Charts of the Week: If you can't join 'em, beat 'em

Plus: Later stage companies, getting lean; YouTube is eating the film industry?; AI converts shoppers; Need more power!

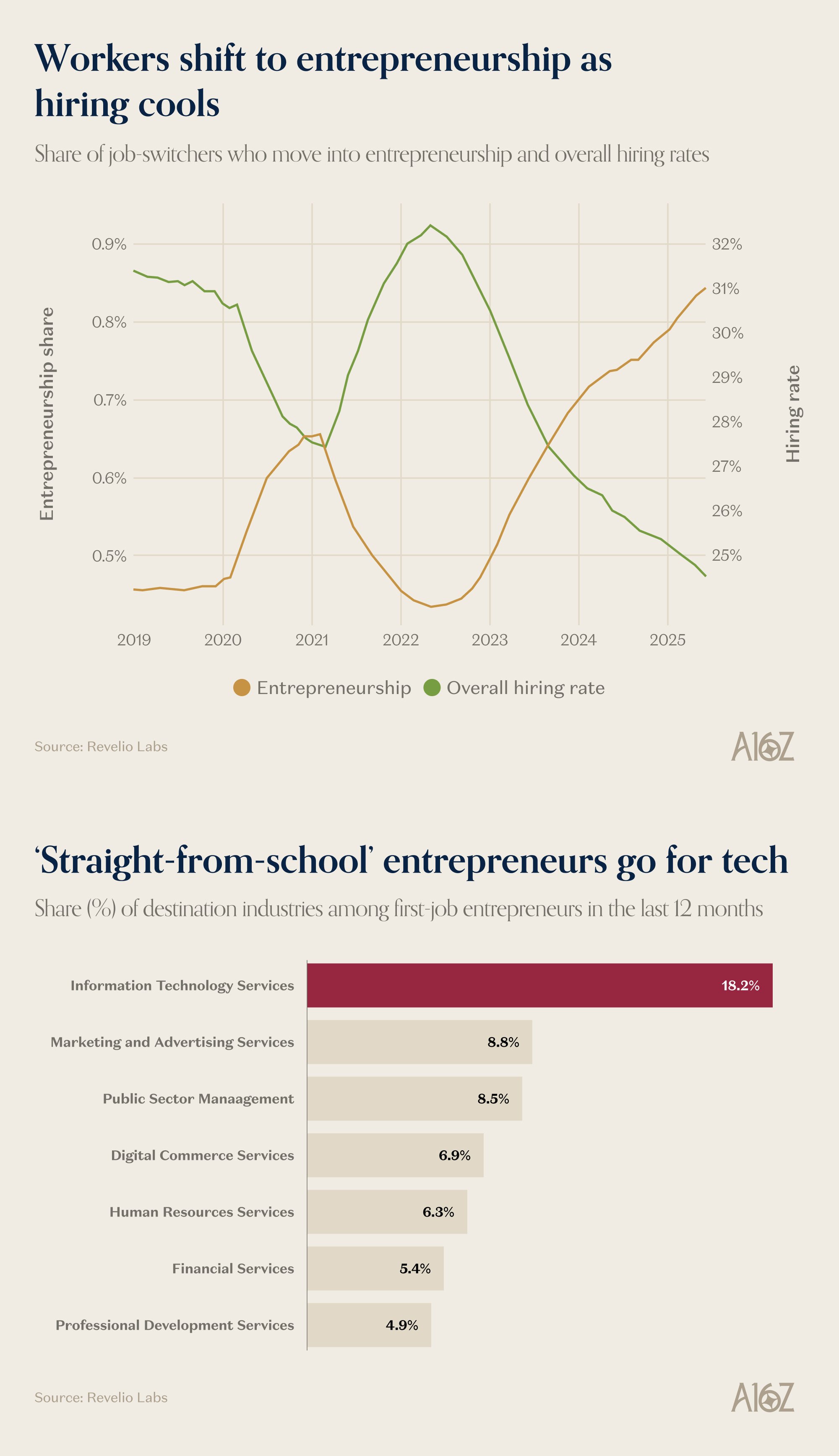

If you can’t join ‘em, beat ‘em

Mind the dual y-axes, but there is an inverse relationship between the “hiring rate” and the share of would-be jobseekers pursuing entrepreneurship.

In other words, back in ‘22-’23, when rates went up, and the job market started getting very tough for recent grads, more and more people said “I’m just going to start my own business.” (Conversely, during ZIRP, when hiring was gangbusters, fewer people decided to go it alone.)

And who specifically is making the jump straight from school into entrepreneurship? It’s startup people, obviously. By far the biggest share of “straight from school” business-starters, launched a tech business (with marketing a distant second).

If you can’t join ‘em, beat ‘em. It’s increasingly tough out there for young grads, but if there’s any culture that’s conducive to high-agency self-starter, it’s startup culture.

Later stage companies, getting lean

SaaS cos at all stages have trimmed headcount since ZIRP, but later stage companies have trimmed the most (according to this data).

For companies with $50M+ ARR, the median number of employees has dropped by 59% from the 2022 peak. That’s much larger than the 42% and 25% drops for middle- and early-stage companies, respectively.

In fact, early stage companies have actually increased headcount off their ‘23 lows, and are about the same as last year (while both mid- and late-stage cos, continued to trim).

Again, not to harp on the hiring stuff, because we know it’s tough out there.

But, to find the silver-lining here, the promise of tech cos has always been tremendous operating leverage, at-scale. Whether it’s AI (or just “trade growth for margins” operating discipline in a higher-rate environment), that’s exactly what this data purports to show: more mature companies are doing more with less.

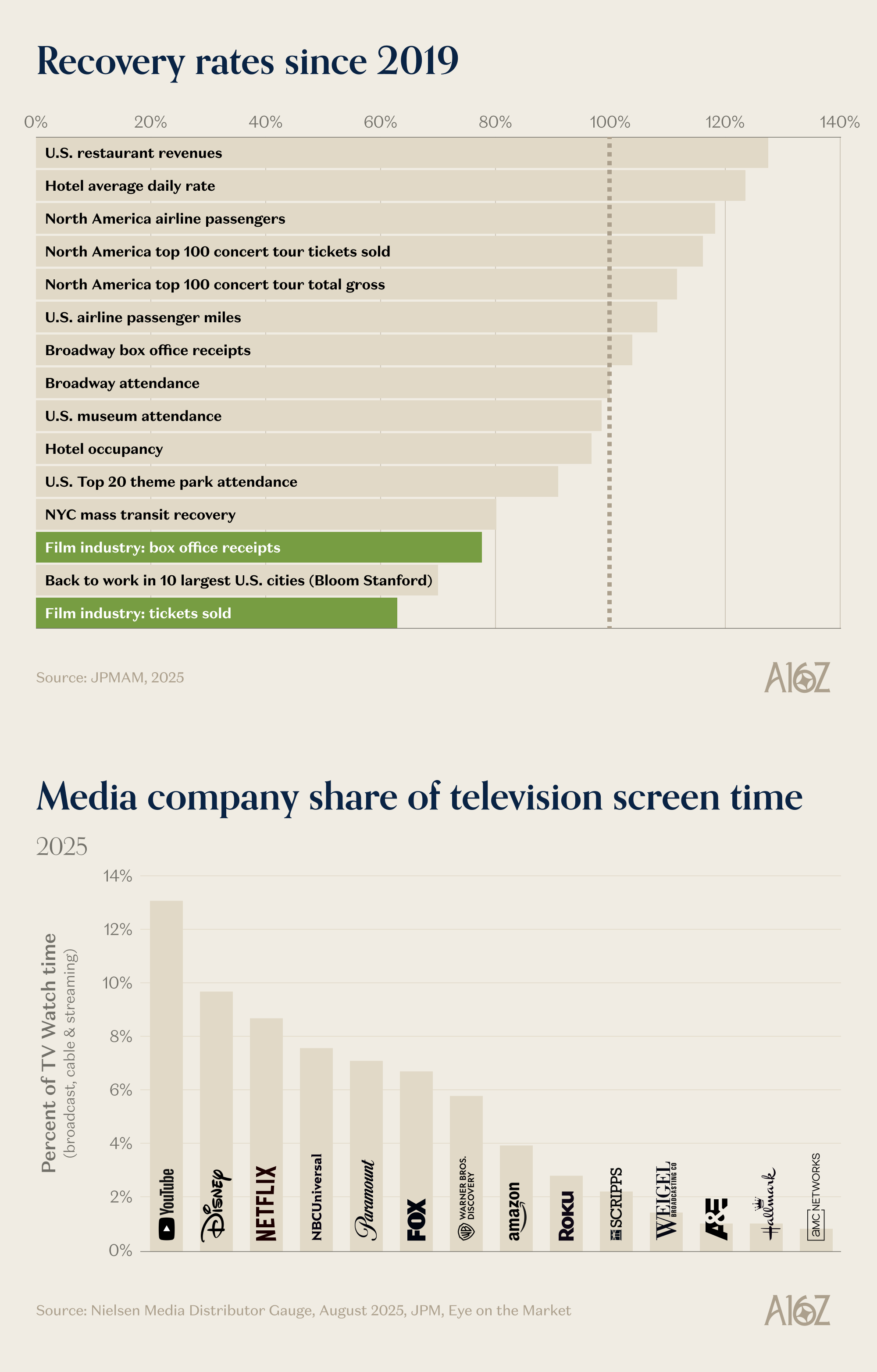

YouTube is eating the film industry?

Of all the “experience” industries attempting to recover their pre-pandemic baselines, the Film Industry is lagging the pack.

Box office receipts and tickets sold are still ~65-75% of what they were back before the world went into lockdown.

At same time, and perhaps coincidentally (but perhaps not), YouTube has captured a staggering 13% of all TV screen-time, far more than any other network, platform or brand.

This one more or less speaks for itself. Big screen movies are struggling. Streaming most definitely is not. Draw your own conclusions.

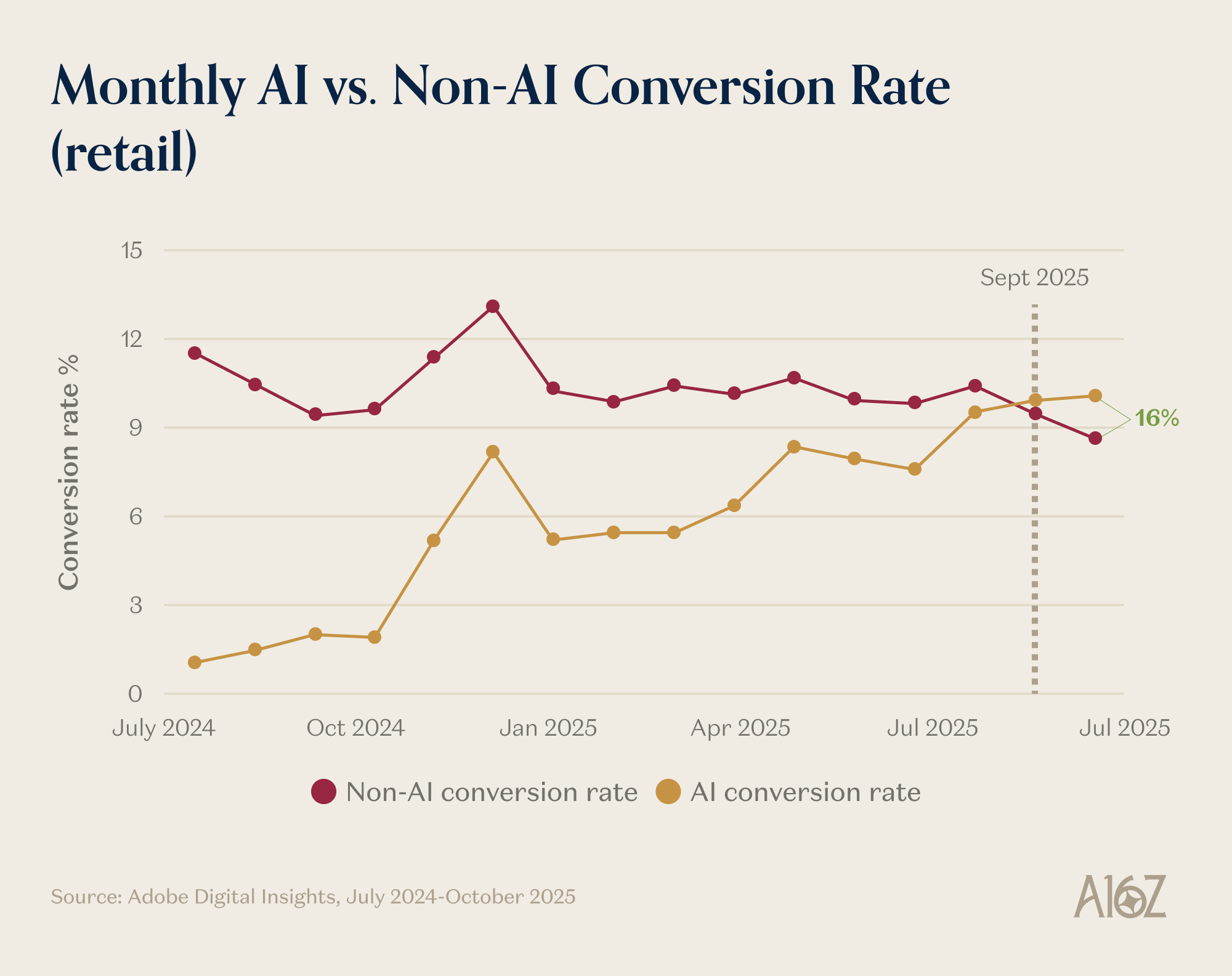

AI shopper? Don’t mind if I do

Recent data from Adobe shows that conversion rates for AI-referrals are now ~16% higher than non-AI

AI conversion rates had been steadily climbing for the better part of the year, but beginning in Fall, there was a visible shift: traditional conversion fell, while AI-conversion leapt ahead

All the caveats about the data (and the recency of the trend) aside, this is kind of a big deal.

There is plenty of other evidence that people (especially GenZ) are increasingly using LLMs for shopping. If the conversion-inversion (see what we did there?) continues to hold, that’s a platform shift, right there.

Need more power!

BloombergNEF has upward revised their forecast for data center power consumption by 36%, just seven months after they released their previous forecast.

As per the report, “[t]he massive growth rate . . . reflects more than a surge in the number of data centers in the pipeline; it also highlights the new centers’ size. Of the nearly 150 new data center projects BNEF added to its tracker in the last year, nearly a quarter exceed 500 megawatts. That’s more than double last year’s share.”

While it’s hard to get perfect estimates on all these buildouts, at least one shows that planned capacity is ~16x of what’s currently operational.

What more can we say? We’re going to need a lot more power. A lot.

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, this content is not investment advice, nor is it intended for use by any investors or prospective investors in any a16z funds. This newsletter may link to other websites or contain other information obtained from third-party sources - a16z has not independently verified nor makes any representations about the current or enduring accuracy of such information. If this content includes third-party advertisements, a16z has not reviewed such advertisements and does not endorse any advertising content or related companies contained therein. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by a16z; visit https://a16z.com/investment-list/ for a full list of investments. Other important information can be found at a16z.com/disclosures. You’re receiving this newsletter since you opted in earlier; if you would like to opt out of future newsletters you may unsubscribe immediately.