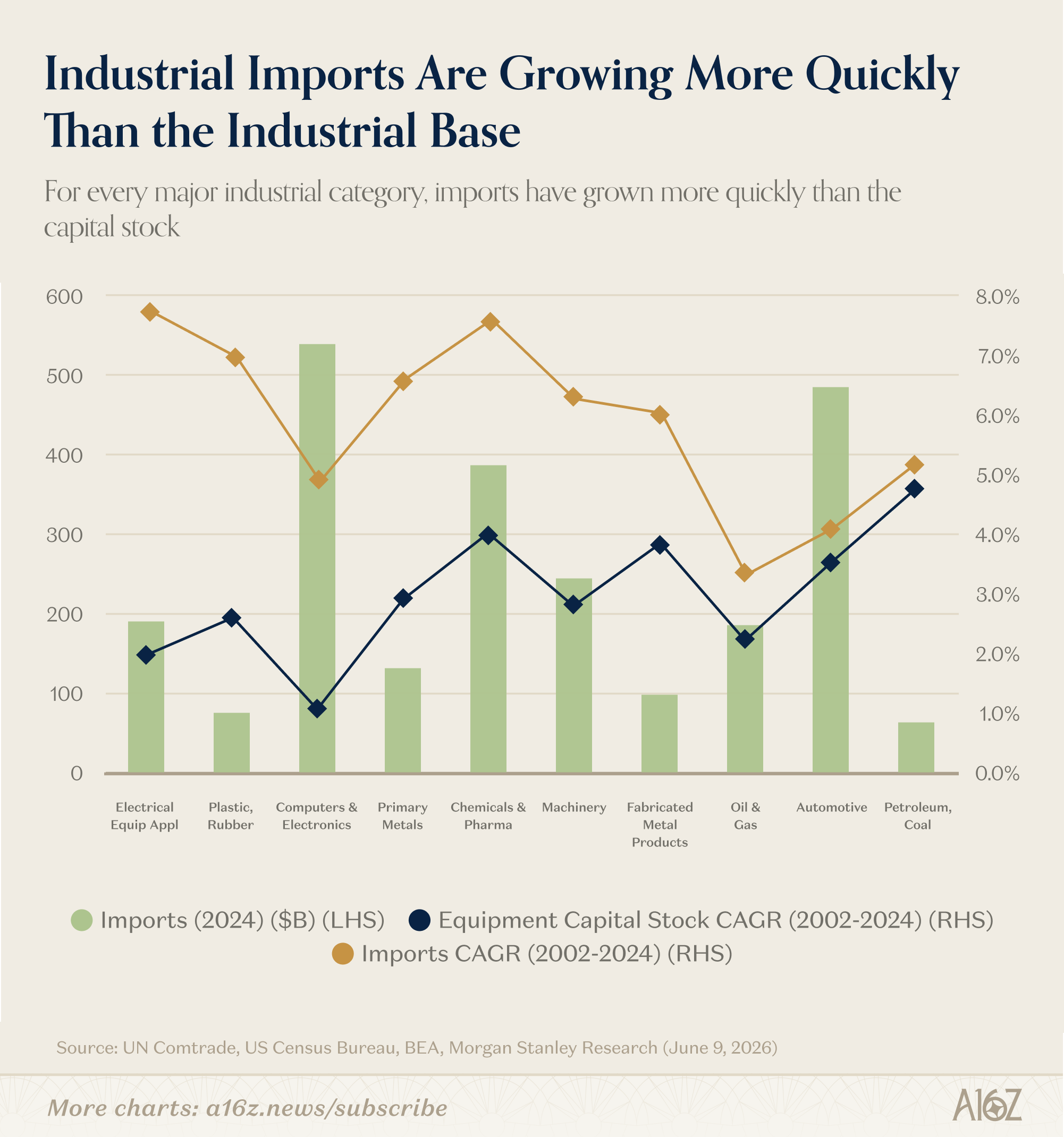

Across all the major industrial categories, imports have grown more quickly than the capital stock of equipment (and structures) to make the things that we’re currently importing.

Certainly, importing more industrial stuff is consistent with more industrial activity. But, to really revitalize American manufacturing, we’re going to need a lot more machine-making machines and factories.

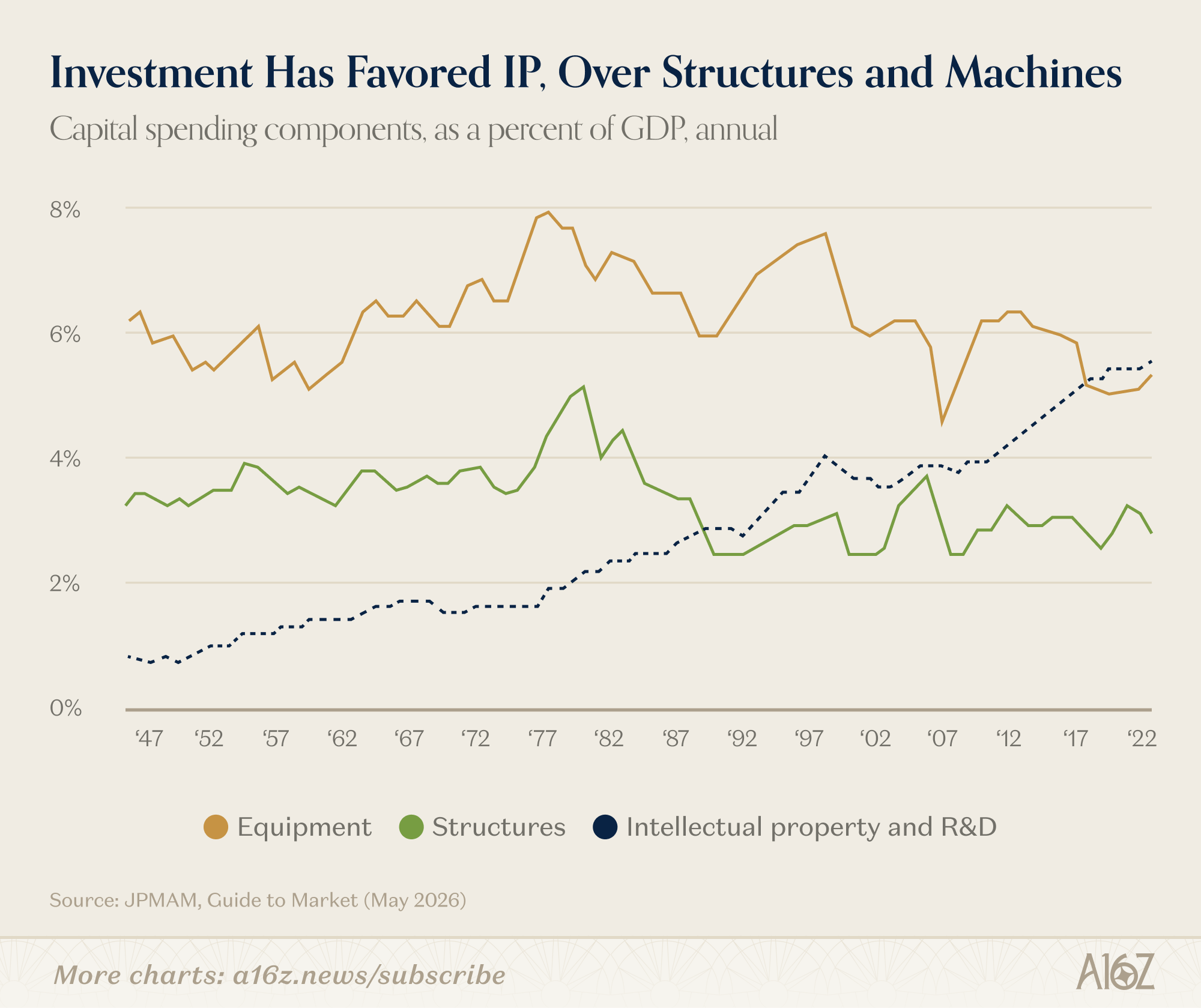

Rebuilding the manufacturing base is not going to be easy, either (and when is it ever?), in large part because we’re very out of practice: relatively modest investment in the capital stock is a long-running trend:

Capital spending on structures and equipment, as a share of GDP, has been more or less in serial decline since the early ‘80s.

It’s a well-known story, at this point, but we very much moved “up the stack,” towards the bits and bytes of intellectual property, and away from the nuts and bolts of atoms.

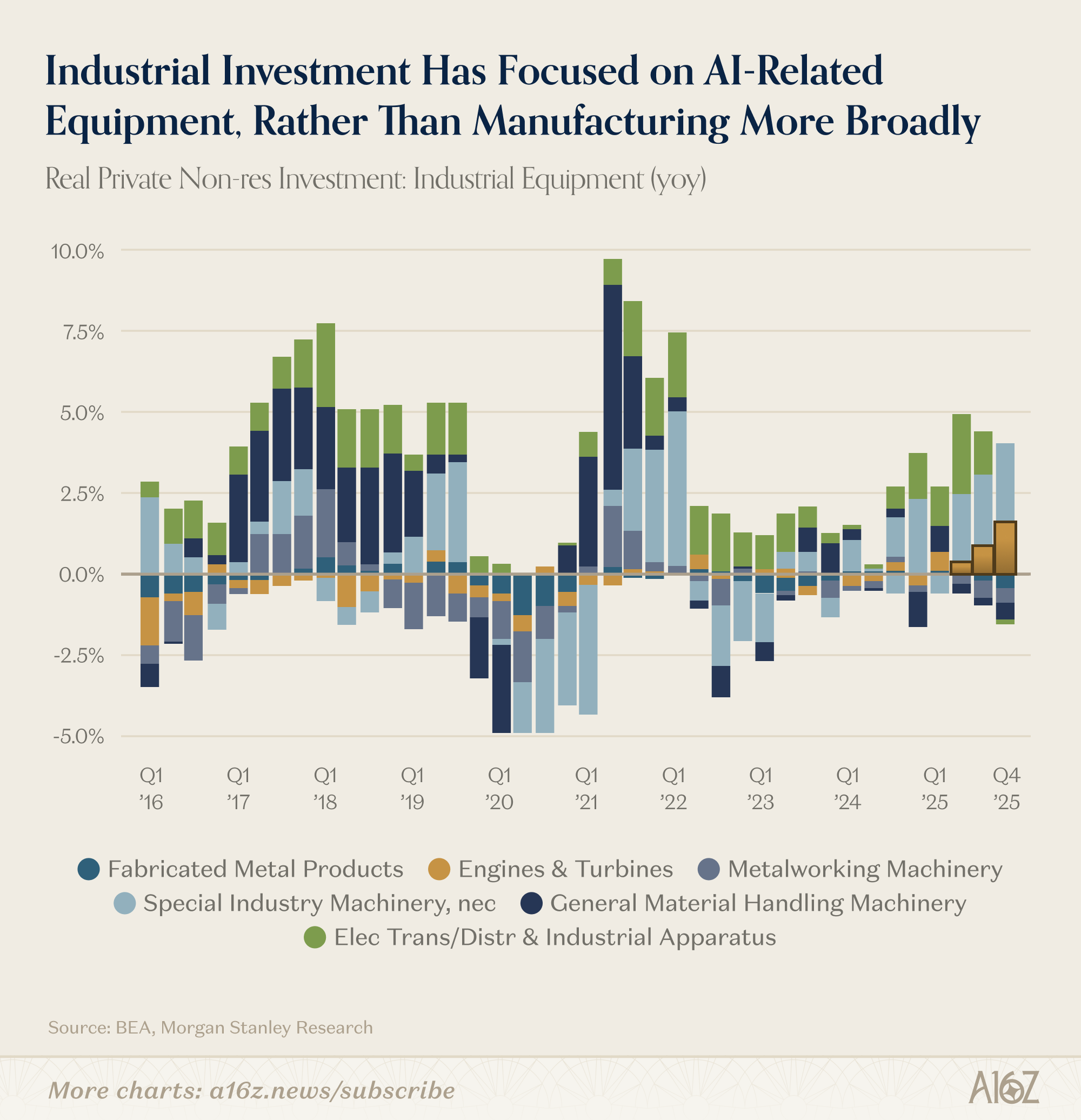

Indeed, even within the category of “equipment” (which has experienced an investment boost in the last few years, with growth approaching 9%), the manufacturing boom-let is fairly narrow, with a singular focus on AI. Investment in core industrial machinery is a smaller part of the picture, and that too, is largely dominated by AI-related needs:

Investment in core industrial equipment (i.e. ex-AI) is about 50% turbines, HVAC, and the like, while the other half is “special industry machinery,” which, in this case, is likely at least part semiconductors, etc.

In other words, where there’s investment in the capital stock, it’s almost entirely focused on the AI build-out, rather than the manufacturing base, more broadly. That’s consistent with the imports story, as well, such that the surge in industrial investment is more aligned with existing supply chains, and less-so with configuring new, domestic ones.

The other thing that’s visible from these longer series is that, as per above, while capital spending on equipment has ticked up of late (as a share of GDP), the opposite is true when it comes to structures—and, once again, it’s hard to make more equipment (and truly “reindustrialize”) without the structures to make it in. For a more enduring transition, we need to increase capacity, and that tends to start with structures.

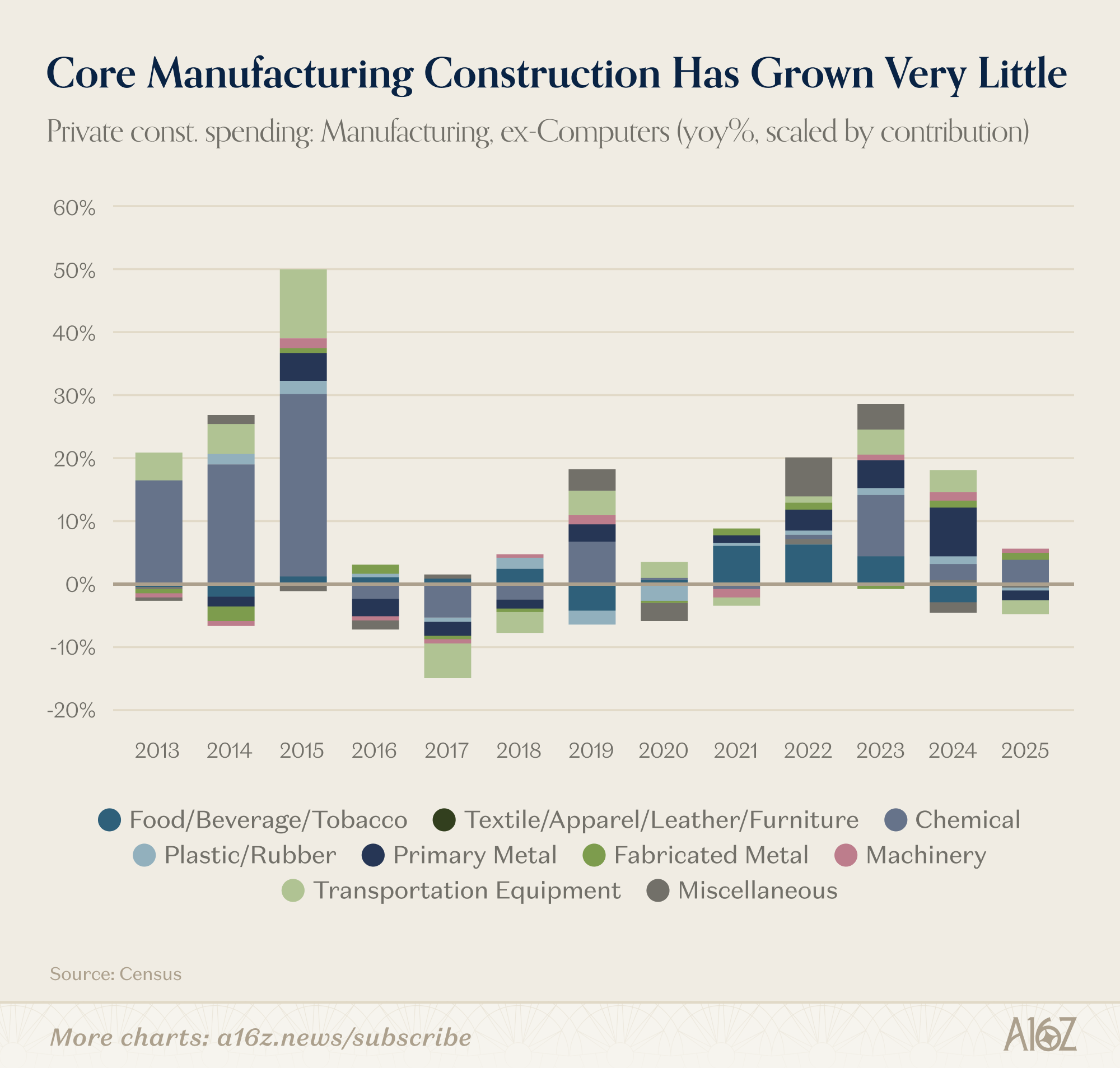

There too, while there have been some modest gains, the gains are, in fact, modest, and focused very much on AI. The CHIPS Act, lower interest rates, and AI likely combined to encourage a surge in semis-related industrial construction, but that has cooled off considerably since its peak in 2023. When it comes to core manufacturing capacity, especially of the sort that would be consistent with a broader non-AI expansion, investment has been a relative drop in the pail:

Outside of semis, manufacturing construction growth increased only ~3% in 2025, and the bulk of it was related to chemicals, consistent with a longer-running trend, as opposed to some recent impulse to domestic capacity.

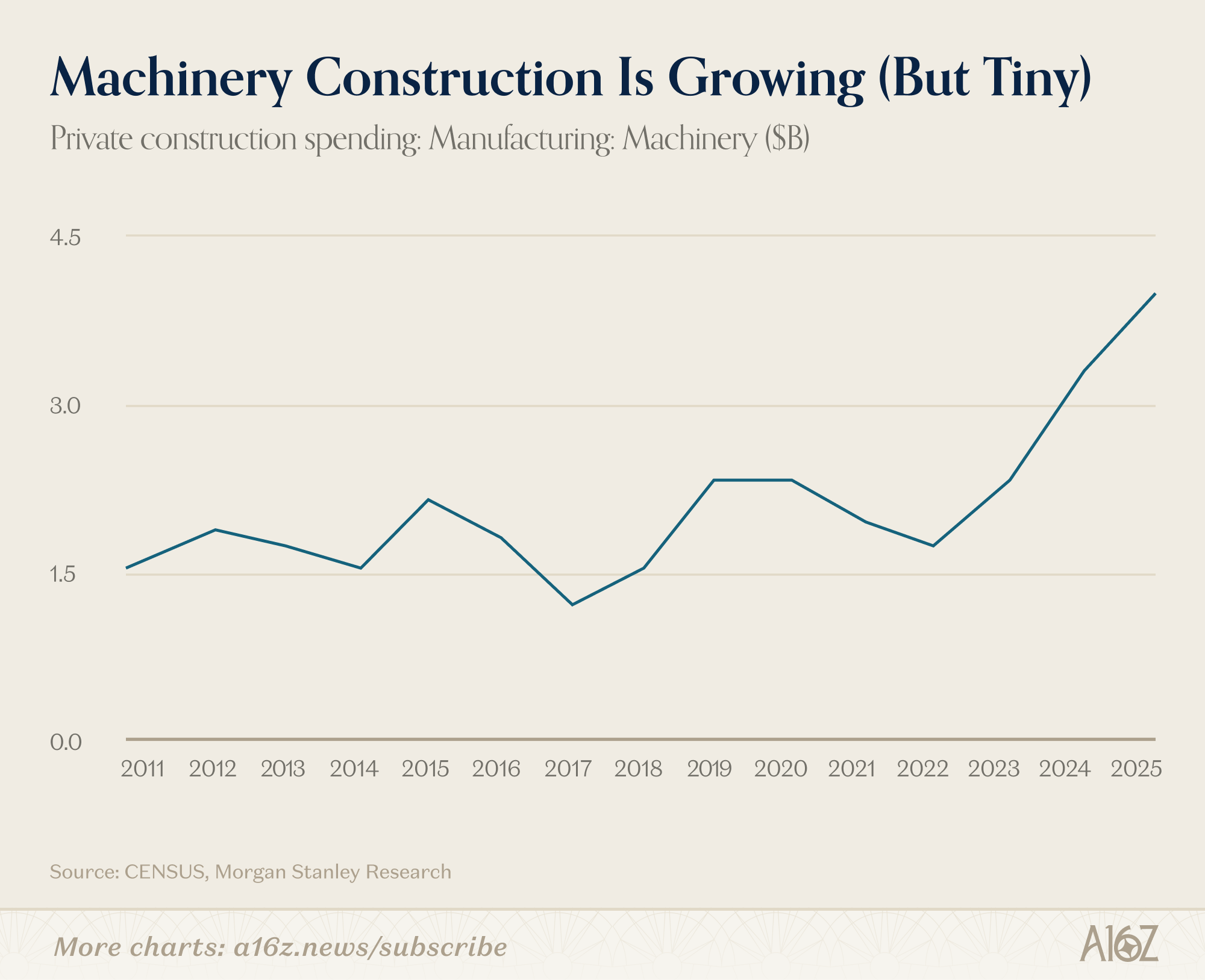

When it comes to machinery specifically, arguably the most important category to a broader industrial revival, construction spending has more than doubled since 2022 . . . from a paltry $1.5B to a slightly less paltry $3.9B.

Obviously, we don’t necessarily need more machine-making buildings to get more machines (or more machines to get more output)—we can also get more productive with the ones we’ve got—but there are limits.

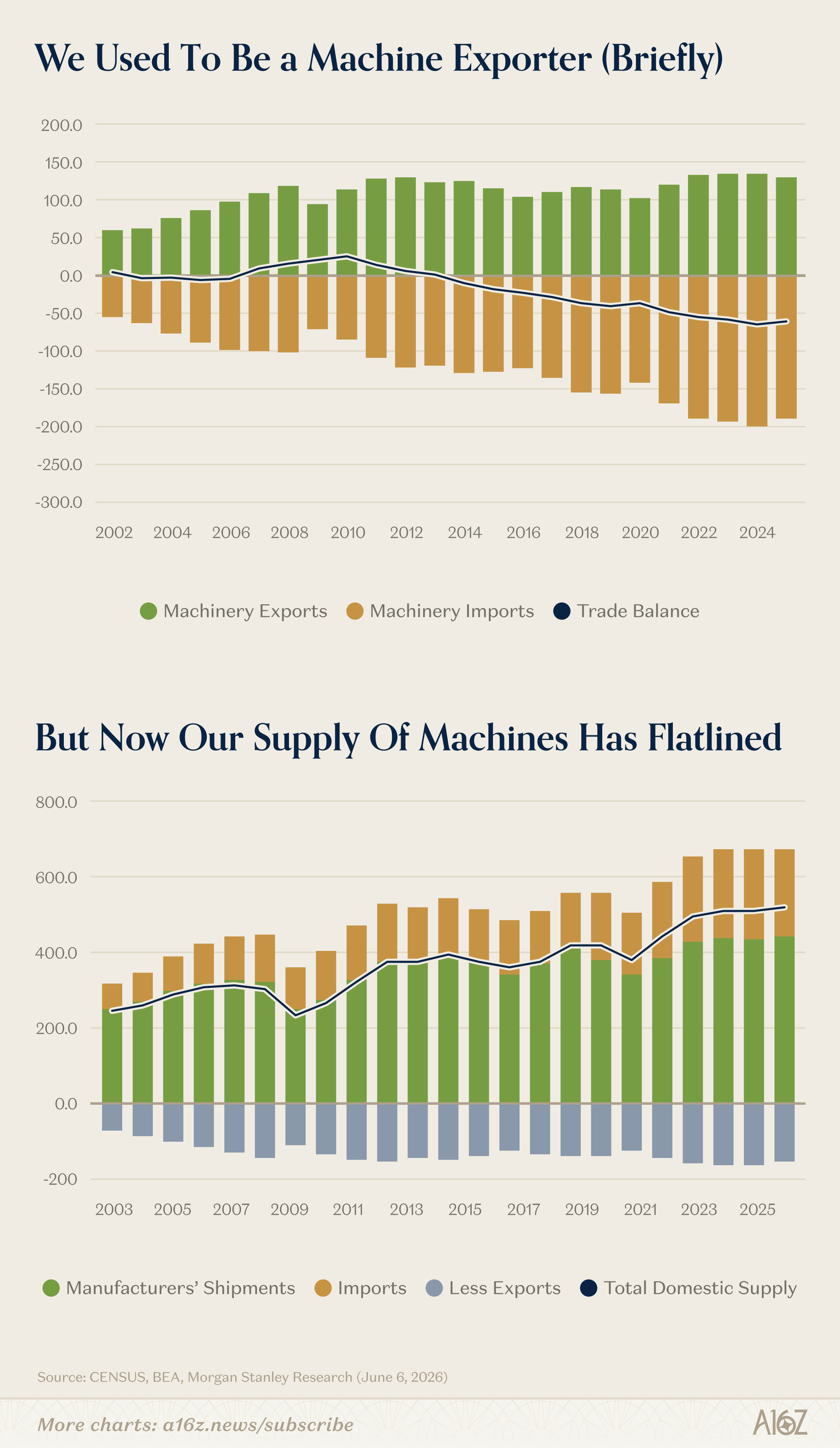

In fact, there was a brief moment in this century when the US was a net exporter of machines, but since ~2013, the situation has reversed:

The domestic supply of machinery has increased over the years, but growth more or less tapered-off back in 2021.

The point here is fairly straightforward: if you think rebuilding the domestic manufacturing base is a good thing, then while there’s been some progress, there’s also a *long* way to go. For better or for worse, we simply have not been investing in the capital stock to support a broader industrial turn. We’re buying parts (especially AI-related parts), but if we’re going to be making more parts, then we need the buildings and machines to make the machines that make the parts, and there isn’t a whole lot of evidence that that transition is underway.

Spirited Away

There’s plenty of anecdata that says “no one drinks anymore,” (especially, young folks). Last year, when the OKC Thunder won the championship, they left buckets of unopened beer and champagne, in a teetotaling display that would shock any athlete (or fan), especially from the ‘80s and ‘90s, when the good times most definitely rolled.

Putting anecdata aside, there’s some actual data, as well, to support the sober turn. There is some nuance, however.

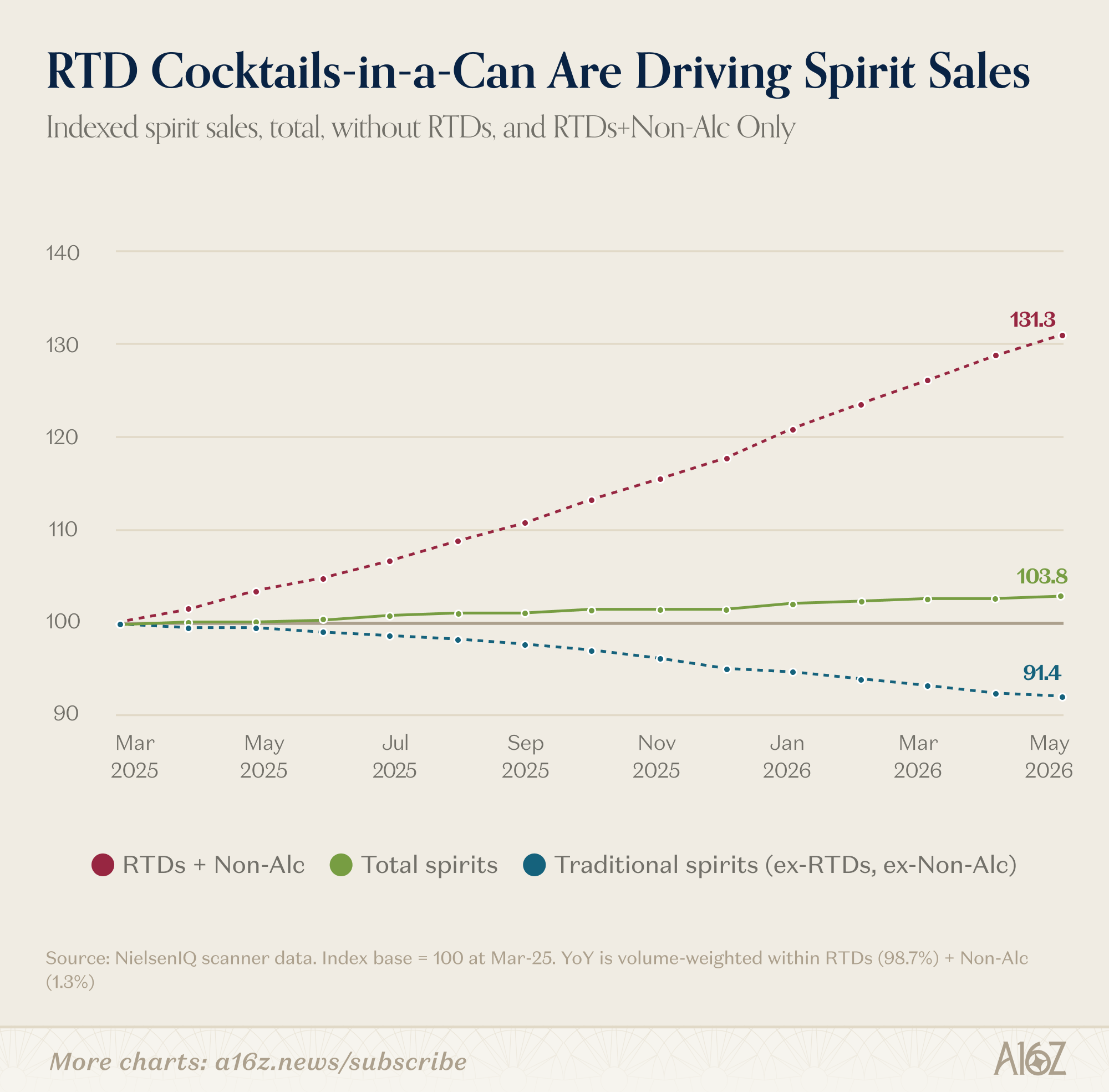

When it comes to spirits, at least, sales (by volume) have been increasing ever-so-slightly:

Spirit volumes are up ~4% yoy, according to Nielsen, but it’s not traditional booze that’s doing the work.

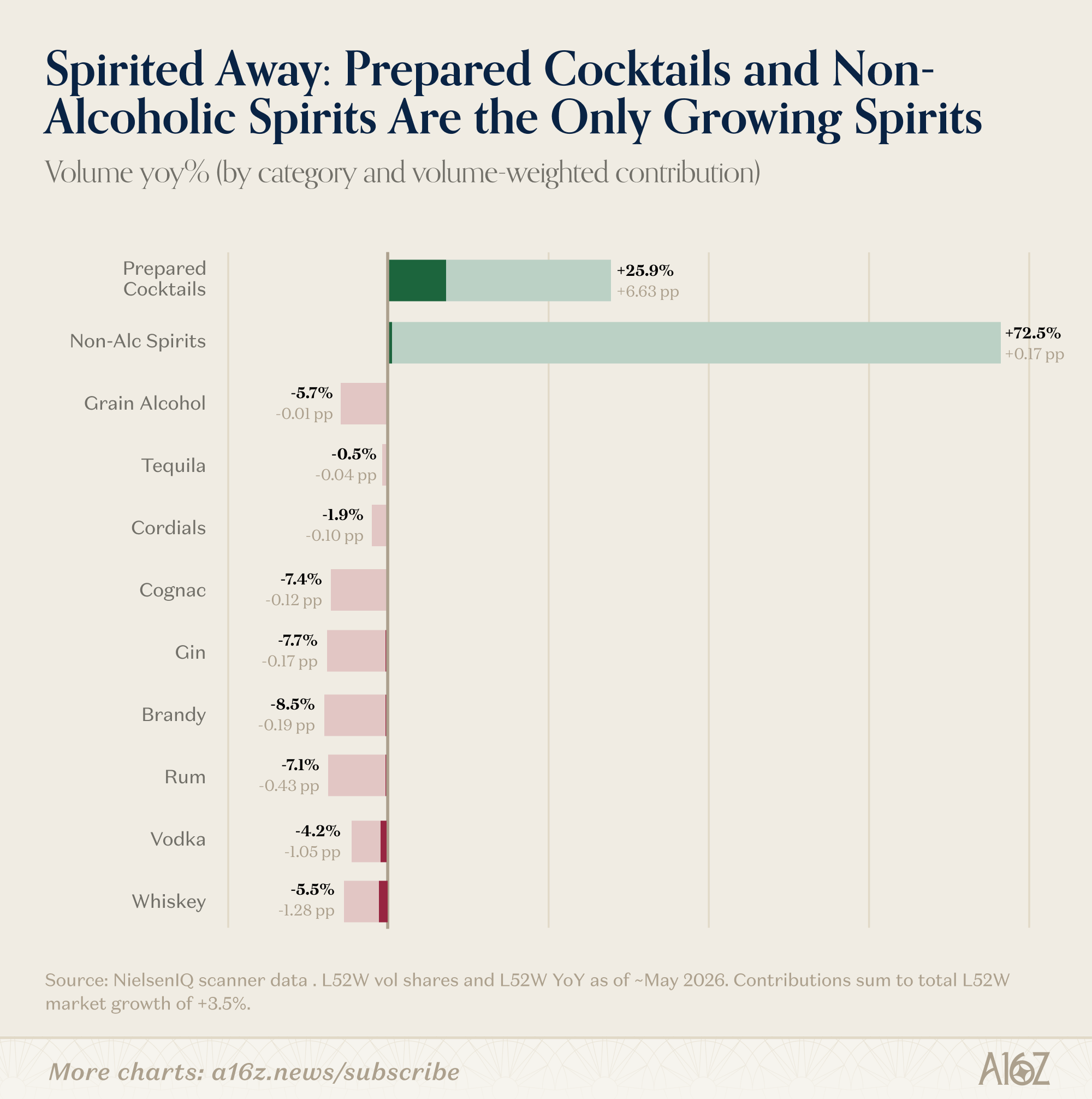

Only two categories of spirits increased: non-alcoholic spirits (which are a relatively tiny category, but jumped over 70%), and prepared cocktails (which are a much bigger % of overall volume, and grew ~26%).

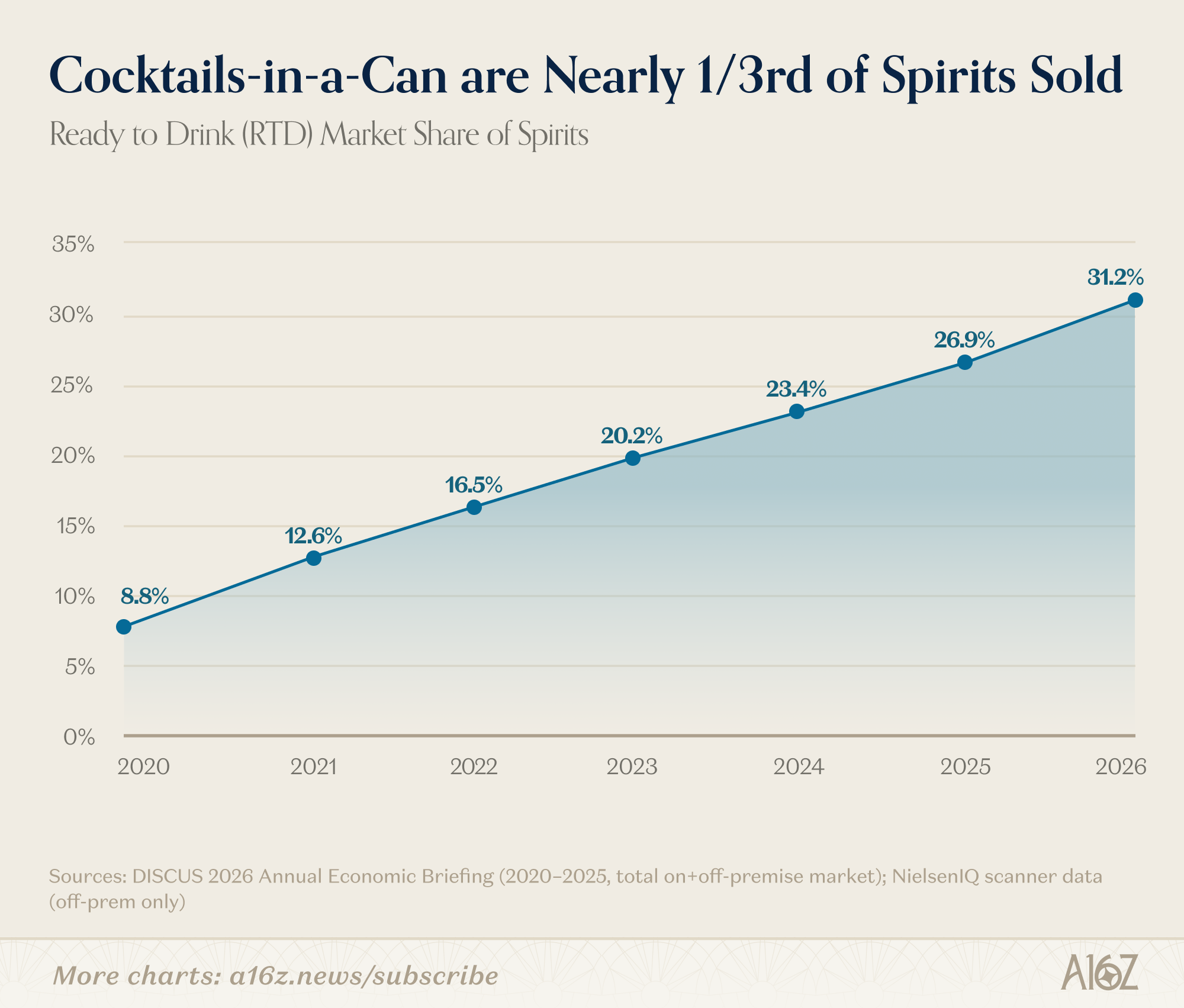

If you exclude prepared cocktails (and non-alcoholic spirits), spirit sales are indeed down almost 10% yoy. All of the gains for the category are attributable to the canned variety, which have become an increasingly big deal.

According to data from the Distilled Spirits Council, a trade group, pre-mixed Ready-to-Drink (“RTD”) cocktails have more than tripled their share of overall spirit sales in just over 5 years.

So, while it’s somewhat true that people are laying off the sauce, it’s a good deal less true when the sauce comes pre-mixed in a can (such that both shaking and stirring are strongly discouraged). Canned cocktails are very much in demand.

Who said there’s no innovation in food and bev?

Giving Zero Clicks

There’s a big change underway in how we surf the internet, at least according to some research from SparkToro.

In the old days, the typical motion for browsing was pretty straightforward: search then click. User puts a query into Google, Google surfaces some helpful links (some paid, some not) and the user clicks through to whatever looks most promising. Google was the gateway to the “open web.” Of course, an entire industry evolved around being one of the lucky links to be surfaced by Google for any given search—if your page could make it to the top, there’s a better chance the user would choose you, and as a publisher, capturing those eyeballs was basically the business.

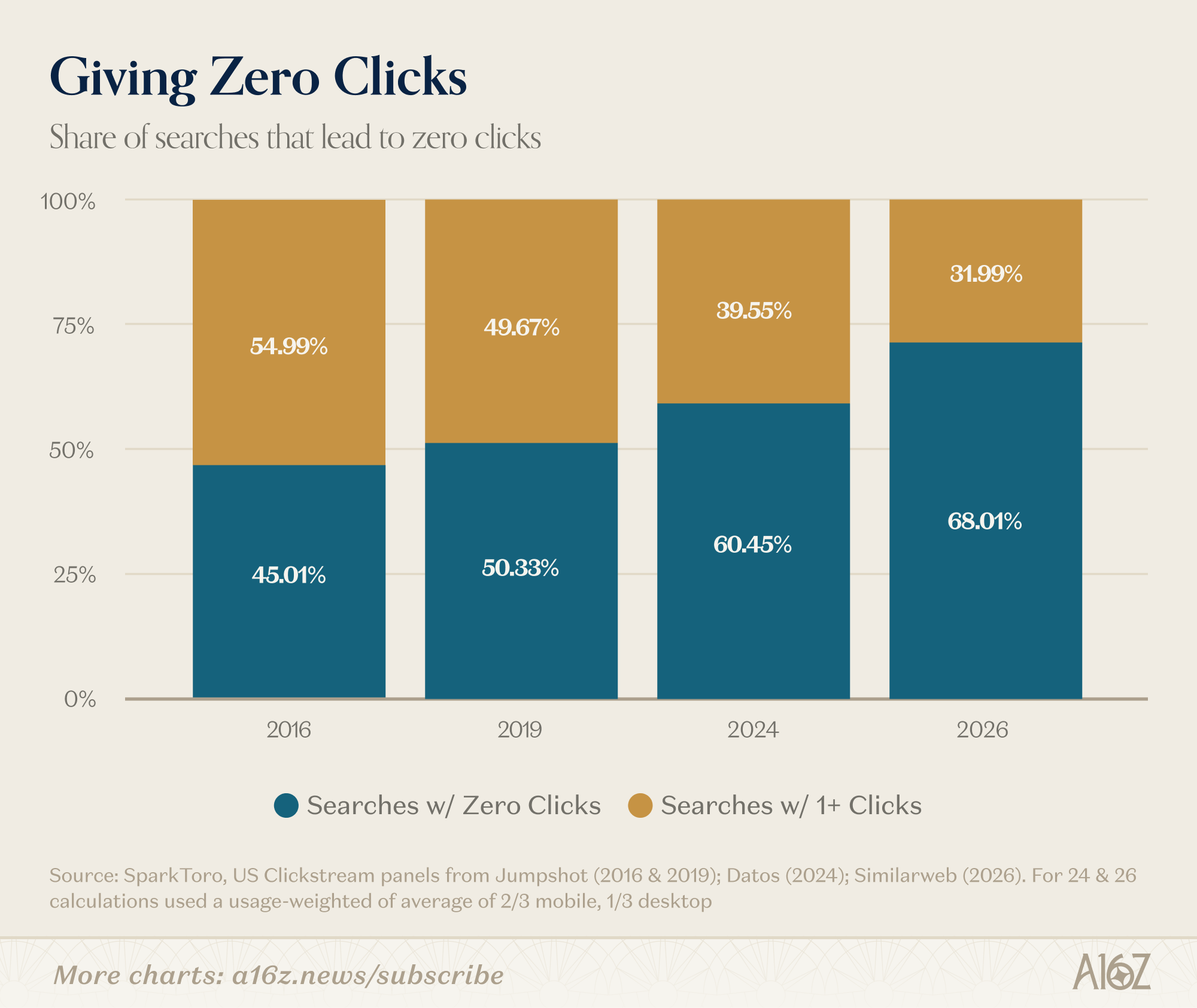

Nowadays, however, the game has changed. Instead of “search-then-click,” it’s increasingly the case that users are “searching-then-stopping,” or perhaps, “searching-then-searching-again,” but in all events, the “click” part is becoming a relative scarcity.

Zero-click searches are now just under 70% of queries, up from 45% just a decade ago, according to Similarweb’s data (combined with some previous panels):

What’s perhaps more striking is that the rise of zero-click searches appears to have accelerated recently. It took about 2 years to move ~10pp, while it took 5 years to make the same move before.

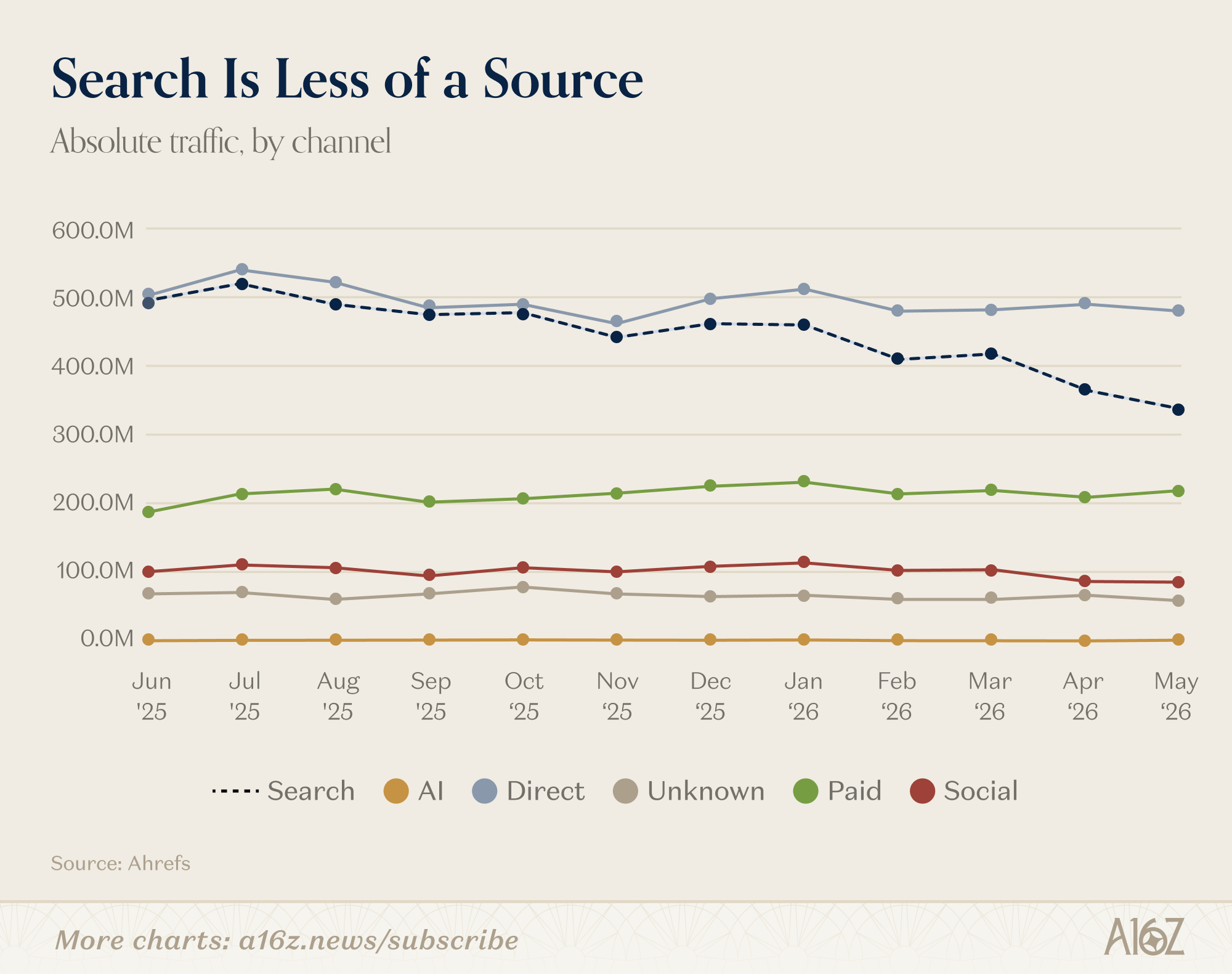

The shift shows up in other data, as well.

Search as a traffic source (for the pages tracked by Ahrefs) has been declining for a while, but really dropped off even more so this year. Direct traffic has also declined, while paid traffic has moderately increased.

The likely driver for the rapid acceleration of zero-clicking is, of course, AI summaries, which either obviate the need for the user to click-through, and/or prompt the user to simply make another search to get a better or different summary—there’s some evidence that AI summaries reduced CTRs by nearly 60%.

The implication for publishers is that being visible to Google search (in the traditional sense) is becoming somewhat less valuable (and harder to monetize). For Google, presumably it means more searching (and otherwise staying within Google’s universe, rather than migrating to a publisher’s site), which is probably good for Google.

V-Shaped SaaS? Depends on Who’s Asking

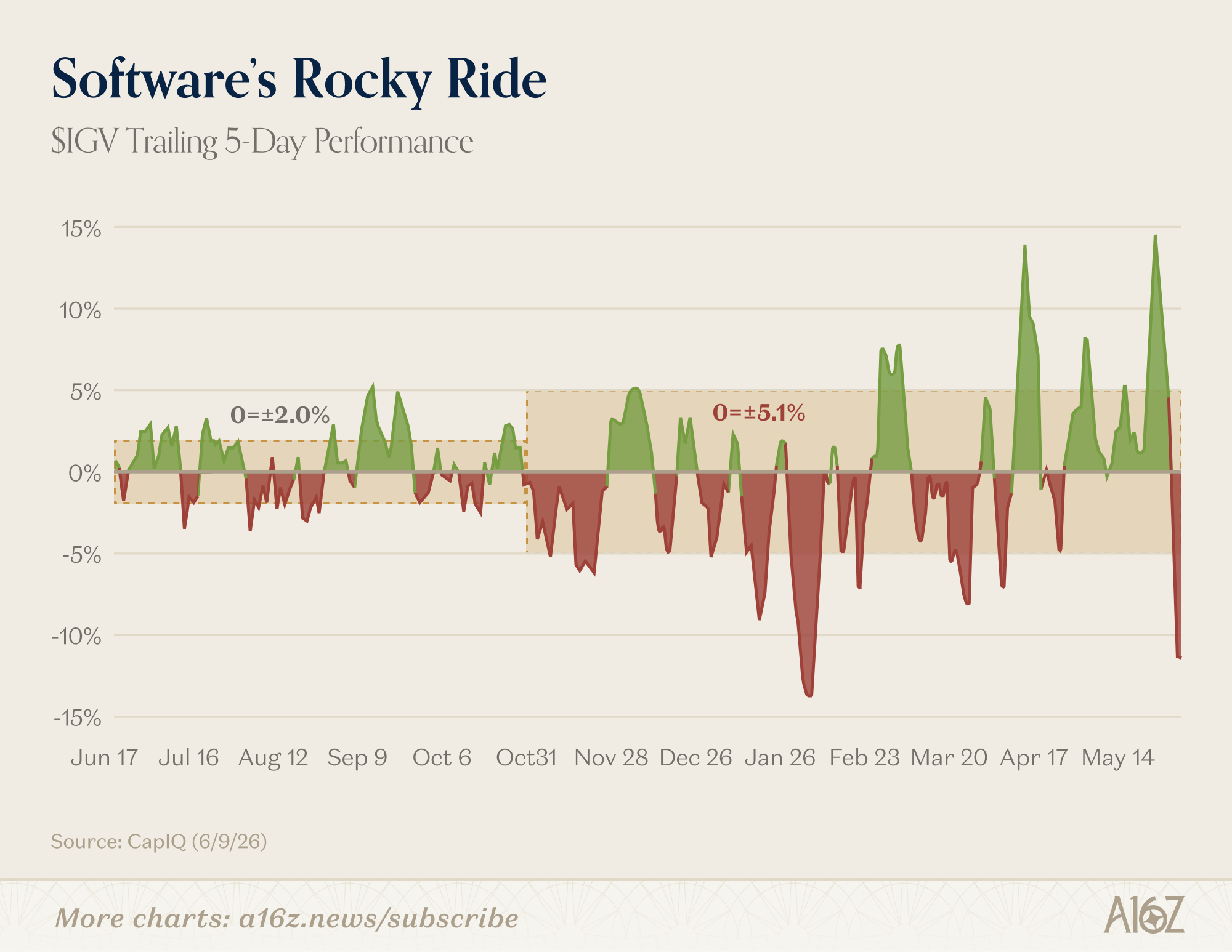

In the bigger scheme of things, the rollercoaster for publicly traded software businesses continues apace, if not even more rollercoastery than before:

IGV (the software ETF) took its pounding through February, had a brief reprieve, then more pounding, and then a pretty good month-long stretch when SaaS was almost so-back . . . only to be followed by another big sell-off.

At some level, the underlying picture here is one of more volatility—the outer limit of a standard deviation move has more than doubled since October, when the boat first started rocking in earnest.

Beneath the surface though, there is at least some semblance of discernment—yes, the moves are more violent, but the market is not treating software businesses indiscriminately. There are plenty of V-shapes, but the Vs are not remotely the same. If you look at the software businesses that have had at least some bust (-5%+) followed by at least some recovery (+25% of the drawdown from the period high)—what we’re calling a V—a very clear distinction emerges.

Compare the following sets of V-shaped recoveries for constituents of the major software ETF, the IGV 0.00%↑ .1

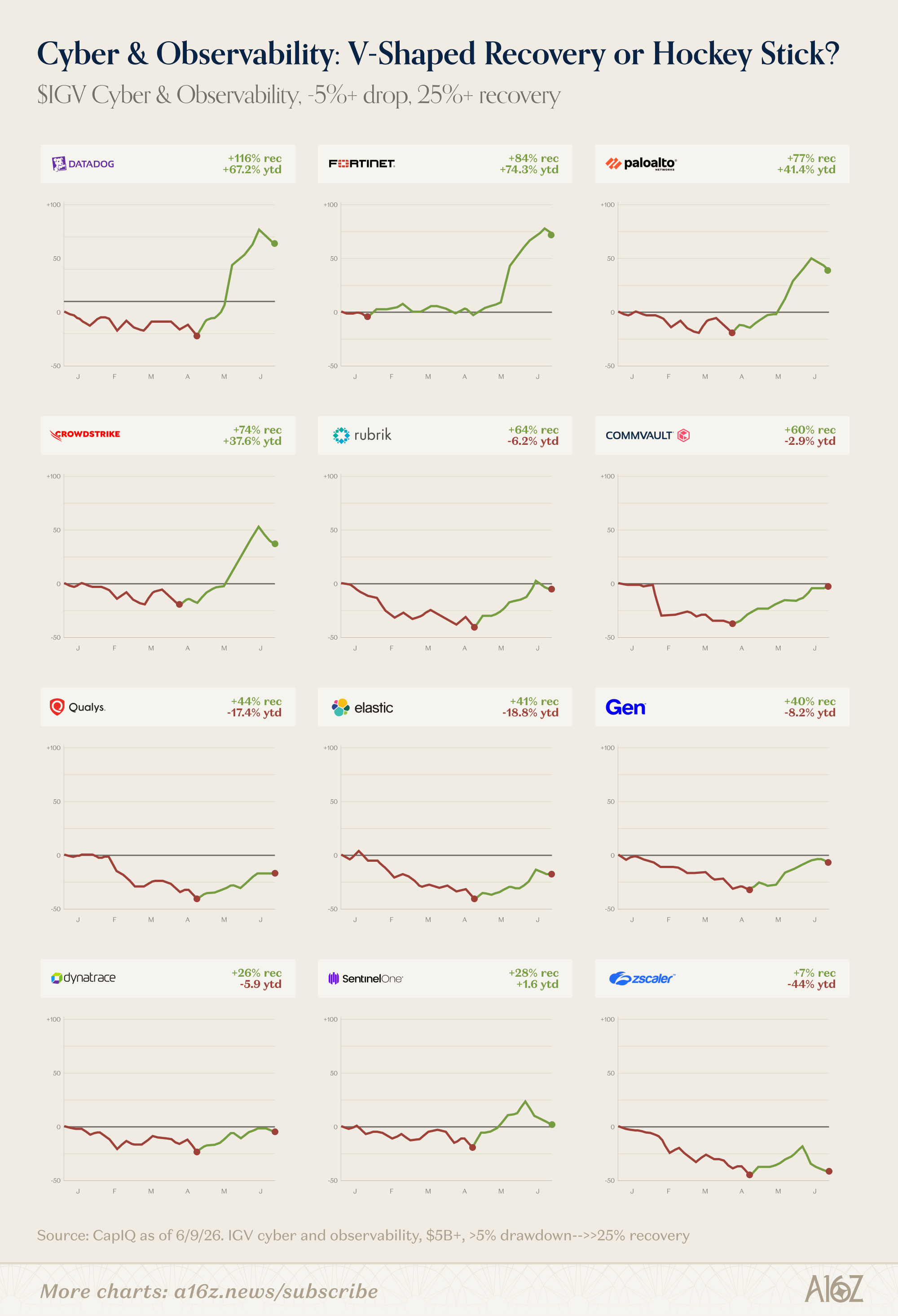

First, we have cyber and observability:

For at least four of these companies, the “V” looks much more like a hockey stick—the drawdown was brief and trivial, while performance since then has been very strong. Outside of Zscaler (who had a V, then lost it, but also reported yesterday, after this chart was made), every “cyber and observability” V has either fully recovered, or is close.

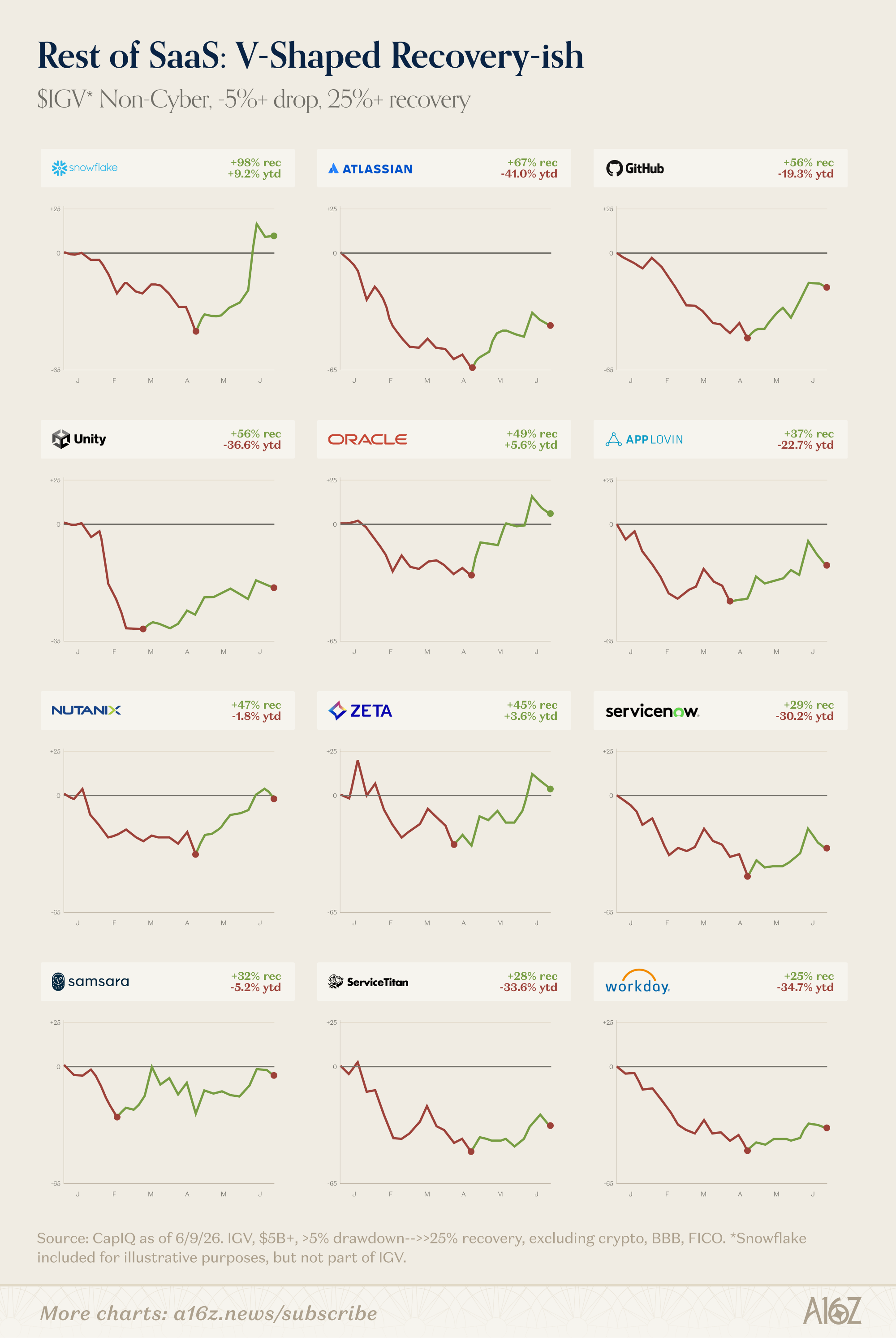

Now consider the non-cyber and observability software businesses:

Here the “V” is much more pronounced. Outside of Snowflake, which recovered all of its losses and then some, these SaaSCos were punished pretty hard. And while they’ve recovered some ground, they still have a ways to go if they ever plan to complete the V (and, again, the picture has worsened slightly, since the data for these charts was collected).

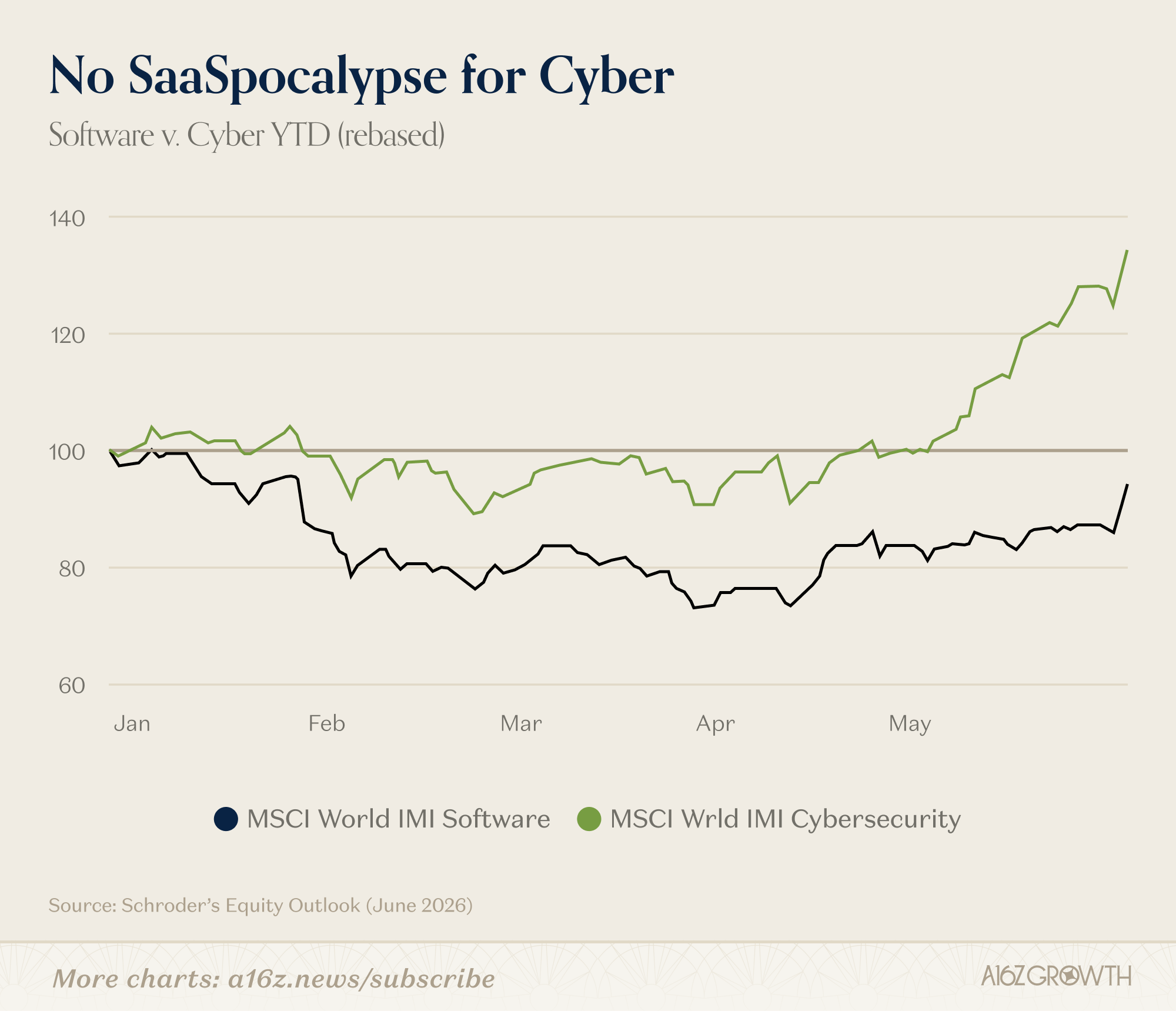

In other words, if some time in January, the market decided that AI has doomed software, it very quickly decided that (a) cyber was the exception; and (b) at least some SaaSCos, perhaps, weren’t as bad as feared.

For cyber especially, the story has gone from “actually not so bad,” to “pretty great, thanks for asking.”

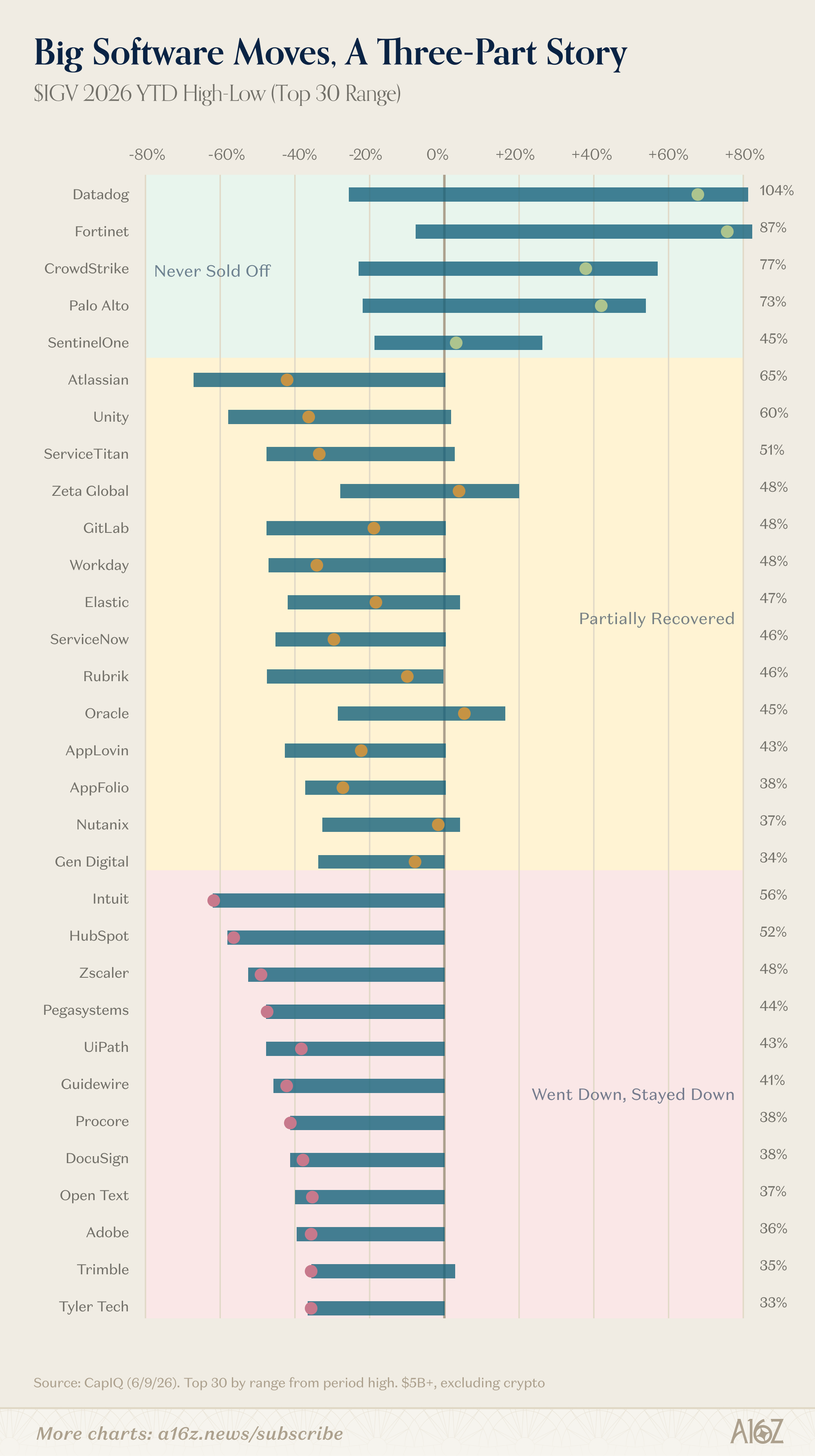

The point here is that the headline figure of the IGV (albeit dizzying) is obscuring a much more nuanced picture beneath the surface. Here again, is a cut of the top 30 names by price-swings (bottom-to-top, from the period start):

Three buckets emerge:

Some that never really sold off in the first place (cyber and observability)

Some that sold off pretty hard, but have made partial-to-full recoveries (and Oracle and Zeta would look slightly worse, with the latest data)

Some that went down, and have more or less stayed down (at least, thus far).

In other words, when it comes to software, the market appears to be saying that yes the AI threat is real, but not for everyone, and even where the AI threat is real, if the fundamental story is strong (and/or AI is a positive driver), we’ll be cautiously optimistic.

For cyber and observability, the zeitgeist says that vibecoding a CrowdStrike, etc. just isn’t happening. Buyers are too risk-averse, the cost of failure is too high, and if anything, AI has introduced a new threat-vector that only increases buyer urgency. Whether that’s right or wrong, time will tell, but that’s certainly what the market is signaling. Whatever the AI-discount to terminal value that’s been applied to SaaS generally, cyber is getting special treatment.

For everything else, if you can tell a story where AI is increasing demand and it shows up in the results, e.g. Snowflake, the market has, in some cases, welcomed you back with loving arms. Even a slightly less compelling version of that story (e.g. Atlassian, AppLovin, GitLab and Zeta) can still go a long way. If, on the other hand, you can’t tell that story, but really more importantly, you can’t show that story, it’s simply not enough to say “we’re still doing just as well as before, and maybe even slightly better.” In that case, the market appears to have fundamentally repriced your equity, and the SaaSpocalypse is very much still on.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

Snowflake is not in the IGV, but we included it for demonstration purposes. We also excluded crypto-related companies, companies at or below $5B in marketcap, and BlackBerry and FICO (which aren’t really SaaS businesses, in the traditional sense, although Blackberry might be close).

The no-click search is likely to become a big issue. We're getting the AI summary for free now, I can just see the links on the side of the AI summary, to stuff that humans actually wrote with the hope that searchers will click. And just feel a bit of free-rider guilt.

Not sustainable. If there's no way to prevent raiding content and not pay anything to creators, human creators will cease to exist as a specie. Humans will stop letting their writing being used for free by AI companies, or stop writing altogether.

And AI companies, of course, will have to stop providing those summaries for free.

So, enjoying these while it lasts, while wondering what comes next. A business model for AI that doesn't involve short-changing the original human creators - that's the next step, but not sure it will come from Silicon Valley. There's a coordination pb that the oligarchy may not solve.

The capital stock framing is right, but the mechanism goes one layer deeper. We didn't just move production offshore — we moved the process knowledge that ran it. Capital can fund new structures and machines. It can't compress the institutional memory that accumulates in tooling, process engineers, and supplier relationships over decades. TSMC Arizona is the proof: unlimited capital, world-class engineering, still three-plus years to high-volume production. That ceiling is the constraint the investment charts can't show.

https://levelset.substack.com/p/waymo-tesla-robotaxi-manufacturing-architecture