America’s Energy Problem Isn’t Supply. It’s Delivery.

Solid-state transformers have the power to solve today’s critical energy needs - safely, reliably, and affordably.

America | Tech | Opinion | Culture | Charts

Drew Baglino is founder and CEO of Heron Power, an industrial power electronics company focused on affordably scaling electrification. He is formerly a longtime engineer turned executive as SVP of Powertrain and Energy at Tesla.

The US electricity grid is one of the greatest infrastructure achievements in history. Built over a few remarkable pioneering decades, it now spans an entire continent and has served incredible growth throughout our cities and society. But this infrastructure has been quietly aging and much of the grid is now approaching end of life at the exact moment we desperately need it to support tremendous growth.

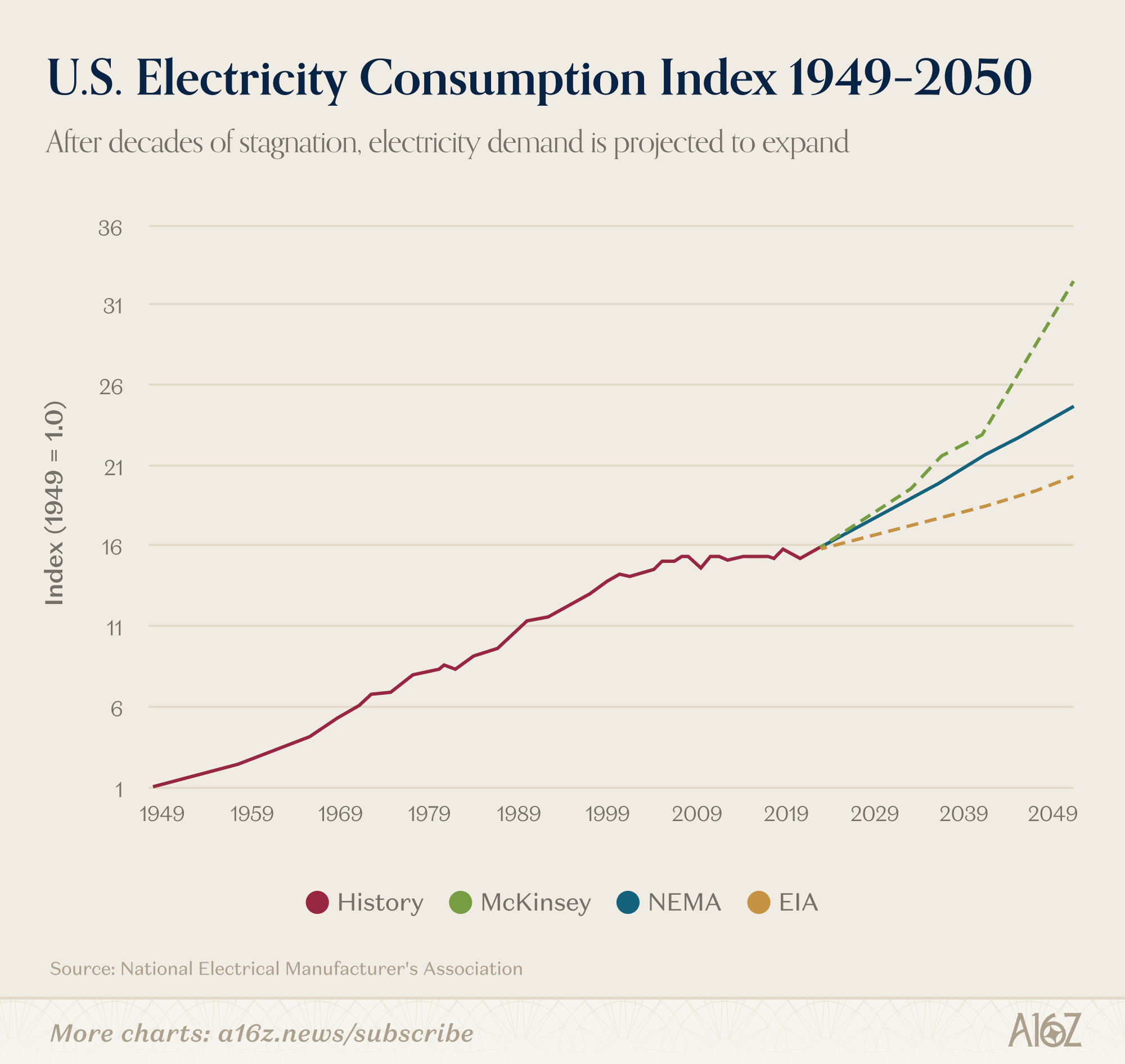

Electricity demand is accelerating faster than at any point in a generation — driven by datacenters, electric vehicles, heat pumps, re-industrialization, and AI. Every indicator points to that growth continuing: more of our energy economy runs on electricity each year, and more of that electricity comes from renewables. Getting to a fully electrified economy means generation needs to grow more than four times from today’s levels — and that estimate doesn’t yet account for the next wave of AI infrastructure now coming online.

I founded Heron Power in 2024 because I believe the grid itself is the next frontier for power electronics. The engineering capability exists. The talent exists. What’s needed now is the same concentration of focus, urgency, and scale that transformed electric transportation — directed at the infrastructure that powers everything else.

We are asking a nineteenth-century grid to power a twenty-first-century economy.

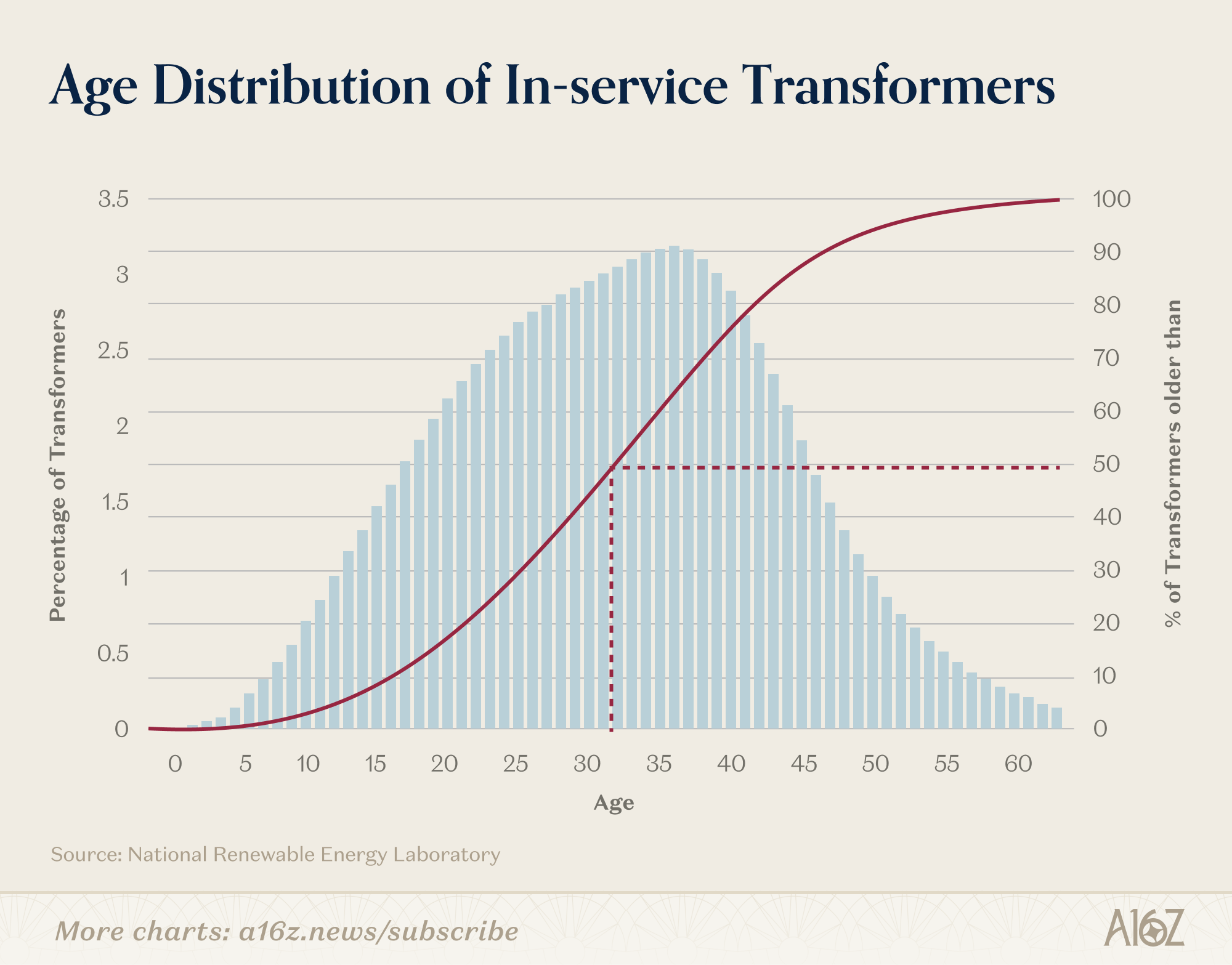

Electricity demand growth is running headlong into physical limits. In the US, seventy percent of transmission lines and large power transformers are over 25 years old, and more than half of all distribution transformers are nearing the end of their useful lives. In 2025, the American Society of Civil Engineers gave U.S. energy infrastructure a D+.

We have to renew existing infrastructure while planning for the future, and we have to do it affordably. The minute power bills jump, public support weakens, regulators get cautious and necessary projects stall. Every rate case is a balancing act between investing in new infrastructure and keeping power affordable. If utilities can’t serve future demand without higher rates, approvals slow down. And if bills rise anyway, the backlash ripples as delay and disruption to entire growth sectors.

That is why the next wave of grid investment must be different. We cannot simply replace aging equipment with more of the same. We need a new generation of grid-scale solutions that unlock capacity, increase utilization, improve reliability, and reduce loss — without pushing costs onto customers. A sustainable economy can only grow as fast as affordable electricity can propel it.

The superpowers of power electronics

The hero of this story is power electronics. Advances in computing, communications, heat pumps, renewable energy, efficient lighting, battery storage. Electric cars, AI datacenters, next-generation manufacturing. None of these scale without efficient, reliable, high-performance power conversion. Five decades of continuous advancement in power electronics has quietly enabled nearly every major technology of our era.

I saw this firsthand over nearly two decades at Tesla, where I led the development and scaling of electric vehicle drivetrains, battery storage, and fast-charging infrastructure — none of which would have been possible without power electronics. By combining the best available device technology with rigorous engineering and manufacturing at scale, we transformed industries and unlocked cost curves that once seemed unreachable. But I also kept running into the same wall: progress at the grid’s edge was consistently outpacing the infrastructure on the other side of the wire. The build out of energy installations and factories stalled — not for lack of capital, technology, or permits, but because the grid equipment they needed to connect to was undersized, supply-constrained, or prohibitively expensive.

What’s limiting the grid

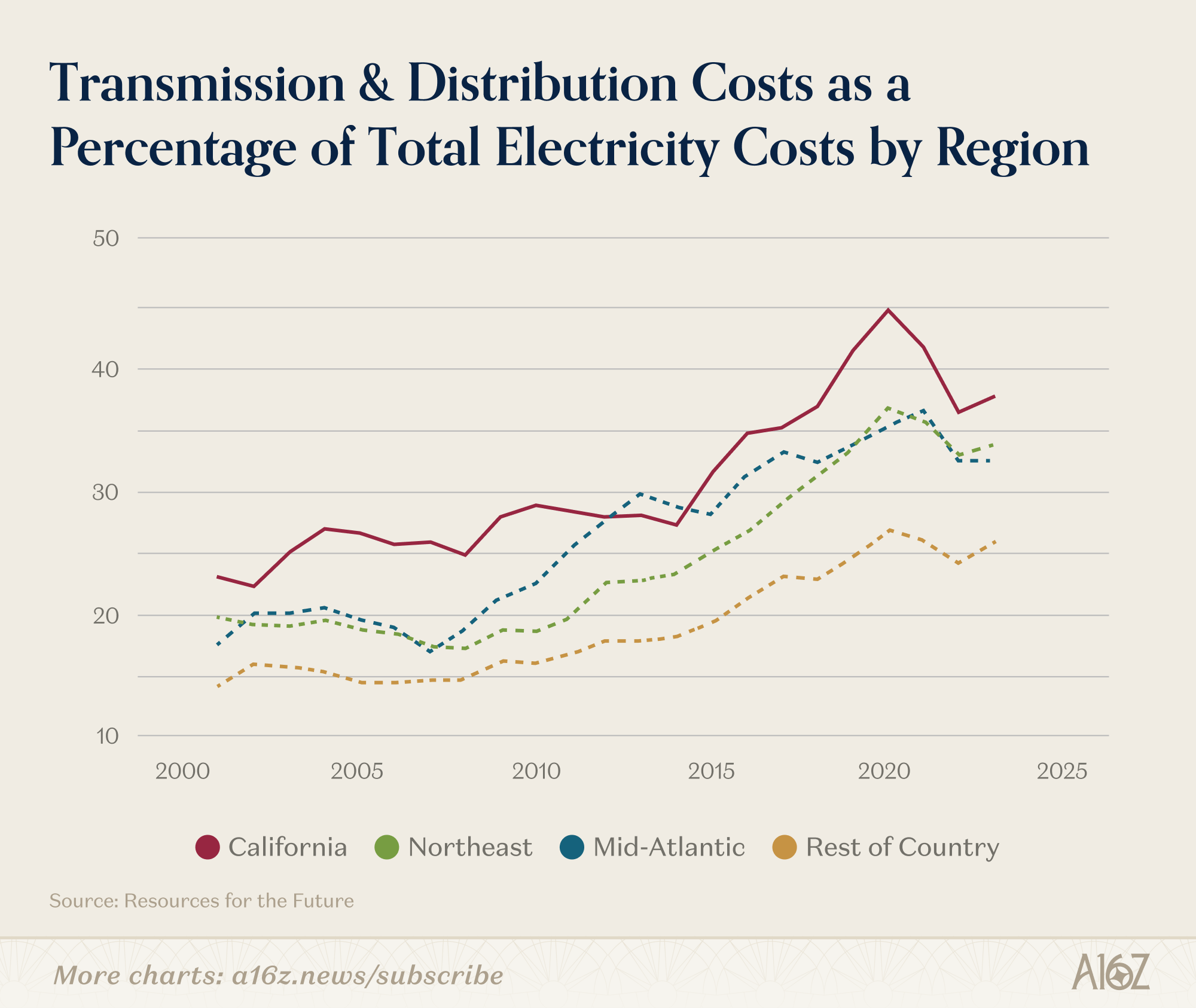

Since 2019, average residential electricity rates have climbed roughly 25-30%. But the cause isn’t what most people assume. Generation costs have actually declined — natural gas expanded, wind and solar fell dramatically, battery storage reached grid scale. The problem is delivery. Transmission and distribution now accounts for nearly half of what customers pay in many regions. Generation is getting cheaper, but delivery is more expensive. The net result is more expensive power.

Two structural problems explain why.

First, incentives are misaligned. Regulated utilities earn returns on capital deployed — the more they spend building, the more they earn. Decades of flat demand left equipment suppliers with little pressure to innovate. When the only tools available are large, slow, hardware-heavy upgrades, investment scales accordingly. Much of this spending is necessary — replacing aging assets, hardening against wildfires, expanding to serve new loads. But the incentive structure means there’s no natural brake on inefficient deployment.

Second, the system is engineered conservatively by necessity. Keeping the lights on is a literal matter of life and death, requiring simultaneous management of supply-demand balance, frequency, voltage, line congestion, fault-isolation and power quality in real time. Operators value reliability over cost minimization. Batteries and VPPs are making headway — aggregated home batteries and utility-controlled VPPs can defer pole and wire upgrades — but capacity is only part of the equation. Planners still need to solve for everything else, and today’s equipment gives them few tools to do so.The basic hardware hasn’t fundamentally changed in decades. Large mechanical switchyards direct power flow, breakers and reclosers protect circuits slowly with wide safety margins. The equipment is durable, but blunt. It does not sense or control dynamically. It cannot actively optimize. Transformers — on telephone poles, in green boxes in your neighborhood — convert voltage at a fixed ratio. No sensing. No telemetry. No control. Without visibility at each node, planners assume worst-case scenarios and overbuild accordingly.

An aging supply chain compounds the problem. Transformer demand has more than doubled since 2019, costs are up 80%, and the U.S. faces a 30% supply deficit. A single grossly under-capacitized domestic producer makes the steel required to build them. Eighty percent of supply is imported — for the most critical component of our infrastructure, at the exact moment we need to scale it.

The deeper challenge is distributed electrification: millions of EV chargers, heat pumps, rooftop solar, and commercial fleets connecting to circuits designed for a different world. These loads are dispersed, variable, and increasingly bidirectional. These are tractable problems for operators with dispatchable, continuous control of power flow. But with today’s passive, mechanical, analog equipment, planners default to what they know — overbuilding.

The problem is clear as day. If we want Americans to have affordable access to the abundant power we can now freely generate and propels prosperity, growth, and sustainability, things must change. We need better tools: tools to extract more capacity, more reliability, and more flexibility from the infrastructure already in the ground.

Applying Moore’s Law to power

Fortunately better technology exists today, born of decades of innovation in power semiconductors. Before they arrived, electrical engineers could only use mechanical devices to control current — think the light switch in your home, or the electro-mechanical relay that locks your car door. These switches are slow to change state, degrade as arcs pit their contacts over time, and top out at 5,000–10,000 lifetime cycles. At home wiring voltages they’re manageable, but at higher voltages they grow to the size of refrigerators — painfully expensive, and slow to actuate. In all cases, electrical switches that are fundamentally mechanical in nature have limited lifetime.

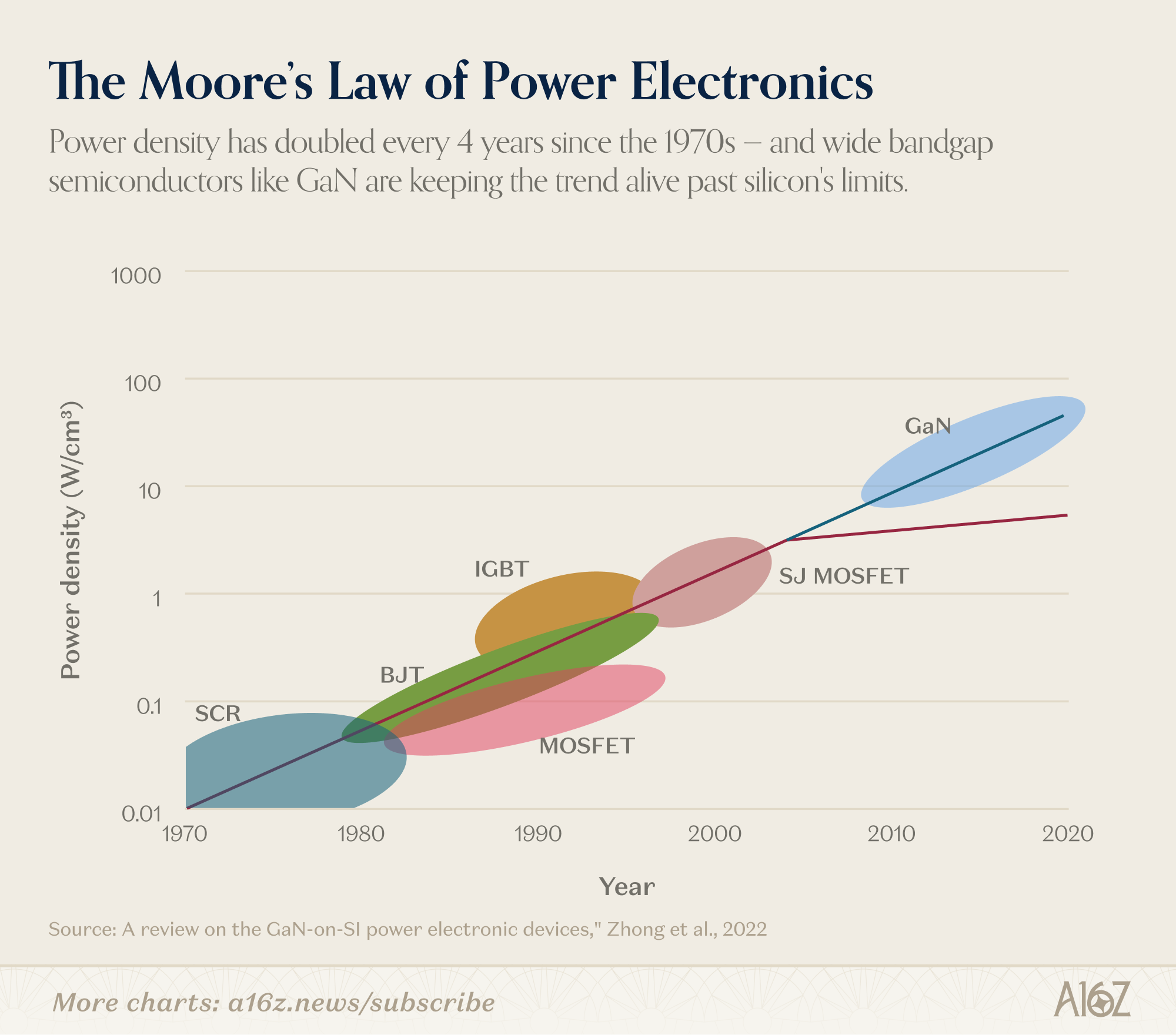

In the late 1970s and early 80s, pioneering scientists unlocked an entirely different class of device and entirely new means of controlling electricity. Thyristors, power diodes, and IGBTs could switch on and off in microseconds, block high voltages, and cycle trillions of times without fail. Power electronics enable electricity to control itself: in the right circuit topologies, engineers apply them to convert AC to DC, DC to AC, control power flow, or step between voltage levels with precision. Much like transistors in compute, power semiconductors have followed their own Moore’s law — smaller, faster, cheaper, and dramatically more capable on a relentless curve of improvement.

Since power semiconductors were first industrialized in the early 1980s, device switching speeds have improved by four orders of magnitude and current density by more than three. Fifty years ago, silicon MOSFETs switched in hundreds of microseconds and blocked 60–100 volts. Today, silicon carbide MOSFETs switch in nanoseconds and block thousands of volts in a millimeter-scale package. The power semiconductor business now generates roughly $60 billion in annual sales, enabling terawatts of new conversion capability every year.

And every step along that curve has unlocked new industries. Variable frequency drives transformed industrial efficiency in the 80s and 90s by precisely matching motor speed to load. In the 2000s, continued advances supported the build out of solar, wind and industrial automation. In the 2010s, another leap in performance helped EV powertrains and utility-scale batteries move into the mainstream. Today, a 140-watt USB-C charger uses GaN semiconductors switching a million times per second, packs 20X more power density than a comparable 1990s power supply, uses adaptive controls to share power across ports, and runs cool enough to require no fan at all. Each generation: lower cost, higher efficiency, higher power density.

The major inflection for higher-voltage applications came with silicon carbide (SiC), a semiconductor perfect for power. SiC devices operate at higher voltages and switching frequencies with less loss, run cooler, and enable smaller, more efficient converters than traditional silicon. It’s also an American success story — the technology emerged from North Carolina State and was commercialized by Cree, now Wolfspeed, in the 90s in Durham. Global competition is accelerating, and we should consider the national security priority of power chips alongside next-generation GPUs.

I lived this transition firsthand at Tesla. The 2006 Roadster and 2012 Model S used silicon IGBTs in their traction inverters. With the 2017 Model 3, we bet on SiC MOSFETs — and it paid off in efficiency, range, thermal performance, and package size. That same decision shaped the success of Megapack. Today most major EV and storage companies have followed, with more than two terawatts of SiC-enabled devices deployed in EVs alone every year.

Five decades in, nearly all power semiconductor progress has accrued to low-voltage applications: telecoms, datacenters, vehicles, chargers, solar, batteries. The distribution grid, operating at medium voltage between 7.2kV and 34.5kV, remains dominated by passive, mechanical hardware.

Medium voltage is the next frontier.

Solid-state transformers: one solution for many problems

Today’s best silicon carbide devices block up to 3.3 kilovolts and switch at hundreds of kilohertz. That combination makes something genuinely new possible: modular, medium-voltage, high-frequency power electronics stages that replace passive 60-hertz oil-filled transformers with software-controlled silicon. The latest SiC devices are more than a better switch. They are the foundation for solid-state transformers, or SSTs. Since the 2000s, SSTs have been at the forefront of research into medium-voltage applications and grid integration. Leading academic contributors such as Alex Q. Huang (NC State, FREEDM Systems Center), Marco Liserre (Kiel University), and Frede Blaabjerg (Aalborg University), along with institutions like UT Austin, RWTH Aachen, and Tsinghua University, have shaped the field.

Where a conventional transformer is a passive iron core on a pad, an SST is a software-defined power-conversion platform. It consolidates voltage conversion, fault isolation, power factor correction, frequency regulation, harmonics control, and phase balancing into a single package, managed in real time by software, far smaller and more power-dense than anything it replaces. Reliability comes not from mass and simplicity, but from modularity where no single failure is fatal, real-time monitoring that catches problems early, and protective response measured in microseconds. SiC devices already survive decades of thermal and electrical stress in EVs and grid storage. Bringing that durability to medium voltage is an engineering challenge, not a physics barrier.

The economics are compelling across every customer type. For solar and battery developers, NREL research found inverter failures accounted for 36% of lost energy in utility-scale systems over a 27-month study period, with inverters failing 300 to 500 times more frequently than PV modules. An SST with built-in redundancy and real-time monitoring directly attacks that problem. For utilities, an SST replaces not just a transformer but the switchgear, tap changers, capacitor banks, and phase balancers that utilities can rarely afford to deploy at scale. Every passive node replaced becomes a programmable one.

The cost trajectory only moves one direction. Power semiconductors get cheaper and more capable with every generation and scale economy. Steel and copper follow commodity cycles and are never structurally cheaper. And because SSTs are software-defined, they improve after installation. A conventional transformer that’s wrong for the job gets ripped out and replaced. An SST gets a firmware update.

Combined with distributed resources, the compounding effect on grid planning is significant. Batteries provide capacity. SSTs offer a new paradigm of visibility and control at the circuit level to maximize how much power existing infrastructure can serve. Move more kilowatt-hours across the same poles and wires with less capital and lower maintenance costs, and rates stabilize or fall. That can be deployed now, on circuits already scheduled for replacement.

Building a grid for the future

The grid will be rebuilt. Aging equipment will be replaced and demand will continue to grow. The only real question is whether we replace yesterday’s hardware with more of the same, or with systems designed for a more dynamic, electrified economy.

Grid hardware deployed today will remain in service for decades. It must support higher load density, distributed generation, bidirectional power flow, and tighter reliability requirements. It must do more than convert voltage. It must sense, respond, and adapt.

We have seen this transition before. Telecommunications moved from fixed-function electro-mechanical systems to programmable, software-defined networks. Costs fell, capacity expanded, and entirely new mobile and cloud industries emerged on top. Power is at a similar inflection point. There is real work ahead: solid-state transformers must integrate with existing protection systems, satisfy cybersecurity requirements, and prove long-term reliability in the field. But these are engineering challenges, not scientific ones. The physics is proven. The semiconductor supply chain exists. The capital will be deployed regardless.

The only choice is what we build. A grid rebuilt from passive equipment locks in today’s constraints for another generation. A grid rebuilt from active, programmable, multi-function SSTs gets smarter, more efficient, and more capable every year. It carries more power across the same infrastructure, stabilizes rates, and creates the foundation for everything the next economy will demand.

America has scaled transformative technologies before, from aerospace to semiconductors to the internet, when engineering and economics align behind a clear mission. The grid is that mission now. The tools exist. The need is urgent. And the opportunity, for the first time in a century, is to deploy dynamic, controllable hardware solutions that maximize our existing infrastructure and unlock future growth.

The future needs more electricity. Let’s build a grid worthy of delivering it.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.

I can't understand why founders given the opportunity to guest post on the a16z Substack choose to post AI slop. Do you think we can't tell??

Seems a waste of a great opportunity to attract top-tier talent and raise your company's profile.

I really enjoyed your newsletter. Thank you.

I had a few questions about what you wrote, and I was wondering if it would be okay to ask you personally.

Would you be willing to send me an email? I can reply with my questions.

davidkimxlab@gmail.com

Or if you prefer, please let me know your email address and I will reach out first.

I would really appreciate your reply.