The Power Brokers

a16z and the Rise of the Future: a guest special by Packy McCormick

| America | Tech | Opinion | Culture | Charts |

To mark the occasion of our $15B fundraise, our good friend Packy McCormick of Not Boring wrote a long and wonderful piece about us. You’re gonna love it. -AD

This article reflects the views and opinions of the author and does not necessarily reflect the views or beliefs of a16z. Investment returns are included throughout this article. Past performance is not indicative of future results. See related fund returns and disclosures at the end of this piece.

Hi friends 👋 ,

Happy Friday! IT’S TIME TO WRITE about a16z.

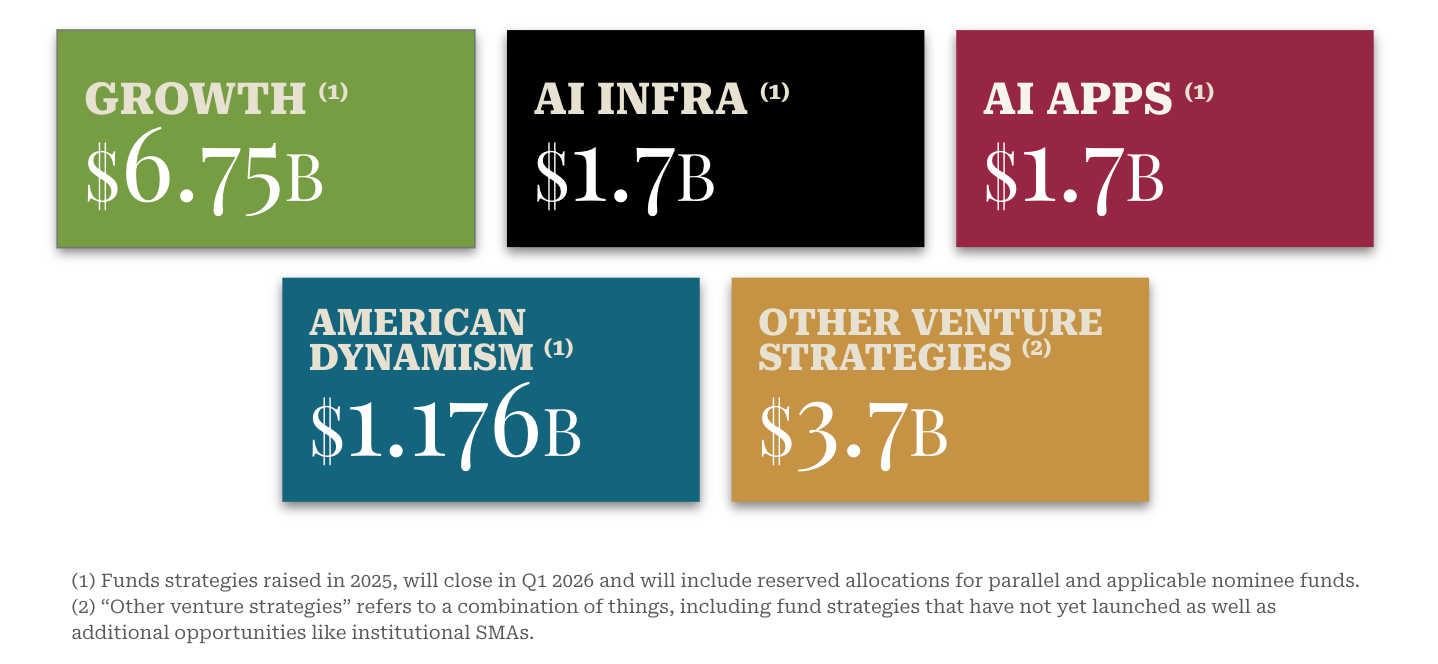

Today, a16z is announcing $15 billion in fresh funds.

To commemorate the occasion, I’m writing a Deep Dive on the Firm. I spoke with Firm’s GPs, LPs, ~$200 billion worth of portfolio founders, reviewed documents and presentations, and analyzed returns data for a16z’s funds since inception (see appendix with disclosure information at the end).

There is a lot of writing on the internet about what’s wrong with a16z’s approach. You probably know the arguments. They’ve followed the firm since inception.

I think it is much more interesting to understand just what it is that all of these smart people who have been right in the past think it is that they’re doing now.

And look, I am about as far from an unbiased observer as anyone without an @a16z.com email address could be.

For more than two years, I was an advisor to a16z crypto (but am currently not compensated by the firm). Marc Andreessen and Chris Dixon are LPs in not boring capital. From time to time, I am on the same cap table as a16z. I am friends with a lot of people in the Firm and with most of the New Media team. I partner with, like, and respect these people.

But look, we’re not counting on me to analyze whether a16z’s pitch at this moment in time is worth investing in. Sophisticated institutional LPs have decided, to the tune of $15 billion, to do so. It will take a decade to know whether they made the right decision, and nothing either I or any hypothetical critic could say will change that outcome, just as it hasn’t in the past.

What I can hopefully bring is a way to think about what a16z actually is from my unique experience. I think a16z is the best-marketed Firm in venture. It can, and does, tell a story about itself. Based on my experience, I can tell you that its story is consistent with its actions. The things that a16z says about itself to the public are the same things it trains its team on internally. The pitch it makes is the same one it’s made since its first Offering Memorandum. And you will be able to judge the returns for yourself.

There are a lot of great venture capital funds and investors, some of the best of whom have been profiled recently. Their approaches and successes are increasingly well-appreciated and well-understood.

But a16z is doing something different, bigger, less… understated. It doesn’t feel like venture capital is supposed to, in part, I think, because I don’t think a16z cares if it’s doing “venture capital.” It just wants to BUILD the future and eat the world.

Let’s get to it.

a16z: The Power Brokers

“I’m living in the future so the present is my past,

My presence is a present kiss my ass.” – Kanye West, Monster

Andreessen Horowitz hears your feedback.

That it’s too loud. That it should shut up and dribble, politically speaking. That you don’t agree with a recent investment or two. That it is unbecoming to Quote Xeet the Pope. That there is no way it will ever generate a reasonable return for LPs on such enormous funds.

a16z does hear you. It has been hearing you, at this point, for nearly two decades.

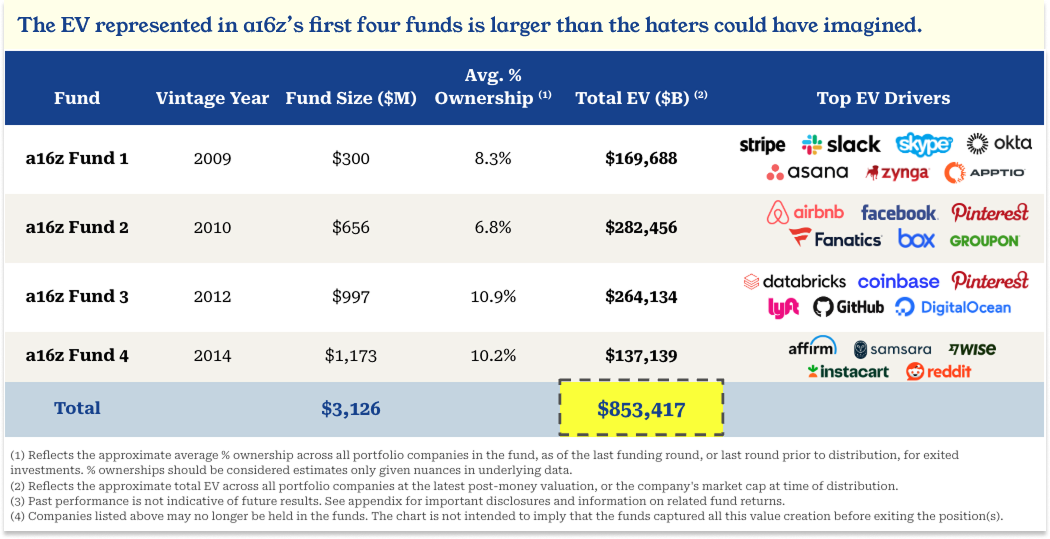

Like in 2015, when New Yorker writer Tad Friend sat down to breakfast with Marc Andreessen while writing Tomorrow’s Advance Man. Friend had just heard from a rival VC who wanted to get a word in - that a16z’s funds were so large, and ownership percentages so small1, that to get 5-10x aggregate returns across its first four funds, they’d need their aggregate portfolio to be worth $240-480 billion.

“When I started to check the math with Andreessen,” Friend writes, “He made a jerking-off motion and said ‘Blah-blah-blah. We have all the models—we’re elephant hunting, going after big game!’”

I want you to keep that image in your mind. To preempt Marc’s reaction to the reaction you’re about to have to the next paragraph.

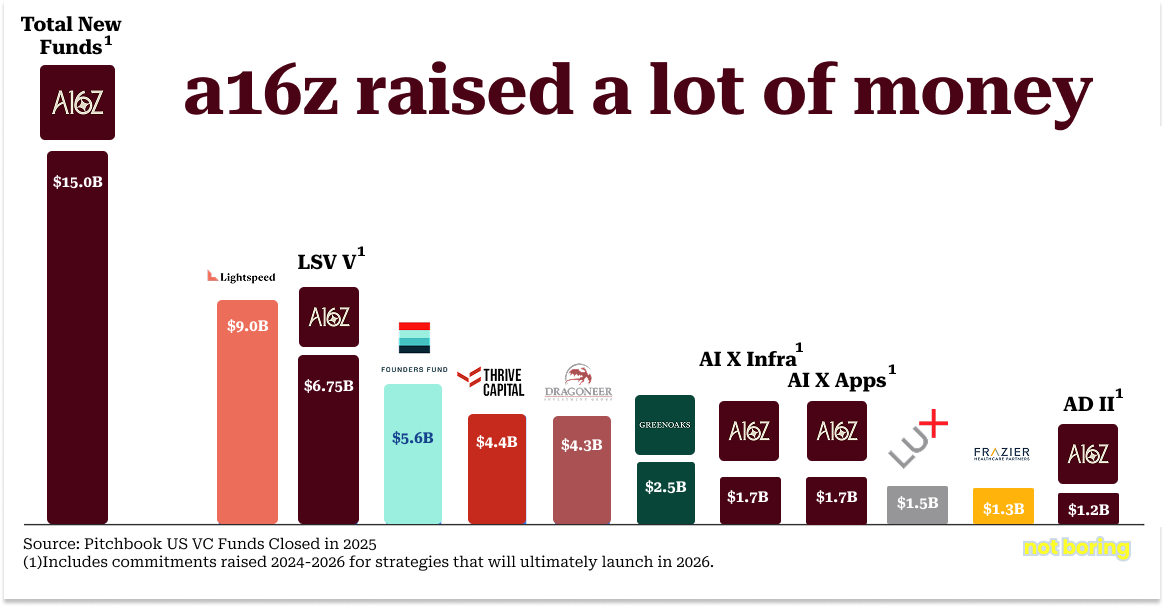

Today, a16z is announcing that it has raised $15 billion across all of its strategies, bringing its total regulatory assets under management (RAUM) to over $90 billion.

In a year in which venture fundraising was dominated by a small number of large firms, a16z raised more than the next two funds - Lightspeed ($9B) and Founders Fund ($5.6B2) - raised in 2025, combined.

In the worst VC fundraising market in five years, a16z accounted for over 18% of all US VC funds raised in 20253. In a year in which it took the average VC fund 16 months to close their fund, a16z took just over three months from start to finish.

Split up, four of a16z’s individual funds would be in the 2025 top 10 among entire firms’ raises: Late Stage Venture (LSV) V would be #2, Fund X AI Infra and Fund X AI Apps would be tied for 7th, and American Dynamism (AD) II would be tenth.

One could argue that this is way too much money for a venture fund to deploy with any reasonable expectation of generating outsized returns. To which, I imagine, a16z collectively makes a jerking-off motion and says, “Blah blah blah.” It is elephant hunting, going after big game!

Today, across all their funds, a16z is an investor in 10 of the top 15 private companies by valuation: OpenAI, SpaceX, xAI, Databricks, Stripe, Revolut, Waymo, Wiz, SSI, and Anduril4.

It has invested in 56 unicorns over the prior decade through its funds, more than any other firm5.

Its AI portfolio includes 44% of all AI unicorn enterprise value, also more than any firm6.

And from 2009-2025, a16z led 31 early rounds of eventual $5b companies, 50% more deals than the two next closest competitors.

It has all the models. It has the track record, now, too.

Below is the aggregate portfolio value of those first four funds, the ones that would have had to be worth $240-480 billion to clear that rival VC’s hurdle. Combined, a16z Funds 1-4 had a total enterprise value of $853 billion at distribution or latest post-money valuation7.

And that was just at the time of distribution. Facebook alone has added more than $1.5 trillion in market cap since!

Some form of this pattern keeps playing out: a16z makes a crazy bet on the future. Those in the know say it’s stupid. Wait some years. Turns out it’s not stupid!

a16z raised its $300 million Fund I in 2009 on the heels of the Global Financial Crisis, touting an operating platform to support founders. “We visited a lot of our VC friends and many of them said it was a really dumbass idea and we should definitely not pursue it and it’s been tried before and it didn’t work,“ Ben recalls. Today, nearly every significant VC has some flavor of platform team.

When it invested $65 million of that fund alongside Silver Lake and other investors to acquire Skype from eBay for $2.7 billion in 2009, “everyone said it was an undoable deal due to IP risk” (eBay was in litigation with Skype’s founders over the technology at the time of the deal). Ben recounted the skepticism in a blog post less than two years later when Microsoft acquired Skype for $8.5 billion.

Marc and Ben raised a $650 million Fund II in September 2010, and proceeded to make large late-stage investments in companies like Facebook ($50 million at $34 billion), Groupon ($40 million at $5 billion), and Twitter ($48 million at $4 billion), betting the IPO window would open. Rivals bristled to The Wall Street Journal in a classic, A Venture-Capital Newbie Shakes Up Silicon Valley, that private share deals were just not what venture capitalists did (the now-common practice was so new that the word “secondary” makes no appearance). Matt Cohler, a Benchmark partner, dropped this banger: “There’s also money to be made in pork bellies and oil futures, but that’s not what we do.” In November 2011, Groupon IPO’d, opening at $17.8 billion. In May 2012, Facebook IPO’d at $104 billion. And in November 2013, Twitter IPO’d, closing its first day at $31 billion.

By the time Marc and Ben raised a $1 billion Fund III and a $540 million parallel opportunities fund in January 2012, the criticism shifted to a familiar one: scale. a16z’s funds represented 7.5% of all US VC dollars raised in 2012, while VC kind of sucked. The 2014 Harvard Business School Case Study on a16z notes a 2012 Kauffman Foundation report which found that, “Venture capital has delivered poor returns for more than a decade.” In 2012, VC investments returned an average of 8.9% to the S&P 500’s 20.6% per Cambridge Associates. Legendary venture capitalist Bill Draper said, “The growing consensus about venture capital in Silicon Valley is that too many funds are chasing too few truly great companies.” Which certainly rhymes with today.

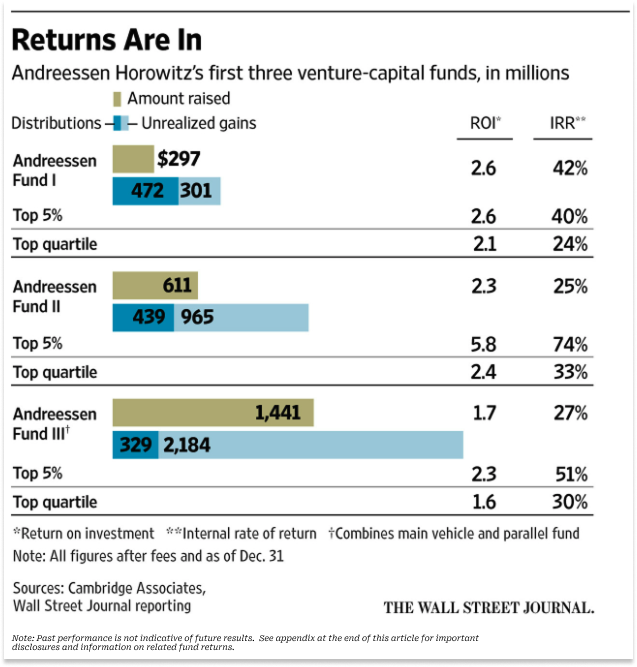

In 2016, The Wall Street Journal published an article that Acquired’s David Rosenthal called “so clearly a hit piece planted by rival venture firms” titled Andreessen Horowitz’s Returns Trail Venture-Capital Elite, when its funds were seven, six, and four years old, respectively. It showed that while AH Fund I was a top 5% VC fund, AH II was merely top quartile, and AH III was actually slightly outside of the top quartile.

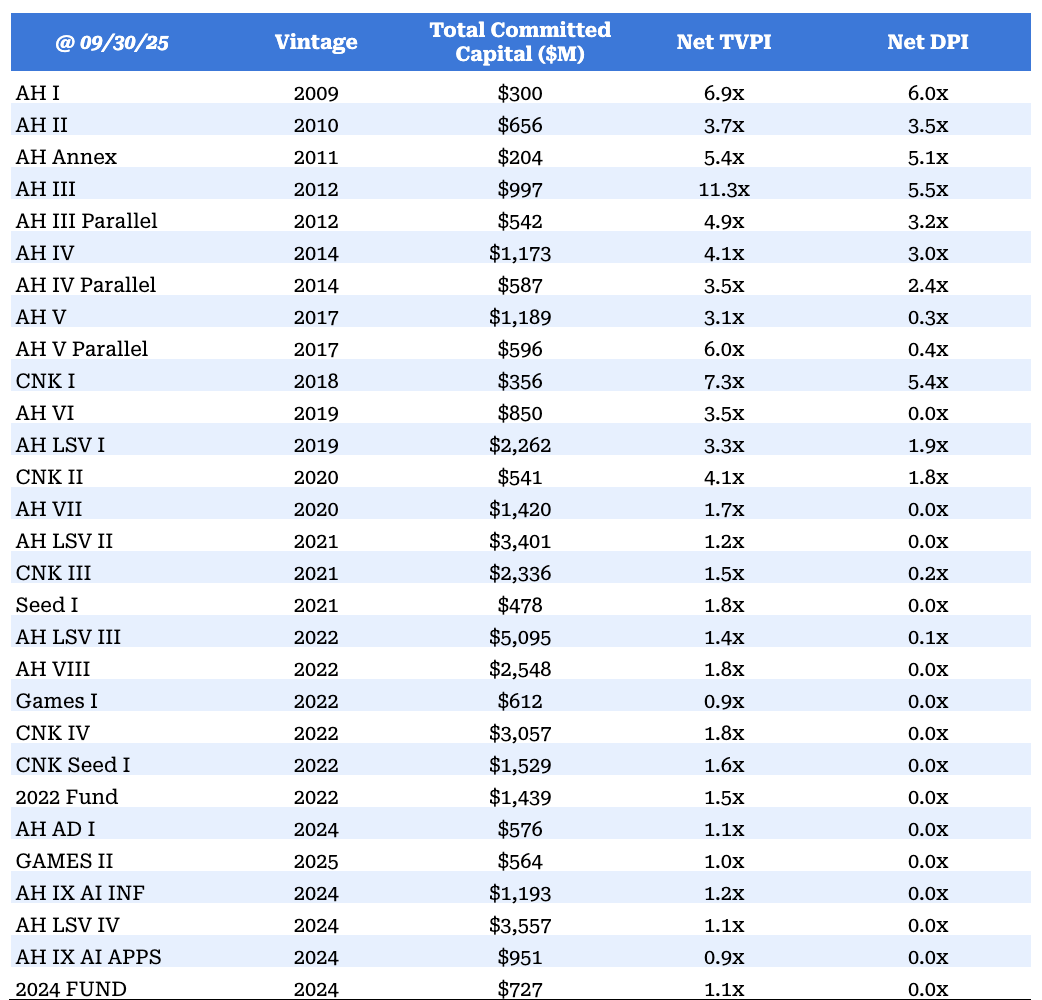

Which is funny, in hindsight, because that fund, AH III, is a monster fund: sitting at an 11.3x Net TVPI (total value to paid-in capital after fees) as of September 30 2025, and when you include the parallel fund, it’s at a 9.1x Net TVPI.

AH III includes Coinbase, which resulted in distributions of $7 billion gross to a16z LPs across the funds it’s in, Databricks, Pinterest, GitHub, and Lyft (although not Uber, proof positive that one sin of omission trumps every sin of commission), and I believe is one of the best performing large venture funds of all time. Since Q3 2025, Databricks (currently a16z’s largest position) raised at $134 billion, which means Fund III’s performance is even stronger now (assuming other positions have not decreased). a16z has already distributed $7 billion net to LPs from AH III and AH III Parallel with nearly as much in Unrealized Value still on the table.

Much of that unrealized value sits in one company, Databricks: a big data company that was very small, still a few months away from hitting the half-billion-dollar valuation mark, when the WSJ was writing off a16z in 2016. Databricks represents 23% of a16z’s Net Asset Value (NAV) across all funds.

Spend any time around a16z and you will hear the name Databricks a lot. In addition to being its largest position (and what must be a top three largest dollar position in all of venture capital), its story is the cleanest example of how a16z operates at its best.

Databricks & the a16z formula

There are some things about the Firm we haven’t discussed yet that are useful to understand before we start talking about Databricks.

First, a16z is founded and run by engineers. Not just founders, engineer-founders. This influences how they designed the Firm (to feast on scale and network effects), and also how they pick markets and the companies within them.

Second, there is perhaps no bigger investing sin at a16z than investing in second best. If you miss a winner early, you can always invest in a later round. If you invest in second best, you lock yourself out from investing in the winner. This is true even if the eventual winner isn’t yet born.

Third, once a16z believes it has identified the category winner, the classic a16z move is to give it more money than it thought it needed. Everyone makes fun of them for that move.

These three things have been true since the Firm’s earliest days.

Back in the early 2010s, just a couple of years into the founding of Andreessen Horowitz, Big Data was the Big Thing (you remember this) and the era’s dominant Big Data framework was Hadoop. Hadoop used a programming model called MapReduce (originally developed by Google) to distribute computing across clusters of cheap commodity servers instead of on expensive specialized hardware. It ~*Democratized Big Data*~ and a wave of companies sprung up to facilitate and capitalize on that democratization. Cloudera, founded in 2008, raised $900 million in 2014, leading a year in which investment in Hadoop companies had quintupled to $1.28 billion. Hortonworks, spun out of Yahoo!, IPO’d that year.

Big data, big dollars. And a16z made none of them.

Ben Horowitz, the “z” in a16z, didn’t like Hadoop. A computer science major before he was CEO of LoudCloud/OpsWare, Ben didn’t think Hadoop was going to be the winning architecture. It was notoriously difficult to program and manage, and Ben thought it was poorly suited for the future: every step in a MapReduce computation wrote intermediate results to disk, which made it painfully slow for iterative workloads like machine learning.

So Ben sat out the Hadoopla. And Marc, Jen Kha told me:

Was just giving him so much shit, because at that point, Hadoop was taking over the headlines, and he was like, ‘We fucking missed it. We totally bungled this. We dropped the ball.’

And Ben was like, ‘I don’t think this is the next architectural shift.’

Then finally, when Databricks came around, Ben said, ‘This might be it.’ And he of course just bet the farm on it.

Databricks came around just in time and just down the road in UC Berkeley.

Ali Ghodsi and his family fled Iran in 1984 during the Iranian Revolution and moved to Sweden. His parents bought him a Commodore 64, which he used to teach himself how to code, well enough, in fact, to get invited to UC Berkeley as a visiting scholar.

At Berkeley, Ali joined the AMPLab, where he was one of eight researchers, including thesis advisors, Scott Shenker and Ion Stoica, working to implement the idea in Ph.D. student Matei Zaharia’s thesis paper and build Spark, an open source software engine for big data processing.

The idea was to “replicate what the big tech companies did with neural networks without the complex interface.” Spark set the world record for data sorting speed and the thesis won the award for best computer science dissertation of the year. True to academic form, they released the code for free, and barely anyone used it.

So starting in 2012, the eight met for a series of dinners, over which they decided to team up to start a company on top of Spark. They called it Databricks. Seven of the eight joined as cofounders, and Shenker signed on as an advisor.

Databricks, the team thought, would need a little money. Not a lot, but some. As Ben recounted to Lenny Rachitsky:

“When I met with them they were like, ‘We need to raise $200,000.’ And I knew at the time that what they had was this thing called Spark and the competitor was something called Hadoop, and Hadoop had very well-funded companies already running towards it, and Spark was open source, so the clock was ticking.”

He also realized that as academics, the team would be pre-disposed to doing something small. “Professors in general… it’s a pretty big win if you start a company and you make $50 million. Like you’re a hero on campus,” he told Lenny.

Ben had bad news for the team: “I’m not going to write you a check for $200,000.”

He also had really good news for the team: “I’ll write you a check for $10 million.”

His reasoning was, if you’re going to build a company, “You need to build a company. You need to really go for it if you’re going to do this. Otherwise, you guys should stay in school.”

They decided to drop out. Ben upped the check size and a16z led Databricks’ Series A at a $44 million post-money valuation. It owned 24.9% of the company.

This initial encounter - Databricks asking for $200k, a16z going much, much bigger - set a pattern. When a16z invests in you, they believe in you.

When I asked him about a16z’s impact, Ali was unequivocal: “I don’t think Databricks would be around today if it wasn’t for a16z. And Ben specifically. I don’t think we would be around. They truly believed in us.”

In the company’s third year, it was only doing $1.5 million in revenue. “It was far from clear that we would make it,” Ali recalls. “The only person that truly believed it was going to be worth a lot was Ben Horowitz. Much more so than us. Mind you, like, much more than me. To his credit.”

Belief is a cool thing to have. It’s even more valuable when you have the power to make it self-fulfilling.

Like in 2016, when Ali was trying to get a deal done with Microsoft. From his perspective, with overwhelming demand to have Databricks on Azure, it was a no-brainer. He asked some of his VCs for introductions to Microsoft VC Satya Nadella, which they did, but then those introductions got “buried in executive assistant loops.”

Then Ben introduced Ali to Satya properly. “I had an email from Satya saying, ‘We’re absolutely interested in having a very deep partnership,’” Ali recalls, “adding his lieutenants, and their lieutenants. Within a couple hours, I had 20 emails in my inbox, from Microsoft employees who I had tried to talk to before, and they were all like, ‘Hey, when can we meet?’ And it was like, ‘Okay, this is different. This is going to happen.’”

Or in 2017, when Ali was trying to recruit a senior sales executive to keep the foot on the gas. The executive wanted change of control provisions in his contract – essentially, accelerated vesting if the company gets acquired.

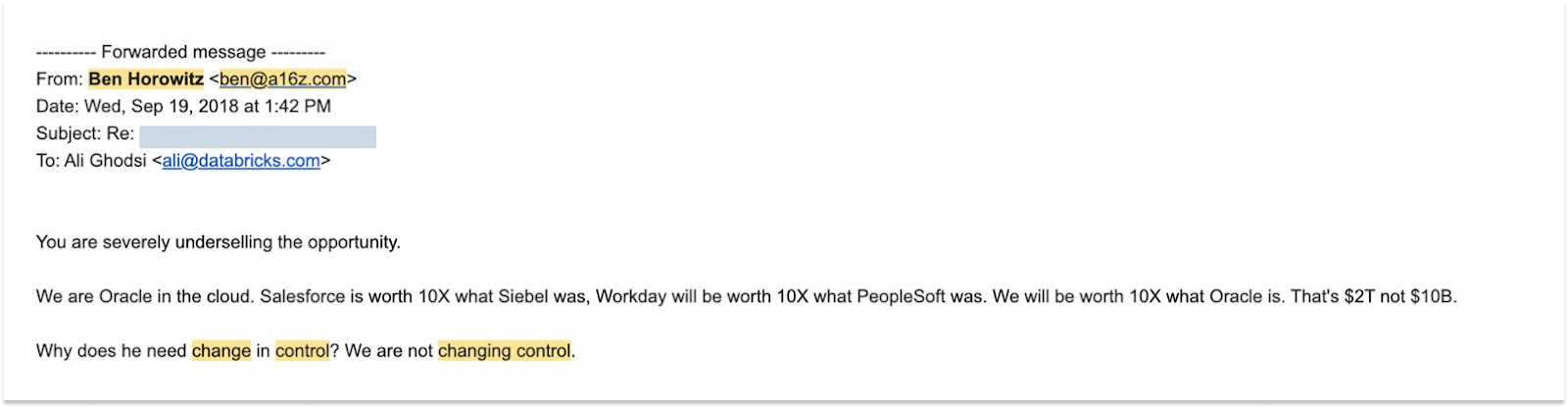

It was a sticking point, so Ali asked Ben to help convince the guy that the value of Databricks was “at least $10B.” Ben talked to him, and then sent Ali this email:

“You are severely underselling the opportunity.

We are Oracle in the cloud. Salesforce is worth 10X what Siebel was. Workday will be worth 10X what PeopleSoft was. We will be worth 10X what Oracle is. That’s $2T not $10B.

Why does he need change in control? We are not changing control.”

That’s one of the hardest corporate emails of all time, especially considering that Databricks was worth $1 billion at a $100 million revenue run rate then and is worth $134 billion at a more than $4.8 billion revenue run rate now.

“They envision the full potential of the thing,” Ali tells me. “When you’re knee deep in it, like we are operating every day, and you’re seeing all the challenges—the deals are not closing, the competitors are beating you, you’re running out of money, no one knows who you are, people are quitting on you—it’s hard to think about the world that way. But then they come to the board meetings and they tell you, ‘You’re going to take over the world.’”

They were right, and they’re getting paid for their belief. All told, a16z has invested in all twelve Databrick’s funding rounds. It has led four of them. The company is one of the reasons AH 3, from which the Firm did its initial investment, is doing so well, and it is a driver of returns in the larger Late Stage Ventures Funds 1, 2, and 4.

“First and foremost, they just really care about the mission of the company. I don’t think Ben and Marc think of it as an investment return first. That comes second,” Ali observed. “They’re tech believers who want to change the world with technology.”

If you don’t understand what Ali said about Marc and Ben, you will not understand a16z.

What is a16z?

a16z is not a traditional venture capital fund. On its face, this is obvious! It just completed the largest VC fundraise across all of its strategies since SoftBank’s $98 billion Vision Fund in 2017 and Vision Fund II in 20198. Nothing traditional about that. But even the SoftBank Vision Fund was a Fund. a16z is not that.

Of course, a16z has raised money and needs to generate returns. It needs to be great at this, and to date, it’s been exceptional. Not Boring has returns data on a16z’s funds to date that we will share below.

But first - what is a16z?

a16z is a cult of technology. Everything it does is to bring about better technology to make the future better. It believes that “Technology is the glory of human ambition and achievement, the spearhead of progress, and the realization of our potential.” Everything flows from that. It believes in the future and bets the firm that way.

a16z is a Firm. It is a business, a company. It is built with the goal to scale, and to improve with scale. There are many characteristics of a Firm that I believe do not apply to a traditional Fund, and we will cover them. I think this distinction solves one of the oddest things about venture capital’s self-image: that venture capital is an industry that sells the world’s most scalable product (money) to its most scalable companies (technology startups) but must not, itself, scale.

This distinction - Firm > Fund - comes from a16z GP David Haber, the most East Coast Finance of the bunch and a self-described student of investment firms as businesses. “The objective function of a fund is to generate the most carry with the fewest people, in the shortest amount of time possible,” he explains. “A Firm is about delivering exceptional returns, and building sources of compounding competitive advantage. How do we get stronger with scale, not weaker?”

a16z is run by engineers and entrepreneurs. Money managers stereotypically try to grab larger pieces of a fixed pie. Engineers and entrepreneurs try to grow the pie by building and scaling better systems.

a16z is a temporal sovereign. It is the institution for the future. The Firm, in its more ambitious moments, views itself as a peer to the world’s leading financial institutions and governments. It has said that it aims to be the (original) JP Morgan for the Information Age, but I think that undershoots the true ambition. If governments work on behalf of chunks of space, a16z works on behalf of that big chunk of time that is the future. Venture capital is simply the way that it’s found it can have the biggest impact on the future, and the business model most aligned with profiting when it does.

a16z makes and sells power. It builds its own power through scale, culture, network, organizational infrastructure, and success, and then gives its power to the technology startups in its portfolio through sales, marketing, hiring, and government relations, primarily, although to hear its founders tell it, a16z will do whatever is in its power to do, which seems to be a lot.

If you were designing such an institution, one that believes that technology is “eating markets far larger than the technology industry has historically been able to pursue,” that Everything is Technology, what you would build is a company that sells the power to win to the hundreds and thousands of companies that might one day come to be the economy. I think you would build an institution that looks a lot like a16z.

Because the companies that might one day become the economy start small and fragile. They start diffuse, each with their own goals and competitors; often, they compete with each other. And they face entities that dominate the present, with no desire to cede ground to new entrants. A small company, no matter how promising, may not be able to hire the very best recruiters who can hire the very best engineers and executives. It might not be able to advocate for policies to give itself a fair shot. It may not have the audience to get its message out to the world in a way that people will listen. It may not have the legitimacy to sell its products to governments and large enterprises who are flooded with pitches promising the next big thing.

It doesn’t make sense for any one small company to invest the billions of dollars it would need to create those capabilities and amortize them over only itself. But if you can amortize those capabilities across all of those companies, across trillions of dollars of future market value, then all of a sudden, the small companies can have the resources of the big companies. They can win or lose on the merits of their product. They can bring about the future the way it should be.

What if you could combine the agility and innovation of a startup with the power and heft of a temporal sovereign?

That’s what a16z is trying to do, and has been trying to do since it was a startup itself.

This post continues on Not Boring

Appendix

Important Disclosures Related to Performance

This appendix is provided for informational purposes only and does not constitute an offer to purchase any interest in any fund managed by a16z Capital Management, LLC (“ACM”). This document’s information should not be relied upon in any manner as legal, tax, investment or accounting advice. An investment in any fund managed by ACM involves a high degree of risk including a risk that the entire amount invested is lost. Further, Certain statements herein reflect the views of limited partners and may constitute endorsements. No compensation was provided in connection with these statements; however, such limited partners have a financial interest in the adviser.

All figures as of 09/30/25 unless otherwise noted. All performance figures, valuations and fund summaries contained herein are unaudited and subject to change. Past performance is not indicative of future results. There can be no assurances that any future a16z Capital Management, LLC fund or investment will achieve comparable results. Furthermore, performance of any future ACM fund will not be comparable to performance of existing funds due to material differences in market conditions, differences in investment strategy and other factors. No individual investor or fund received investment performance illustrated above.

Gross performance figures provided herein do not represent and should not be used as a substitute for the actual returns delivered to limited partners of the respective funds. Performance figures of certain funds reflect the use of a warehouse, capital call, or similar line of credit. Performance would differ if calculated from the time of the opening of such line of credit rather than from the initial contribution of capital and may be lower. Performance includes performance for the primary or “main” fund identified herein as well as any vehicle that aggregates capital from multiple unaffiliated investors for the primary purpose of investing directly into such primary fund, including those funds which do not charge a management fee or carried interest. If such funds were excluded, performance would be lower. Fund performance does not include funds in ACM Bio and Health strategy or the Cultural Leadership Fund strategy; single-investor vehicles; or special-purpose/single-investment vehicles (SPVs), unless specifically mentioned.

Performance figures include reinvested capital and may differ if such performance was excluded. Performance reflects voluntary General Partner fee waivers and would be lower if such fee waivers were excluded. Any investments and portfolio companies described or referred to in this report are not representative of all investments in vehicles managed by ACM and there can be no assurance that the investments described are or will be profitable or that other investments made in the future will have similar character or results. Performance figures do not include all investment funds managed by ACM. Visit a16z.com/portfolio for a list of all investments in a16z-managed vehicles.

Gross/Net Total Value to Paid-In Capital (TVPI): represents the sum of (1) the aggregate amount of distributions made to the all limited partners of those Funds and (2) the fair value of all limited partners’ capital accounts as of the end of the period indicated expressed as a multiple of the aggregate amount of capital that has been contributed by all limited partners of a given fund. Net includes the effect of management fees, fund expenses and carried interest allocations.

Net DPI: Net Distributions to Paid in Capital for ACM funds represent the aggregate amount of distributions made to the limited partners of those funds expressed as a multiple of the aggregate amount of capital that has been contributed by those limited partners of a given fund.

Gross Metrics (Fund-Level): Includes cash still held, and any other assets and liabilities of the Fund. Gross return adds back management fees, carried interest, and fund expenses.

The rival’s analyst crunched the numbers and estimated 7.5%. Close. Andreessen Horowitz’s average ownership in its portfolio companies was 8%.

Pitchbook data lists Founders Fund Growth III ($4.6B) and Founders Fund IX ($972M) closed in 2025.

Per Pitchbook, US VC funds raised in 2025 totaled $82.0B, including a16z’s $15B.

Source: Valuations per Pitchbook as of September 14, 2025.

Source: Ilya Strebulaev, Venture Capital Initiative, Stanford GSB, April 2025.

Source: Based on Pitchbook data available as of July 31, 2025. Excludes AI unicorns in China and Hong Kong.

Past performance is not indicative of future results. See appendix for important disclosures and information on related fund returns.

I see you, Insight Partners fans. The $20B Fund XII it raised in 2022 includes a Buyout fund.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

| A guest post by

|

Packy, I had unsubscribed from your Substack long ago. Reading this made me subscribe again. Keep writing more such stuff.

Packy, Excellent article. Great story. I will reread it again. I have been following A16Z for a long time. I remember when Ben spoke on a podcast more than 10 years back about his investment thesis and how he met Doug Cutting from Hadoop ( If my memory serves right). Also, on the same podcast, Ben talked about how he met Ali from Databricks (in fact it was not even called Databricks then). He mentioned about a startup in Berkeley that they are investing and wanted to keep it confidential. It came to be Databricks later. What a sea change in the last 12-13 years !!