America | Tech | Opinion | Culture | Charts

Finance is a world of verticals, and each vertical has anointed its “one true conference.” Providers, payors, and biotech leaders gather every year in San Francisco for the J.P. Morgan Healthcare Conference. Global macro titans and politicians make their yearly pilgrimage to the Swiss Alps for Davos. TMT, Real Estate, Industrials, Financial Services, and every other sector under the sun has a marquee summit.

At the end of March, Kalshi Research, the academic and institutional research arm of Kalshi, hosted its first-ever Research Conference in New York, bringing together academics, Wall Street executives, former politicians, and the traders who make the markets move. The composition of the room reflected “the industry is growing up.”

The day opened with Kalshi’s co-founders Tarek Mansour and Luana Lopes Lara, in conversation with Bloomberg’s Katherine Doherty. Below are some takeaways on the industry from that session and the panels that followed.

1. There’s more to life (and markets) than elections and sports.

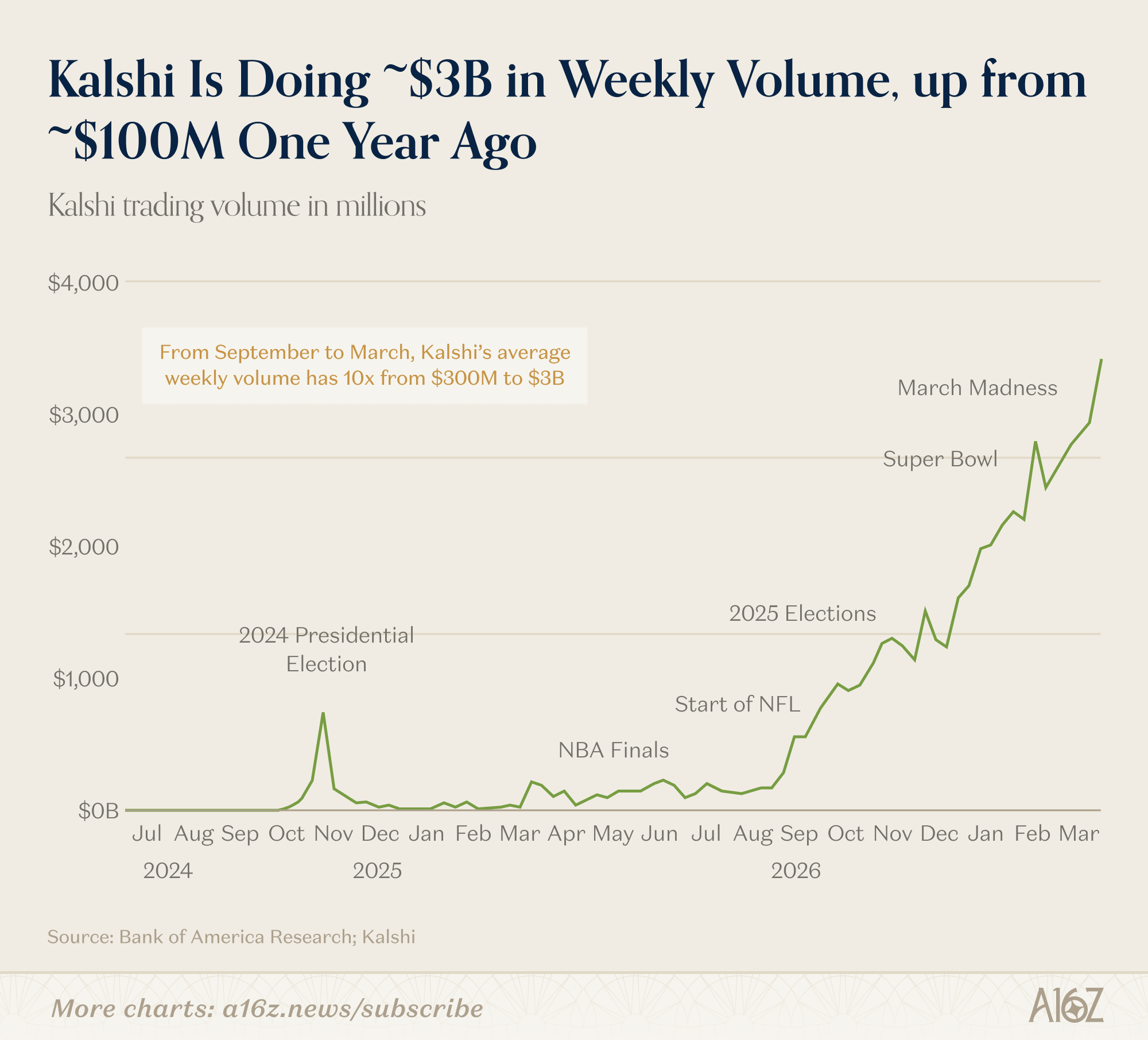

A pattern tends to emerge during major news cycles: a big event (e.g., the 2024 election, or the Super Bowl, or March Madness, more recently) dominates headlines, and by extension prediction market volumes, and people come away with the impression that “that’s the only thing prediction markets are good for.”

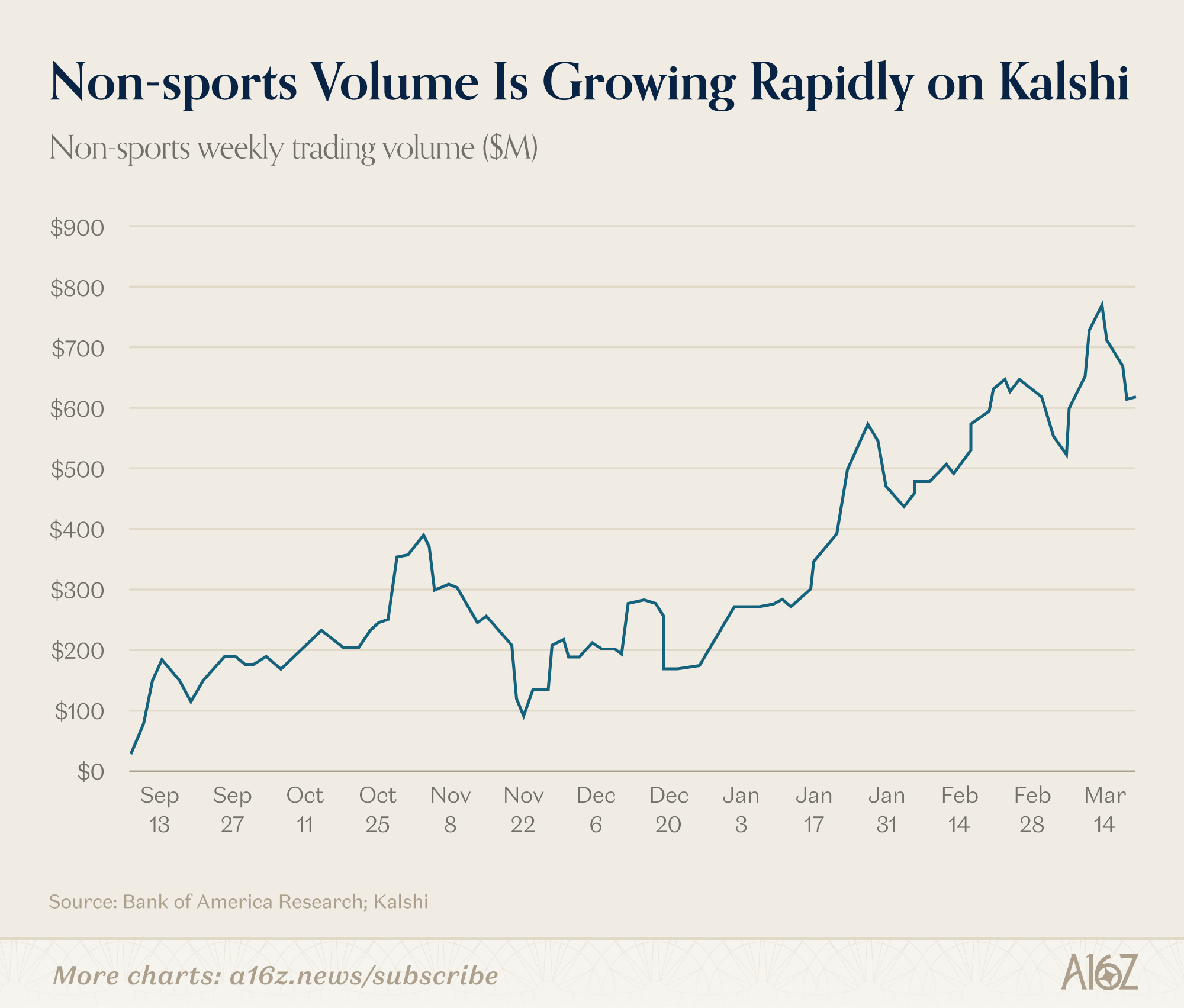

But, while earlier narratives may have suggested prediction markets were only viable during election cycles, Kalshi has seen significant growth in other sectors.

At the time of the research conference, sports trading had just hit nearly $3 billion in weekly volume, roughly 80% of Kalshi’s total, largely driven by March Madness. Tarek and Luana framed this dominance as a phase.

The more revealing stat: sports as a share of total volume was actually at an all-time low even as its absolute volume hit an all-time high. Every other category is growing faster.

Tarek and Luana pointed to entertainment, crypto, politics, and culture as categories showing stronger user-growth — and better volume-retention cohorts than sports. Sports function as a mass-market catalyst; it’s a familiar, scheduled, emotionally engaging wedge product.

But the company is seeing significant growth in its longer-tail markets that make up the remaining 20%+ of Kalshi’s volume, and that are going to be important to institutional hedging and information markets.

An institutional panel later corroborated this observation from the demand side.

Goldman Sachs’ global co-head of equities, Cyril Goddeeris, described predictions related to macro events and CPI prints as the categories where Wall Street attention was most focused.

CNBC’s EVP of growth Sally Shin said she was already using the Fed chair market and non-farm payrolls predictions as storytelling tools.

And Tradeweb’s co-head of global markets, Troy Dixon, described a future where bulge bracket banks have dedicated prediction market trading desks, with financial contracts as the anchor product.

2. Why Kalshi earned Wall Street’s attention.

Traditional financial markets work for lots of reasons, but a big one is that there are agreed-upon benchmarks for every major asset: the S&P 500 is an average of 500 stocks; crude oil has an ICE benchmark.

But for political and economic events (e.g., who wins an election, whether a tariff passes, the outcome of a case before the Supreme Court), few widely-accepted (and dynamic) benchmarks existed before. Prediction markets have changed that. Now, we have a living, liquid benchmark for the future of nearly any event.

Once you have a credible price for, say, a 30% tariff passing, institutional counterparties can transact at that price. It creates a mechanism for trading events directly, or hedging downside in other parts of their portfolio. As Troy Dixon from Tradeweb put it:

“If you go back to when Trump was elected the first time, there was a lot of hedging in the equity market. The trade was short the S&P because obviously if Trump wins it’s going to go down. That was a terrible trade. The challenge is: how do you price these things? What is the benchmark?“

Tarek described a similar motivation for founding Kalshi: working on a Goldman desk that recommended trades pegged to the 2024 election and Brexit. Without prediction markets, institutions trying to hedge political or macro-events through correlated assets are making two bets simultaneously: one on the event, and one on the relationship between the event and the asset being traded. That second bet can go wrong independently.

With a direct benchmark on the event itself, those two bets collapse into one. As Tarek described: “this community is now pricing things.”

3. The three steps toward true institutional adoption.

It would be getting ahead of ourselves to say that major Wall Street firms are trading with size on Kalshi: the majority of institutional use cases today are still about leveraging Kalshi as a data source, rather than a trading platform.

But, it’s still true that there’s a clear progression to wider Wall Street adoption, said Luana, and she outlined it as follows:

Stage one is data: get prices in front of institutional workflows until a Goldman portfolio manager habitually glances at a Kalshi odds feed the same way they consult a VIX reading. This is already happening, to some extent. As John Hopkins University professor and former Fed official Jonathan Wright observed, “for certain things like Fed decisions, unemployment, and GDP, Kalshi is really the only game in town.”

Stage two is integration: compliance and legal sign-off, technology integration, and internal education - the process of onboarding a new instrument.

Stage three is the payoff: actually laying-off risk on the exchange, where volume and depth begin to compound. At that point, more hedgers attract more speculators, tighter spreads attract more hedgers, and the benchmark becomes self-reinforcing.

Today most institutions are still in stage one, a decent portion in stage two, and only a few in stage three.

A big reason more institutions haven’t reached stage three is that currently, trading prediction market contracts requires posting the full notional value as collateral: a $100 position requires $100 in the clearinghouse. For a retail trader, that’s workable, but for a hedge fund or bank operating on leverage ratios and return on capital, it’s a meaningful limitation.

As Tarek put it: “If you want a $100 hedge, you have to put $100 in the clearing house. That’s too expensive for an institution. A Citadel or Millennium wouldn’t do this.” Kalshi just received licensing from the National Futures Association and is working with the CFTC to bring margin trading to market.

4. What’s next?

Bloomberg’s Head of Market Innovation Michael McDonough articulated it most directly: “Success means these things get boring.”

McDonough drew the parallel to options markets in the 1970s: there were similar concerns about manipulation and regulatory uncertainty, all of which eventually resolved into infrastructure so mundane that nobody thinks about twice.

Toby Moskowitz, a principal at AQR, said he was “putting his money where his mouth is” on prediction markets becoming a viable institutional tool within five years, possibly faster.

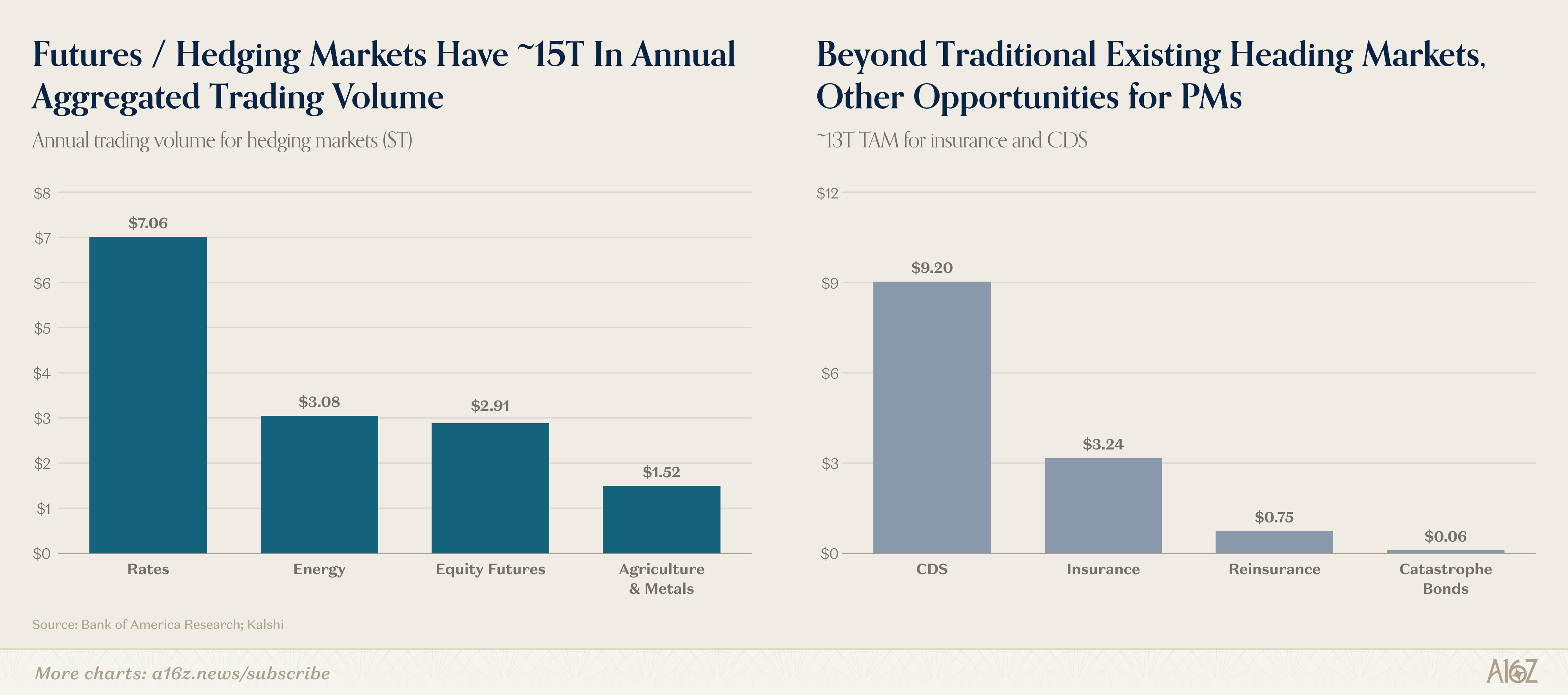

Garrett Herren from Vote Hub described the end state: “It’s not going to be a question of whether we should use prediction markets, but how. And as soon as you start asking that question, you know it’s become indispensable.” Indeed, while prediction markets are currently relatively small, hedging markets are massive:

The truth is that normalization of prediction markets is already underway.

During the politics panel, former Congressman Mondaire Jones noted that congressional leadership on both sides - President Trump, House Minority Leader Jeffries, Senate Minority Leader Schumer - were already publicly citing Kalshi odds. Scott Tranter of DDHQ confirmed that prediction market data is now a standard input inside party committees. And Vote Hub announced it was integrating Kalshi data directly into its midterms forecast model.

None of this was the case two years ago. Two years ago, the most successful traders on Kalshi were still hobbyists. Things are different now. It’s not even fair to call them “hobbyists,” any more.

Four traders during Kalshi’s “The People Behind the Markets” panel described careers built on habits familiar to professional traders—things like, eleven years of obsessing over Billboard charts, or grinding through prediction markets since 2006 back when it was “a dorky hobby” with no real money in it. None of the four panelists came from finance; they came from music, politics, and poker. But all the panelists agreed that the platform rewarded deep, domain knowledge over credentials.

Prediction markets have come a long way. They were supposed to be an academic curiosity, then an election novelty, then a sports betting adjacent product. What the conference made clear is that Prediction markets are maturing into infrastructure for pricing uncertainty across a wide range of participants and use cases - from the retail traders to the largest institutions.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.